- INTC +142% was the single biggest move across all cap tiers — semis dominated mega-cap leadership as the AI capex regime spilled into legacy silicon names.

- Hydrogen showed sector-wide bidding (FCEL +129%, BLDP +104%, PLUG +81%) — speculative reflation in the smallest-cap names with the biggest moves.

- The EV ecosystem cracked across mid + small (LCID −41%, EVGO −32%, ACHR −18%) — even with AI tailwinds elsewhere, mobility-electrification was the cleanest unwind.

The top stock movers of the past three months reveal a market that decided the AI buildout still has room to run — but only if the buildout is in chips and infrastructure. Between February 19 and May 18, 2026 (the most recent US session), the leadership board rotated hard into legacy semiconductors (INTC, AMD, CSCO) and the picks-and-shovels behind them, while consumer-discretionary, EV-mobility, and defensive industrial names were sold across the entire cap-tier ladder.

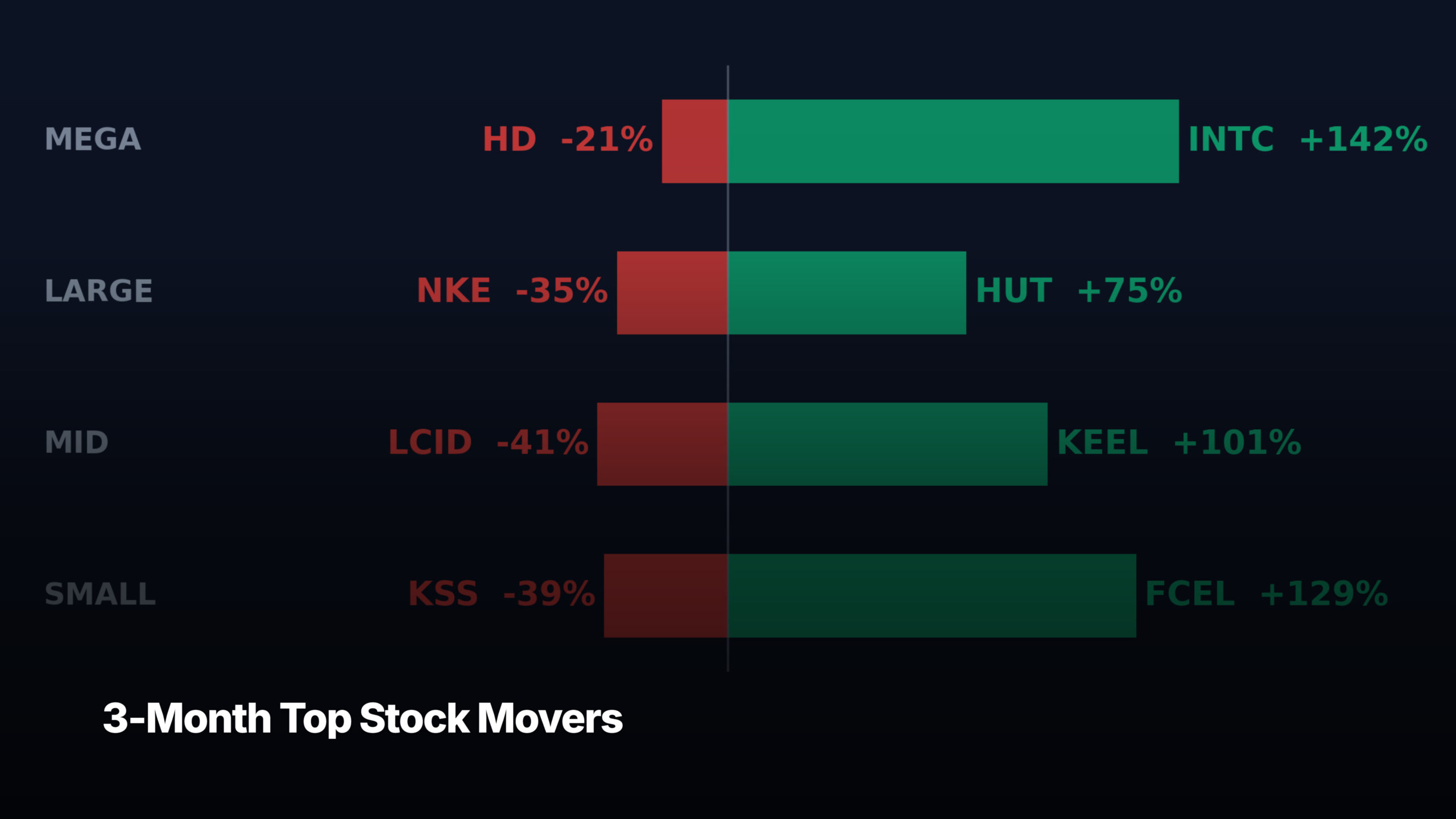

This breakdown is the cap-tier cohort view — top three gainers and top three losers in each of mega, large, mid, and small. Useful for screening today’s leaderboard, not for academic “what worked from the starting line” rankings. Cap tier is computed at current market cap (so a name that crossed up or down a tier during the window appears in the bucket a reader would scan it under today).

Methodology

Universe: ~145 liquid US-listed common stocks across the four cap tiers, drawn from the curated Luna3 Movers universe (refreshed quarterly). Return: total price return (no dividend adjustment) from the February 19, 2026 close to the May 18, 2026 close — 62 US trading sessions, roughly three calendar months. Cap tiers (current market cap): mega ≥ $200B, large $10B–$200B, mid $2B–$10B, small $300M–$2B. Top three winners and top three losers per tier are listed below with a one-line catalyst note and an algorithmic pattern read.

Mega-cap top stock movers (≥$200B)

The mega-cap tier — 44 names in the curated universe — produced the cleanest theme of the quarter: AI semiconductors and AI networking led, while industrial cyclicals and defensives rolled over.

↑ INTC +142.42%

Intel Corporation · $44.62 → $108.17 · mega-cap (~$544B) · price history

Why: Intel’s foundry pivot re-rated as the AI capex regime spilled into legacy silicon. After years of being treated as the wrong-side-of-history mega-cap, the 18A node ramp and turnaround narrative converted a sub-$50 base into the largest mega-cap move of the quarter.

Pattern: Failed-breakdown reversal off a multi-year base — the kind of move that doesn’t show up in trend-following screens until it’s tripled.

↑ AMD +107.01%

Advanced Micro Devices, Inc. · $203.37 → $420.99 · mega-cap (~$686B)

Why: AMD compounded its datacenter-share gains through the quarter as hyperscaler order books for the MI accelerator series extended beyond expectations. The “second-source AI silicon” thesis matured from optionality into earnings reality.

Pattern: Continuation breakout into new highs — momentum reading is strongest of the gainers, not just biggest.

↑ CSCO +51.32%

Cisco Systems, Inc. · $78.56 → $118.88 · mega-cap (~$470B)

Why: Cisco was the quiet beneficiary of the AI buildout — every accelerator rack needs networking. Splunk integration finally showed in observability cross-sell, and hyperscaler switch spend kept compounding.

Pattern: Structural breakout above a multi-year base — clean, low-volatility trend.

↓ HD −20.81%

Home Depot, Inc. · $378.58 → $299.81 · mega-cap (~$299B)

Why: Housing-adjacent demand stayed soft as rate-cut timing kept slipping and tariff pressure on building materials raised ticket-size costs. Big-box home improvement is the cleanest read on the consumer’s mood on big-ticket discretionary spend.

Pattern: Distribution top, lower-high formation below the 50-day moving average.

↓ GE −14.56%

GE Aerospace · $334.74 → $285.99 · mega-cap (~$299B)

Why: Post-spinoff GE Aerospace cooled as the aerospace late-cycle order book moderated and the bar for incremental upside got harder to clear.

Pattern: Gap-down below the 200-day moving average — first major trend break since the spin.

↓ RTX −14.34%

RTX Corporation · $205.41 → $175.95 · mega-cap (~$237B)

Why: Defense-capex moderation pressured the entire prime-contractor cohort. The “indefinite ramp” story that worked for two years gave way to a more selective procurement environment.

Pattern: Distribution below the 50-day, lower-low formation.

Large-cap top stock movers ($10B–$200B)

Large-cap (54 names) split into two clean themes on the upside — AI infrastructure (DDOG observability, HUT Bitcoin-miner-to-HPC, IONQ quantum compute speculation) — and three different ways to be a tired consumer brand on the downside.

↑ HUT +75.36%

Hut 8 Corp. · $54.86 → $96.20 · large-cap (~$10.8B)

Why: Hut 8 graduated from the small-cap miner cohort into large-cap territory on the back of the Bitcoin-miner-to-HPC-infrastructure conversion trade — the same playbook BITF/Keel ran in 2025. Power-tier hyperscaler interest in pre-built grid-connected sites is the actual fundamental.

Pattern: Stage-2 breakout from a multi-month accumulation base.

↑ DDOG +73.15%

Datadog, Inc. · $120.60 → $208.82 · large-cap (~$74B)

Why: AI observability moved from feature to category. As every hyperscaler customer scaled inference workloads, Datadog’s per-seat and per-host expansion ramped harder than the consensus model could keep up with.

Pattern: Cup-and-handle breakout to new all-time highs.

↑ IONQ +47.50%

IonQ, Inc. · $33.43 → $49.31 · large-cap (~$18B)

Why: Quantum compute kept reading as the “next leg of AI exposure” for speculative buyers. Government and academic contract wins gave the narrative just enough real-revenue scaffolding to stay credible.

Pattern: Speculative breakout with above-average volume on every up-day — algo-friendly continuation tape.

↓ NKE −35.12%

Nike, Inc. · $65.61 → $42.57 · large-cap (~$63B)

Why: Brand-strength erosion compounded across China weakness, tariff exposure on cost of goods, and a longer-than-expected reset of the wholesale channel. The “iconic moats are forever” thesis took the hardest hit it has in a decade.

Pattern: Failed bounce off the 200-day, lower-low confirmation.

↓ RBLX −27.09%

Roblox Corporation · $64.44 → $46.98 · large-cap (~$34B)

Why: Daily active user growth decelerated while monetization-per-user questions stayed unresolved. Platform-economy multiples compressed across the cohort.

Pattern: Distribution top, three-month downtrend with lower-highs.

↓ LUV −26.34%

Southwest Airlines · $52.08 → $38.36 · large-cap (~$19B)

Why: The low-cost carrier model is squeezed at both ends — fuel and labor costs rising, fare discipline holding airlines from passing it through. Southwest’s structural advantages eroded faster than the operational fixes could land.

Pattern: Bear flag continuation, multi-quarter downtrend intact.

Mid-cap top stock movers ($2B–$10B)

Mid-cap (26 names) was the most thematically split tier — Bitcoin/AI infrastructure and hydrogen on the upside, mobility-electrification on the downside.

↑ KEEL +100.96%

Keel Infrastructure Corp. · $2.08 → $4.18 · mid-cap (~$2.5B)

Why: The post-Bitfarms rebrand to Keel was the cleanest “miner-to-HPC infrastructure” story of the quarter. Power-tier hyperscaler contracts converted the equity from a Bitcoin-beta name into an infrastructure-beta name — different multiple, different buyer base. See the CLSK Stock Analysis for the comparison framework.

Pattern: Stage-2 breakout off a $2 base into a new tier classification.

↑ PLUG +80.63%

Plug Power, Inc. · $1.91 → $3.45 · mid-cap (~$4.8B)

Why: Hydrogen sector re-rate combined with improving DOE loan visibility and operational milestones. Plug benefited from the “biggest pure-play hydrogen optionality” status as the sector caught a bid.

Pattern: Failed-breakdown reversal — the kind of move that punishes shorts caught in a crowded book.

↑ MARA +53.02%

MARA Holdings, Inc. · $7.96 → $12.18 · mid-cap (~$4.6B)

Why: Bitcoin price strength combined with hashrate-efficiency gains kept the pure-miner thesis viable for one more quarter, even as the cohort started fragmenting between miners-staying-miners and miners-pivoting-to-HPC.

Pattern: BTC-correlated continuation, beta-to-BTC remained the dominant input.

↓ LCID −41.23%

Lucid Group, Inc. · $9.75 → $5.73 · mid-cap (~$2.2B) · price history

Why: Lucid was the worst-performing stock across all cap tiers in the window. Demand softness, production-miss optics, and ongoing dilution overhang from the Saudi PIF backstop kept the equity bid-less. The luxury-EV thesis has the longest gap between price and reality of any segment in the space.

Pattern: Lower-low confirmation, distribution off every bounce attempt.

↓ ALK −28.33%

Alaska Air Group, Inc. · $52.13 → $37.36 · mid-cap (~$4.2B)

Why: The airline pressure that hit LUV in large-cap played out one tier down too — fuel-cost exposure, capacity-discipline limits, and integration costs from the Hawaiian deal still bleeding through margins.

Pattern: Bear flag, multi-quarter downtrend intact.

↓ ACHR −18.12%

Archer Aviation Inc. · $7.23 → $5.92 · mid-cap (~$4.5B)

Why: eVTOL certification timelines drifted again, and the entire urban-air-mobility cohort sold off as “binary FAA outcome” risk got priced more honestly. The story didn’t break — the buy-the-narrative cohort just thinned.

Pattern: Lower-high formation below the 50-day, range compression.

Small-cap top stock movers ($300M–$2B)

Small-cap (13 names that cleared the dollar-volume floor) gave us the most extreme dispersion — hydrogen pure-plays multi-bagged while retail and EV-adjacent names hit fresh 52-week lows.

↑ FCEL +128.90%

FuelCell Energy, Inc. · $7.75 → $17.74 · small-cap (~$0.9B)

Why: FCEL was the sharpest single-name expression of the hydrogen revival. Utility-scale fuel-cell deployment optionality plus hyperscaler interest in stationary power for AI sites gave the equity two narratives to ride at once.

Pattern: Parabolic move off the base — 3x in 62 sessions is algo-classifiable as “speculative reflation tape,” not trend.

↑ BLDP +104.25%

Ballard Power Systems, Inc. · $2.12 → $4.33 · small-cap (~$1.3B)

Why: Hydrogen fuel-cell adoption in commercial-vehicle applications and clearer government-funding visibility re-rated the equity from “perpetual story stock” to “story stock with a balance-sheet runway.”

Pattern: Stage-2 breakout above a multi-quarter base.

↑ TDOC +30.12%

Teladoc Health, Inc. · $4.88 → $6.35 · small-cap (~$1.1B)

Why: Telehealth re-rating from “left for dead” status as cost discipline started showing through in operating margins. Not a structural rerating — a “we may have over-discounted the survivor case” rerating.

Pattern: Failed-breakdown reversal off a multi-year base.

↓ KSS −39.15%

Kohl’s Corporation · $19.26 → $11.72 · small-cap (~$1.3B)

Why: Mall-anchor retail kept losing share to off-mall channels and traffic erosion accelerated. Tariff exposure on private-label sourcing layered on top. The “value retail moat” thesis ran out of room.

Pattern: Lower-low into a fresh 52-week low — distribution tape.

↓ EVGO −31.91%

EVgo Inc. · $2.82 → $1.92 · small-cap (~$0.6B)

Why: EV-charging unit economics stayed unresolved even as the broader EV cohort weakened. Capex slowdown plus utilization questions left the equity in a smaller and smaller buyer base.

Pattern: Distribution, lower-low below all moving averages.

↓ JBLU −22.50%

JetBlue Airways · $5.91 → $4.58 · small-cap (~$1.7B)

Why: Same low-cost-airline cost-pressure thesis that hit LUV and ALK, with the added complication of post-merger-block strategic ambiguity. Smaller-cap airlines are taking the heaviest hits of the cohort.

Pattern: Bear flag continuation, no support test held.

What this tells us about Q2 2026 leadership

Four things stand out when you scan the 24 names as a cohort rather than 24 individual stories.

AI capex is still the regime, but the trade rotated. The three biggest mega-cap winners (INTC, AMD, CSCO) are all silicon-or-network infrastructure plays — not the platform names that led 2024–2025. When the regime trade rotates within itself, it usually means the regime has another leg, not that it’s over.

Hydrogen ran the same playbook crypto did in 2021 — small-caps led the bid. FCEL, BLDP, and PLUG combined for an average ~104% return with the smallest combined market cap on the gainers’ board. Sector-wide bids that start in the smallest, most-shorted names are usually reflation trades, not structural shifts. Whether it sticks depends on whether the funding visibility (DOE loans, hyperscaler stationary-power demand) converts into Q3 contract announcements.

EV-and-charging is the cleanest unwind in the market. LCID (cars, −41%), EVGO (charging, −32%), ACHR (eVTOL, −18%) — the entire mobility-electrification stack got sold across mid- and small-cap. This is rare enough to flag: when an entire thematic stack moves the same direction with this kind of magnitude, the cohort is being repriced, not just rotated.

The airline cohort weakened across three cap tiers (LUV large, ALK mid, JBLU small) — a textbook full-cohort weakness signal that screening tools usually miss until the sector ETFs have already broken. The next 3-month window is the one where airline cost-pressure either resolves into capacity discipline (bullish) or breaks into balance-sheet stress (further downside). For more on cohort vs single-name reads, see the weekly top stock movers and monthly top stock movers — same cap-tier structure, shorter windows.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!