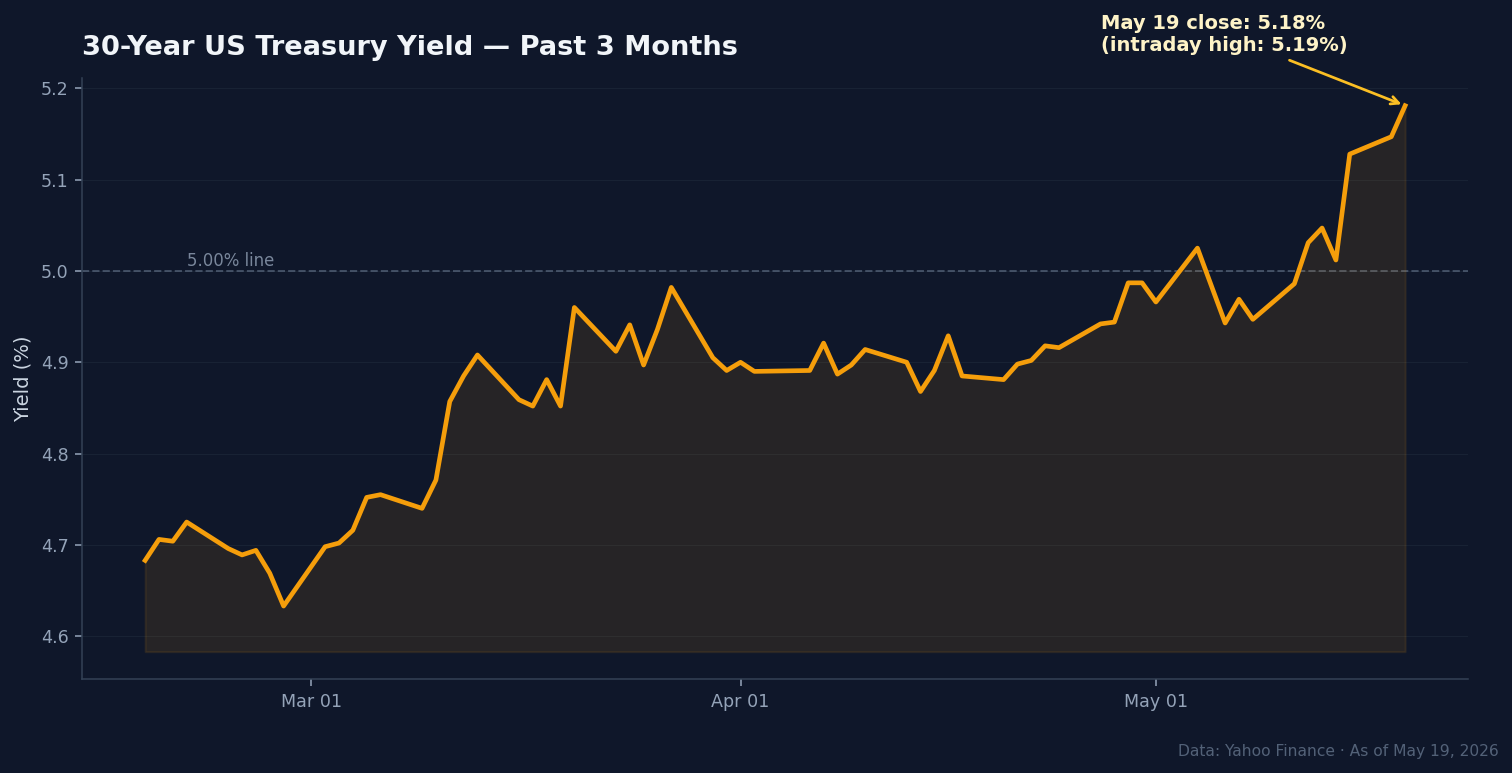

- The 30-year US Treasury topped 5.19% Tuesday — its highest level since 2007 — as the S&P 500 closed lower for a third straight session.

- Reddit and FinTwit are fixated on NVDA's after-bell print tonight, but the consensus is anxious: a 97% beat probability is already priced and the stock has fallen on three of the last four beats.

- What actually matters is the Q2 guide (~$86B consensus, whisper ~$90B) and any China re-entry framework — bigger variables than the headline revenue number.

Welcome to today’s Market Pulse Open Take. The 30-year US Treasury topped 5.19% on Tuesday — its highest level since 2007 — as the S&P 500 closed lower for a third straight session. NVIDIA reports Q1 FY27 earnings after the bell tonight, into the most awkward bond-market backdrop the AI rally has seen all year. We flagged the rates already ripping ahead of Wednesday’s print yesterday. Today they ripped harder.

What Tuesday’s tape said

Tuesday was an across-the-board down day, but the real story was in bonds, not stocks.

- S&P 500: −0.67% to 7,353.61 (third consecutive losing session)

- Nasdaq Composite: −0.84% to 25,870.71

- Dow Jones: −322 points (−0.65%) to 49,363.88

- 30-year Treasury yield: intraday high 5.19%, closed at 5.18% — the highest level in nearly 19 years

- 10-year Treasury: intraday high 4.687% (highest since January 2025), closed near 4.67%

- Oil: WTI above $104, Brent above $111 — Iran-conflict supply risk holding crude elevated

The pop in yields wasn’t a one-day shock. It was the bond market reacting to a stack of unfinished business: Friday’s Moody’s downgrade of US sovereign credit, oil holding above $100 on continued Iran-conflict supply risk, and a growing Wall Street view that the next Fed move could be a hike rather than the rate cut equities have been pricing for months.

Two stocks bucked the red tape. Home Depot beat Q1 EPS estimates (non-GAAP $3.43 vs ~$3.41 consensus) — though revenue came in line at $41.77B and the stock still dipped roughly 2.5% premarket on margin commentary. Micron closed up roughly 2.5% (with an intraday pop above +4%), snapping a three-day losing streak after Citi raised its price target to $840 on continued strength in DRAM and NAND pricing through 2027.

What the crowd is saying

Scroll r/wallstreetbets, r/stocks, or r/investing on Tuesday evening and one ticker dominated: NVDA. The volume is record-setting. The sentiment underneath the volume is anxious, not euphoric.

The dominant thread, repeated in different shapes across subs: “Everyone knows they’ll beat — and the stock fell three of the last four beats. Why would this one be different?” Polymarket prices a 97% probability that NVDA beats consensus, which is the highest pre-print certainty of any large-cap reporting this season — and also the most crowded long going in.

On X, the two camps hardened. AI bulls point to the hyperscaler capex cycle still ramping (~$700B run-rate for 2026 across MSFT, META, GOOGL, AMZN), Blackwell deliveries accelerating, and consensus revenue of ~$79B carrying the trade through the print. Bond vigilantes counter that growth multiples compress structurally when the long bond yields 5.2% — even a clean beat doesn’t reset that math, and a soft guide makes it worse.

Google Trends shows “NVDA earnings” searches spiking sharply through Monday and Tuesday. “Treasury yield” searches have been elevated continuously since Moody’s downgraded US sovereign credit on Friday. The crowd is paying attention to both stories — and the cross-currents are exactly the problem.

The tension — what actually matters tonight

It’s not the beat. At a 97% priced-in probability, the beat is essentially a formality. NVDA has beaten its own guidance every quarter since the AI boom started, by anywhere from $1B to $6B over the midpoint.

What matters is the Q2 guide. Central consensus sits at roughly $86 billion; whisper numbers cluster closer to $90 billion. A guide of $87B+ confirms the ramp and gives bulls cover. Below $85B and the “growth deceleration” narrative grabs the microphone — and at 5.2% on the long bond, deceleration narratives don’t get the benefit of the doubt.

The wildcard is China. H200 delivery timelines, any framework for re-entry to the Chinese market, and commentary about recent Beijing visits — multiple sell-side analysts have called these the single biggest variable on the call, bigger than the headline revenue number. The market hasn’t priced a clean answer either way; it is just waiting.

And underneath all of it: the backdrop the bulls didn’t plan for. NVDA is up roughly 20% in the past month into this print, which means the bar for an upside surprise is unusually high. The last time NVDA beat by a clean margin — Q4 FY26 in February, ~6% EPS beat — the stock fell roughly 5% the next day. What NVDA’s earnings mean for the broader AI trade is now mostly a question of stock reaction, not headline numbers.

What this Market Pulse Open Take is watching tonight

Four things, in order of priority:

- Revenue vs ~$79.2B consensus (+79.5% YoY against Q1 FY26’s $44.06B).

- Q2 guide vs ~$86B consensus — every dollar above $87B reads as confirmation; anything below $85B opens the deceleration narrative.

- China commentary — any mention of H200 timelines, Beijing visit, or re-entry framework.

- The after-hours reaction itself — a beat-and-drop tells you the 20% monthly run already front-ran the news; a beat-and-pop reopens the AI rally and forces the bond bears to wait another quarter.

The S&P 500 falling for a third consecutive session into one of the most heavily-positioned earnings events of the year is the kind of setup that produces big moves in both directions. We will cover the print and the reaction in tomorrow morning’s Open Take. For now: short positions are nervous, long positions are nervous, and the only people sleeping well tonight are the ones who already decided not to trade it.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!