- A high-yield savings account (HYSA) pays roughly 11× what the average US savings account pays right now — 4.20–4.50% APY vs the FDIC national average of 0.38%.

- On a $20,000 emergency fund, that gap is about $824 a year in interest you're either earning or leaving behind. FDIC insurance applies to online banks exactly the same as to brick-and-mortar.

- HYSAs are variable-rate: when the Fed cuts, your APY follows. They beat money market funds on simplicity, but T-bills can win on taxes once you're past your emergency-fund target.

What is a HYSA? Short for high-yield savings account — a deposit account at an FDIC-insured bank that pays substantially more interest than a standard savings account, without locking up your money. That’s the whole product. The catch is that almost nobody at a traditional brick-and-mortar bank uses one, even though the rate difference is now large enough to matter.

Right now, the FDIC national average savings rate is 0.38% (as of May 18, 2026). The best widely-available HYSAs are paying 4.20% to 4.50% APY. On a $20,000 emergency fund, that’s the difference between earning roughly $76 a year and earning roughly $900 — about $824 you either keep or hand back to your bank, depending entirely on which account holds the money.

Why this matters in a 5% rate world

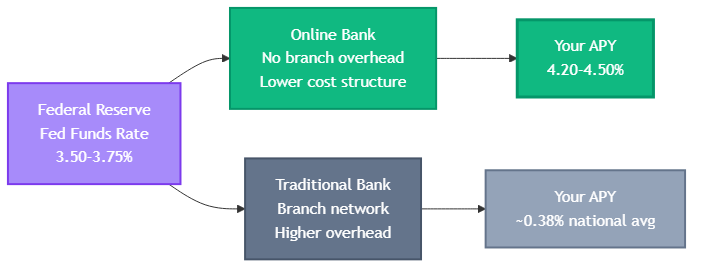

For most of the 2010s, this question didn’t really come up. The Fed funds rate sat near zero, the best HYSAs paid maybe 1%, and the gap between “good” and “average” wasn’t worth the effort of opening a new account. That changed when the Fed started hiking in 2022. The target range peaked at 5.25–5.50% and has since drifted down to 3.50–3.75% as of the April 29, 2026 FOMC — still meaningfully above the zero-rate era and high enough that the spread between a real HYSA and a generic bank savings account is now structural, not a rounding error.

Who’s leaving the most money behind? Anyone holding an emergency fund or cash buffer at a traditional bank. The math, using current rates:

| Cash balance | Standard savings (0.38%) | HYSA (4.20%) | Annual difference |

|---|---|---|---|

| $10,000 | $38 | $420 | +$382 |

| $20,000 | $76 | $840 | +$764 |

| $50,000 | $190 | $2,100 | +$1,910 |

At a top HYSA paying 4.50%, the gap on $20,000 stretches to roughly $824 a year. None of this requires you to invest, take risk, or lock the money up. It’s the same dollars, in a different account, with the same FDIC insurance. The only “work” is the one-hour setup.

One caveat worth surfacing up front: the rate is variable. When the Fed cuts, your HYSA APY drops with it — often within a week of the announcement. The current 3.50–3.75% target is below the 2024 peak, so further compression is plausible. That doesn’t break the case for using a HYSA; it just means the gap is widest when rates are elevated, like now.

How a HYSA actually works

What is a HYSA, technically?

Mechanically, a HYSA is the same product as your bank’s regular savings account: an FDIC-insured deposit, accessible by ACH transfer, no fixed term. The reason the APY is higher comes down to the bank’s cost structure. Online-only banks — Ally, Marcus by Goldman Sachs, SoFi, Discover, American Express — don’t operate branches. No tellers, no leases on retail real estate, no marble lobbies. The cost they save on overhead gets passed back to depositors as a higher interest rate.

Current top-of-market rates (verified May 2026): Ally Bank at 4.20% APY, Marcus by Goldman Sachs at 4.25%, American Express Personal Savings at 4.25%, and SoFi at 4.50% — though SoFi’s headline rate requires recurring direct deposit; without it, the APY drops to 1.20%. Always check the conditions before opening.

APY vs APR — the compounding distinction

Banks quote two different numbers and they aren’t the same. APR (annual percentage rate) is the simple yearly rate. APY (annual percentage yield) bakes in the compounding frequency — so a 4.25% APR that compounds daily becomes a slightly higher effective APY, because each day’s interest earns interest the next day. Most HYSAs compound daily and credit interest monthly. The number you see advertised — “4.20% APY” — already includes the compounding boost, which is why APY is the apples-to-apples figure for comparison. If a bank quotes only an APR, ask for the APY before signing up. The Luna3 explainer on how daily compounding actually adds up walks through the math.

FDIC insurance on online banks

This is the most common safety question, and the answer is short: FDIC insurance covers up to $250,000 per depositor, per insured bank, per ownership category — and online banks are insured the same way as every brick-and-mortar bank in the country. The deposit-insurance fund doesn’t distinguish between a branch network and an app. If the bank fails, you’re made whole up to the limit, typically within a few business days.

Two practical notes. First, the $250K limit applies per ownership category — single account, joint account, trust, business — so a couple with a joint account at one bank is covered up to $500K. Second, if you’re a fintech app user, check whether the app is itself a bank or just a “deposit sweep” partner of one. Real HYSAs make this clear in the fine print.

Opening one is genuinely fast: a soft credit check (no FICO hit), a link to an existing checking account, and a first ACH transfer that lands in one to three business days. No minimum deposit at most providers. Once it’s funded, you can pull money back to your checking account at any time.

Where beginners get confused

Four traps to know about before you open an account.

1. Teaser rates that drop. A few banks advertise a promotional rate for the first three months, then quietly drop to a lower ongoing APY. The headline number on the homepage isn’t always the rate you’ll be earning in month four. Read the asterisk; look for the “ongoing APY” disclosure. The big online banks (Ally, Marcus, AmEx) generally publish a single rate that applies to all balances, which is what you want.

2. Variable means variable. A HYSA APY tracks the Fed’s policy rate. When the Fed cuts 25 basis points, your APY typically drops by something close to that within days. There’s no contractual rate — banks change it whenever they want. This is different from a certificate of deposit (CD), where the rate is locked for the term. For an emergency fund you want liquid, the variable rate is the right tradeoff; for cash you don’t need to touch for 12+ months, a CD or short-dated T-bill might pay better.

3. Withdrawal limits that shouldn’t still exist. Federal Regulation D used to cap savings-account withdrawals at six per month. The Federal Reserve eliminated that limit in April 2020. But many banks still enforce six-per-month as their own policy — and may charge an excess-withdrawal fee or convert your account to checking if you breach it. Read your bank’s specific terms. For an emergency fund that’s only touched in actual emergencies, this is rarely a problem; for an account you’re sweeping cash through monthly, check the rules.

4. “Your bank’s HYSA” vs a standalone online bank. Most big national banks — Chase, Bank of America, Wells Fargo — offer a product called a “high-yield savings account” that pays meaningfully less than a real online bank. The product name doesn’t guarantee the rate. If the APY on your bank’s HYSA is under 1%, it isn’t really a high-yield account; it’s a marketing label. The 4%+ rates are at the online-only and digital-first banks listed above.

Going deeper

Once your HYSA is funded and your emergency cushion is sized appropriately, the next questions shift from “where do I park cash” to “when do I stop holding cash at all”:

- For the math on how a 4.20% APY actually grows over years, read our explainer on how daily compounding actually adds up.

- Once your cash balance gets large enough to compare T-bills and short-term bonds — usually past the $25K mark — the choice gets more interesting. We covered when T-bills and short-term bonds become worth comparing separately.

- And if you’re trying to figure out how much cash to keep liquid before investing the rest, that’s a different framework — the 4% rule gives you a starting answer.

The honest summary: a HYSA isn’t a clever financial product. It’s the same savings account you already have, at a bank that doesn’t pay for retail branches and passes the savings along. The reason it matters in 2026 is that the gap between “default” and “best” has widened to roughly $400–$2,000 a year on a typical cash balance — and that gap exists for the entire time rates stay elevated. The opportunity isn’t going to wait for you to get around to it.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!