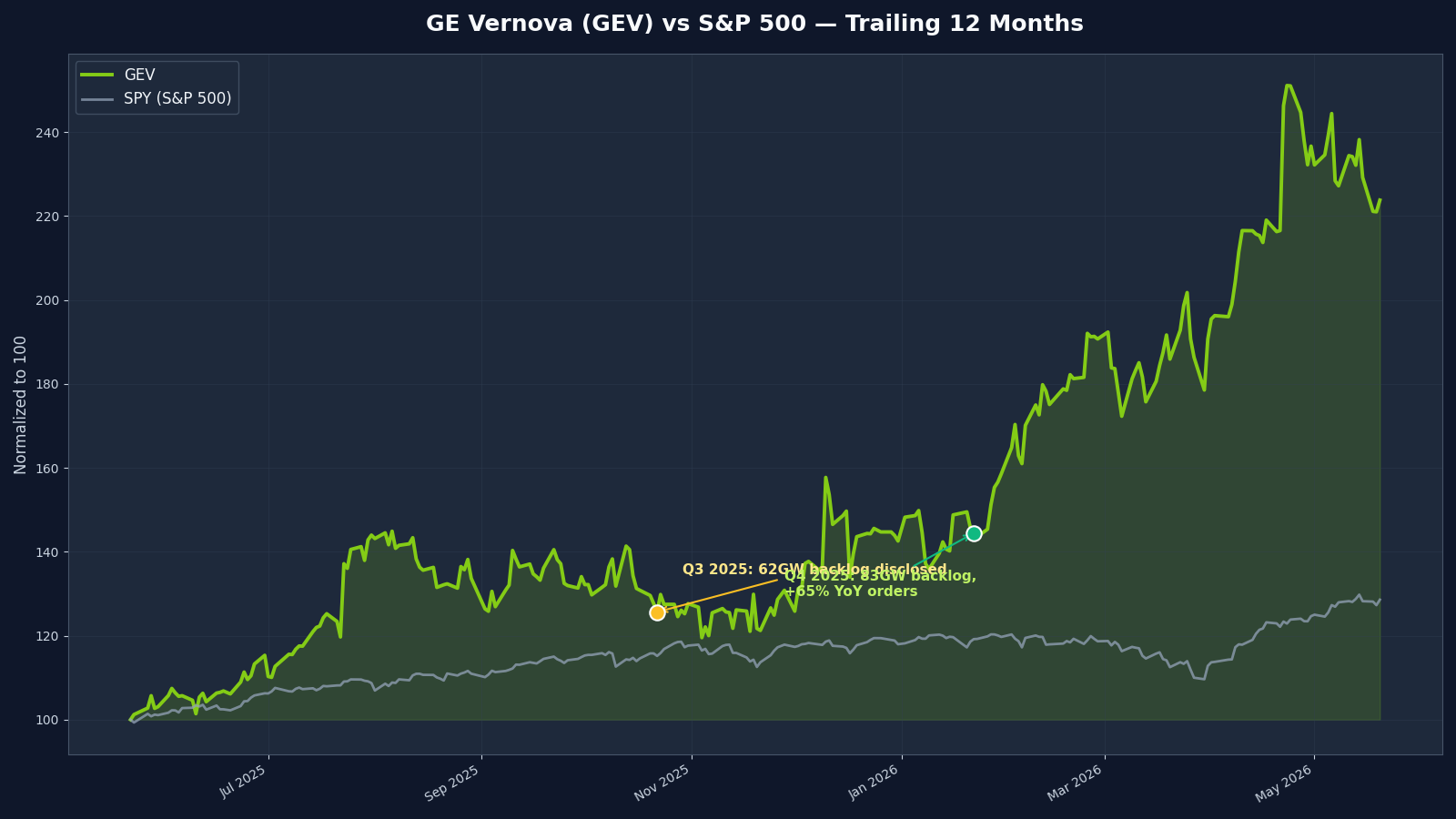

- GE Vernova's gas turbine backlog jumped from 62GW to 83GW in a single quarter (Q4 2025), with deliveries now stretching into 2029 and full sellout through 2030 targeted by end of 2026.

- Manufacturing capacity is the binding constraint — GEV is ramping toward ~20GW of annual gas turbine shipments starting 2027, against an order book multiple times that size. Capacity expansion takes 3–5 years; near-term earnings are almost fully locked.

- The investable cohort isn't just GEV. Independent power producers (VST, CEG, NEE), upstream electrical-equipment suppliers (ETN), and competitor Siemens Energy all sit downstream or adjacent to the same demand wave — even though gas turbines themselves are concentrated in one Western manufacturer.

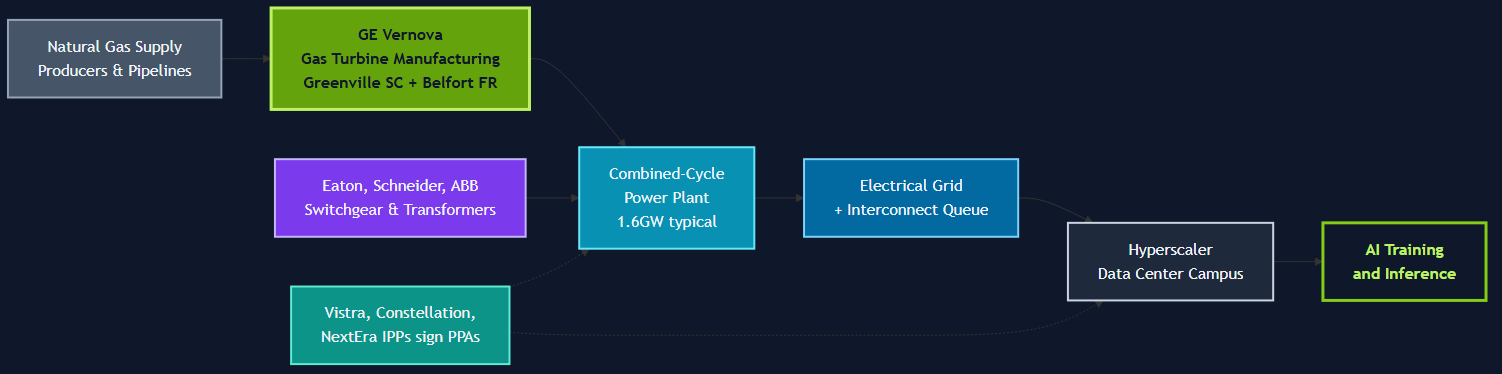

Grid Strategies projects 166GW of US peak power demand growth by 2030, with data centers accounting for roughly 55% of that growth — and gas turbines are the swing supplier filling the gap that solar and batteries cannot dispatch on demand. Big Five hyperscaler capex is tracking above $600B in 2026 (a 36% jump on 2025), and almost all of it ultimately needs to plug into something. That something, for the rest of this decade, is mostly gas. A GE Vernova gas turbine — the heavy-duty kind that anchors a 1GW combined-cycle plant — has become one of the hardest items to buy in the entire AI infrastructure stack.

The stock — ticker GEV — last printed $1024.52 going into publication on May 21, 2026, and has more than doubled in the trailing twelve months on the back of a backlog that now exceeds four years of forward shipments. The story isn’t the multiple. It’s the order book.

Why this matters now

The nuclear story is real, but small modular reactors are 2030-plus at earliest for meaningful capacity. The first commercial NuScale design is still working through NRC pathway and EPC sequencing; X-energy’s TRISO-based reactor hasn’t yet broken ground at scale. Until the SMR fleet shows up, hyperscalers need power they can sign a 15-year PPA on today — and that means gas-backed independent power producers, contracting against new gas-fired generation capacity.

That demand wave hit GE Vernova’s order book in 2025. Gas Power equipment backlog plus slot-reservation agreements went from 62GW at the end of Q3 2025 to 83GW by year-end — a 21GW jump in a single quarter, with Q4 orders alone surging 65% year-over-year to $22.2B per the company’s Q3 2025 SEC 8-K filing. CEO Scott Strazik has since said the company expects to be fully sold out through 2030 by the end of 2026.

The competitive landscape makes the bottleneck binding. Siemens Energy is the closest peer but is fighting its own transformer-and-switchgear supply constraints. Mitsubishi Power is Japan-centric and has limited US footprint. That leaves GEV with effective duopoly economics in the Western heavy-duty gas turbine market at the exact moment hyperscaler demand is going vertical.

How a GE Vernova gas turbine business actually works

The hardware itself is the headline product but not the full revenue story. GEV’s flagship H-class turbines come in two main configurations: the 9HA.01 at 448MW per unit and the 9HA.02 at 571MW per unit, with the smaller 7HA also in active production. One unit anchors one combined-cycle plant block; a 1.6GW data-center campus typically needs three or four. Per CEO Strazik, directional lead times on new heavy-duty orders are now running about three years from booking to delivery, with non-prioritised slots quoted at five to seven years.

Underneath the equipment shipment is the part the equity market still under-prices: long-term service agreements. Every turbine that leaves Greenville pulls a multi-decade LTSA behind it — recurring, high-margin maintenance revenue that compounds as the fleet ages. The implication of an order book stretching into 2029 isn’t just three years of locked equipment revenue. It’s a service tail that will print steady cash flow into the 2040s on hardware shipping today.

Manufacturing footprint is concentrated. The Greenville, South Carolina facility is GE Vernova’s largest gas turbine plant and the HA Repairs Center of Excellence for the Americas, with a $160M-plus capacity expansion announced in 2025. Belfort, France assembles GEV’s 50Hz frames — the 6B, 6F, 9E, 9F, and 9HA — for European, Middle East, and Asia-Pacific customers. Capacity expansion is not a software problem. New manufacturing lines require specialised machining, decade-scale workforce training, and a tightly integrated casting and forging supply chain that itself runs at near-full utilisation. Greenville’s expansion is real but slow; the line capable of producing a 9HA.02 cannot be cloned from a press release.

The capacity ceiling — why the backlog matters more than the multiple

GE Vernova plans to ramp toward roughly 70–80 heavy-duty gas turbines per year starting in the second half of 2026, equivalent to approximately 20GW of annual gas turbine shipments by 2027 per CEO commentary at the company’s 2025 investor day. Set that 20GW/yr output target against an 83GW backlog and the arithmetic is uncomfortable for late-arriving customers: orders placed now ship against 2028 and 2029 slots, and some customers are already being pulled into 2030 on engineering-procurement-construction sequencing grounds.

The corollary is that the near-term earnings picture is almost fully visible. Equipment revenue ramp into 2027–2028 is largely contracted. The live debate isn’t whether GEV can deliver those years — it’s whether the manufacturing footprint can expand in time to capture incremental orders into 2030–2032, when hyperscaler demand might be even higher than today’s projections imply.

Compare the capacity-expansion timeline to semiconductor analogues. TSMC can stand up a new fab in roughly 2–3 years. A new heavy-duty gas turbine assembly line is closer to 5 years, and that’s assuming the upstream supply chain — specialised superalloy castings, precision blade machining, qualified welders — expands in step. It’s a higher moat and a slower ramp than the AI accelerator hardware downstream of it. That asymmetry is exactly what makes the gas turbine layer of the AI infrastructure stack so interesting.

Where the money flows

Gas turbines are the single most concentrated chokepoint in the AI power stack, but the investable cohort isn’t just GE Vernova. The capex cycle radiates outward to the IPPs that own the plants, the utilities that interconnect them, the electrical-equipment suppliers that fit them out, and even non-US competitors who are picking up the orders GEV can’t deliver fast enough.

GE Vernova (GEV) is the direct pure-play. The equity has more than doubled off its spinoff debut, but the under-priced part of the model remains the recurring service revenue tail — a 25-year annuity attached to every turbine shipped. If you’re going to own one name in the AI power thesis, it’s the one with the order book the market actually has visibility into.

Vistra (VST) and Constellation Energy (CEG) are the IPPs most aggressively building gas-backed capacity to sell into hyperscaler power-purchase agreements. Both have signed multi-gigawatt deals with hyperscalers in the past 18 months; both trade like utilities but are now closer to long-duration call options on data-center power demand. NextEra (NEE) is the largest US power developer and explicitly frames gas as the bridge fuel within its long-run renewables thesis. Gas turbine constraint helps these three the same way drought helps a water utility — it raises the value of incumbency.

Eaton (ETN) and the broader electrical-equipment cohort sit upstream of the turbine. A new gas-fired plant doesn’t generate revenue without switchgear, transformers, grid interconnection equipment, and busbars — all categories where Eaton, Schneider Electric (private), and ABB (non-US) are the relevant names. The next bottleneck after the turbines themselves is the electrical equipment that wires them into the grid. Lead times on large transformers are already running 18–24 months and lengthening.

Outside the US listings, Siemens Energy (SIE GY) is the relevant competitive name — relevant context, not a recommendation here. Mitsubishi Heavy Industries’ power arm remains private at the listed-entity level but its gas turbine business is the third leg of the heavy-duty oligopoly. Their order books are filling for the same reasons GEV’s is.

This is a theme post, not a single-name thesis. The point isn’t that GEV is the only stock that benefits — it’s that the bottleneck radiates value to a clearly identifiable cohort, and the cohort is investable in public markets. We’ve covered the demand side in our analysis of the $700B hyperscaler capex cycle and the longer-term SMR nuclear story; this post fills in the near-term supply-side response.

What could break this thesis

Demand destruction. The most direct risk is a downward revision to hyperscaler capex guidance. Microsoft, Google, Amazon, and Meta all guided higher on infrastructure spending in their Q1 2026 prints, but capex guides have rolled over before — the 2022 cloud-spending air pocket erased a year of consensus capex assumptions in a quarter. If guidance reverses, the gas turbine order intake softens months before backlog reduces, and the equity de-rates immediately.

Faster SMR resolution than expected. If NuScale, X-energy, or one of the next-generation reactor designs clears NRC certification and breaks ground at scale earlier than the 2030 base case, the gas bridge shortens. Long-duration gas-fired PPAs become less attractive against firm zero-carbon nuclear. The order book stretches less; the multiple compresses faster than fundamentals would imply.

GE Vernova execution risk. Manufacturing scale-ups are not free options. Workforce attrition at Greenville, defects on the 9HA.02 line, raw-material bottlenecks in nickel superalloy castings, or a single high-profile field failure can each compress margins or delay shipments. The market is pricing roughly flawless execution; reality has historically been messier.

Policy risk. Inflation Reduction Act modifications, EPA emissions rules tightening on new gas capacity, or state-level moratoria on new fossil generation (already in motion in some Northeast and West Coast jurisdictions) all change the economics of new gas-fired plants. None of these by itself ends the thesis, but each at the margin shifts the project mix.

Signals to watch

Three quarterly data points are the cleanest read on whether the thesis is still on track:

- GE Vernova quarterly order intake. Backlog growth deceleration — orders falling materially short of shipments in any given quarter — is the leading indicator that demand is peaking. The Q3-to-Q4 2025 21GW step-up is the bar to beat.

- Hyperscaler capex commentary. Microsoft, Alphabet, Meta, Amazon, and Oracle earnings calls — specifically the FY guidance commentary and capex-as-percentage-of-revenue numbers. The current 45–57% capital intensity is historically extreme; any retreat is a tell.

- Siemens Energy quarterly. The closest competitor’s order intake is the cross-check. If Siemens Energy’s gas turbine bookings accelerate while GEV’s flatten, the relative bottleneck has shifted; if both keep filling, the demand wave is intact.

And one more, less obvious read: FERC interconnection-queue updates. A queue that’s overwhelmingly gas-weighted confirms the bridge-fuel narrative. A queue that pivots toward solar-plus-storage at the margin tells you the relative economics are shifting. The interconnection queue moves before the order book moves, which moves before the equity does.

Cohort-level views like this one tend to age better than single-name predictions. The next two to three years of AI power demand sits with gas turbines because that’s where the dispatchable capacity actually exists. The investable question isn’t whether the bridge holds — it’s how the value distributes along it.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!