- Canlon paid ¥483.2M for 51% of Suzhou Jiazhi Cai Optoelectronics in 2025, adding ¥298M in display equipment revenue and turning the company GAAP-profitable.

- Non-GAAP operations still lost over ¥55M; H2 2025 was a –5.4M loss after H1 booked ¥25.8M — the turnaround narrative is front-loaded.

- At 266x P/E with the core waterproofing business shrinking 14% year-on-year, the market is pricing in flawless multi-year execution before the numbers prove it.

The Canlon display pivot is one of the cleanest single-name case studies of China’s industrial-to-tech rotation. Jiangsu Canlon Building Materials Co., Ltd. (300715.SZ) was a sleepy ChiNext-listed waterproofing manufacturer until January 2025, when it disclosed a ¥483M bid for a Suzhou display panel detection equipment maker. The stock went from a 52-week low of ¥9.30 to a high of ¥22.57 — a 143% trough-to-peak run — and last printed at ¥21.62 going into publication on May 27, 2026, with a price-to-earnings ratio of 266 times. Market cap: ¥8.01B CNY.

Here’s the question worth answering: is this a real transformation, or a re-rating that has run well ahead of what the financials actually show?

What Canlon paid for — the January-to-April 2025 acquisition

The acquisition timeline matters because it sets the bar for the H1/H2 2025 split that comes later. Canlon disclosed its intent to acquire Suzhou Jiazhi Cai Optoelectronics Technology Co., Ltd. on January 7, 2025. The formal binding agreement was filed with the Shenzhen Stock Exchange on April 3, 2025 (announcement #2025-012). Business registration completed on April 28, 2025. The final price was ¥483.1852M (within a ¥510M cap disclosed at the intent stage) for a 51% stake.

Two structural details from the filing matter more than the price. First, Jiazhi Cai’s controlling shareholders — Guisi Caiguang and Chen Xianfeng — agreed to a binding performance commitment: Jiazhi Cai’s net profit must be at least ¥55M in 2025, ¥75M in 2026, and ¥110M in 2027 (cumulative ¥240M across three years). If those targets are missed, the counterparties must compensate Canlon in cash or shares. This is the closest thing to a guarantee that an M&A deal in China can provide.

Second, Canlon’s own controlling shareholders simultaneously transferred 14.4852% of Canlon’s outstanding shares (53.63M shares) to Chen Xianfeng and Suzhou Silica Optoelectronics — a cross-shareholding alignment that makes Jiazhi Cai’s controlling shareholder a substantial owner of Canlon at the same time as Canlon acquires Jiazhi Cai. In early 2026, SZSE filing 2026-002 announced a further 18% stake acquisition; if approved and closed, Canlon would hold 69% of Jiazhi Cai, tightening the alignment further.

In other words: this isn’t a clean takeover with a separate management team. It’s a co-investment structure where the two camps are now financially intertwined.

What Suzhou Jiazhi Cai actually does

Jiazhi Cai was founded in November 2017 and operates in display panel detection and repair equipment — industrial machines that scan LCD and OLED panels coming off production lines, identify defects, and where the defect is repairable, fix the panel rather than scrap it. The customers are the names that matter in Chinese display: BOE Technology Group and TCL CSOT together account for over 37% of global display production capacity by area. As Chinese fab capacity expands and quality requirements tighten, demand for domestic detection equipment is structural rather than cyclical.

The market is growing — multiple research firms cite mid-to-high single-digit annual growth through the early 2030s, though the specific dollar figures vary widely depending on what’s included in the definition. The directional point matters more than the precise number: BOE and TCL CSOT are building, and they prefer domestic suppliers for politically sensitive supply chain decisions. We’ve covered the broader display + memory supply chain in our deep-dive on HBM memory and the AI infrastructure bottleneck and the related DRAM pricing cycle piece.

The competitive set is dominated by Korean firms: HB Tech, Yang Electronic, and KOH YOUNG all have established positions in Asian display fabs. Domestic Chinese competitors include Suzhou HYC Technology and Suzhou UB Precision. Jiazhi Cai is a smaller domestic player — not the market leader, but with proximity advantages and a customer roster that aligns with where the next decade of Chinese display capex is going.

The Canlon display pivot — what the 2025 numbers actually show

2025 results published on April 24, 2026 read as a turnaround on the surface. Revenue: ¥2.410B (+1.26% year-on-year). GAAP net profit: ¥20.4M (+103.79% year-on-year — a flip from prior-year losses). Operating cash flow: ¥266M (+289.53% year-on-year). Gross margin: 21.58% (+1.74 percentage points year-on-year). The 2025 annual report summary hits every metric the bull case needs.

Read the half-yearly cadence and the story changes.

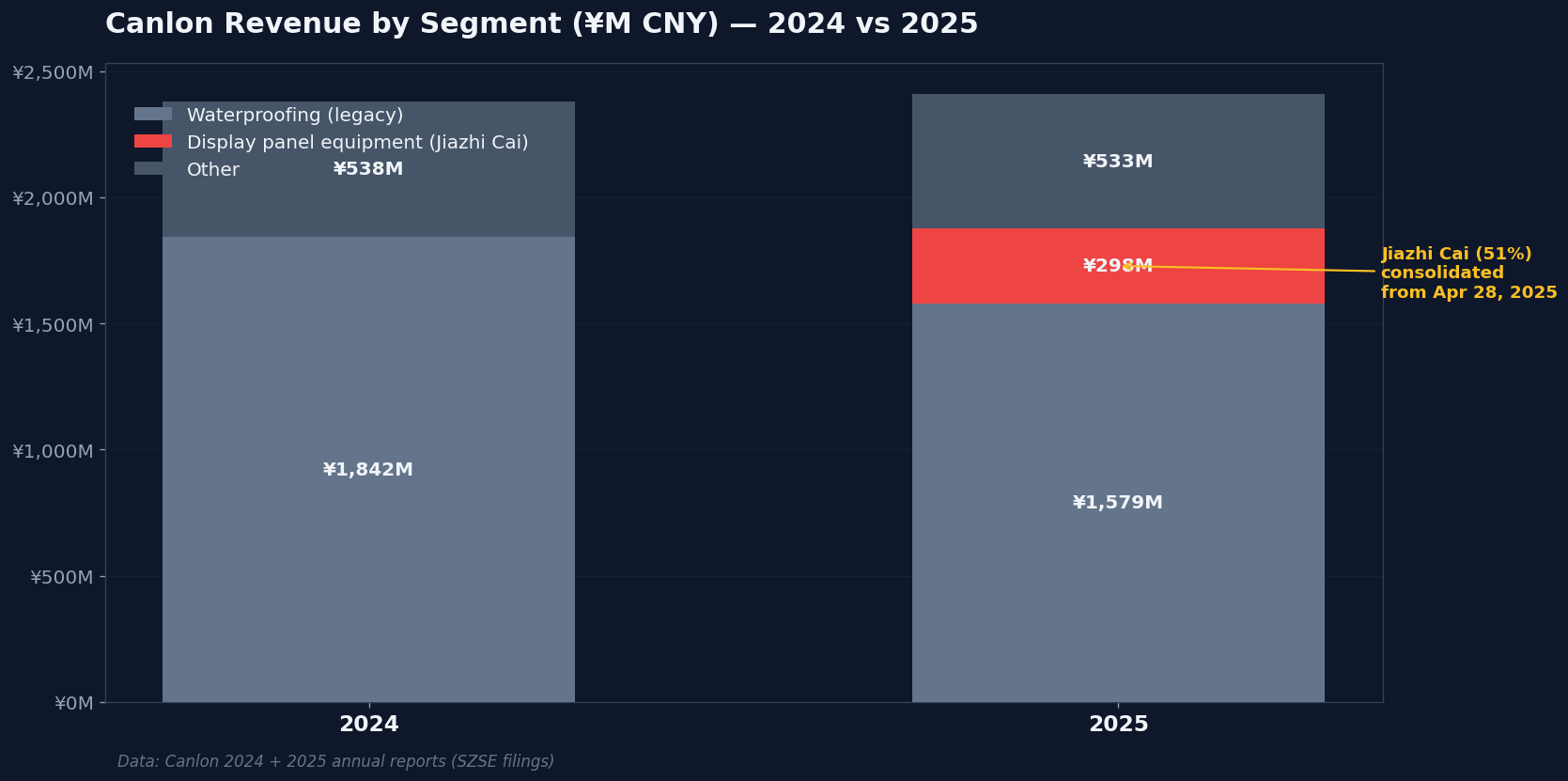

H1 2025 net profit was ¥25.8M (announcement #2025-057). Jiazhi Cai was consolidated for roughly two months of H1 (from late April onward). H2 2025 net profit therefore equals the full year minus H1, or ¥20.4M – ¥25.8M = –¥5.4M (a loss). H2 2025 was a net loss, despite Jiazhi Cai being consolidated for the entire six-month period.

The non-GAAP figure tells a similar story. The Stockstar coverage of the 2025 annual report headlines that adjusted net profit (扣非净利润, which excludes one-time gains, government subsidies, and other non-recurring items) is “still losing more than ¥55M.” So Canlon’s underlying business operations lost ¥55M+ on a non-GAAP basis in 2025, even with Jiazhi Cai included.

What does this imply if Jiazhi Cai hit its ¥55M performance commitment on a stand-alone basis? Canlon’s 51% share of that would be roughly ¥28M attributable. A consolidated group non-GAAP loss of ¥55M+ would then mean the waterproofing business plus Canlon-level corporate adjustments contributed approximately –¥83M of non-GAAP losses on its own. The waterproofing segment is the drag, not the support.

The segment data confirms this. Waterproofing revenue in 2025 was ¥1.579B, down 14.29% year-on-year and accounting for 65.52% of total group revenue. Display panel equipment was ¥298M, or 12.37% of revenue, contributed across an effective seven-month consolidation window (May through December). On an annualised basis, Jiazhi Cai would contribute roughly ¥510M to full-year 2026 group revenue — adding meaningfully to growth, but not yet enough to offset the structural decline in the legacy business.

Q1 2026 results show some improvement off the H2 trough: revenue ¥523M (+12.36% year-on-year), net income ¥14.49M (+118.94% year-on-year). The first full quarter with Jiazhi Cai included in the prior-year comparable is starting to flatter the growth optics. R&D spend was ¥117M, or 4.86% of revenue — a healthy intensity for a company in the middle of repositioning. The debt-to-asset ratio at 63.95% is elevated, reflecting the cash-funded acquisition.

The bear case — what 266x earnings actually requires

At a current market cap of ¥8.01B and trailing twelve-month GAAP net profit of ¥20.4M, Canlon trades at roughly 266 times earnings. Industry context: Chinese industrial peers with no tech-pivot story tend to trade at 10–20x, depending on growth and balance sheet. Display equipment specialists with proven contracts and consolidated profitability typically trade at 25–40x in Asia. The detection equipment leaders — KOH YOUNG, HB Tech — trade closer to 20x earnings.

For Canlon’s multiple to compress to 30x — a level a successful pivot might justify — net profit would need to grow approximately ninefold to around ¥185M. That requires the display segment to scale to roughly ¥2B in revenue at mid-teens net margins (Jiazhi Cai’s current 100% basis run-rate is around ¥600M), or some combination of display scale plus waterproofing recovery. Neither of those is impossible. Both would take multiple years to play out.

The bear case isn’t that the pivot won’t work. It’s that the market is pricing in a flawless multi-year execution sequence before any of it shows up in the numbers. Three specific things would invalidate the bull thesis.

First, the H2 2025 net loss isn’t an isolated print. If H2 2026 also turns negative despite a full year of Jiazhi Cai consolidation, the operational leverage argument breaks. The H1/H2 cadence in 2026 is the cleanest test.

Second, the non-GAAP gap doesn’t close. GAAP profit inflated by non-recurring items is not what a 266x multiple is supposed to capitalise. Adjusted profitability needs to turn positive before any fundamental valuation argument holds.

Third, Jiazhi Cai’s 2025 ¥55M performance commitment was missed. If Chen Xianfeng and Guisi Caiguang have to compensate Canlon in cash or shares, it confirms the seller-side projections were too optimistic, and the 2026 (¥75M) and 2027 (¥110M) targets get re-rated downward in the market’s mind.

The legacy waterproofing business is a separate concern. Polymer membranes (MBP, PVC, TPO) — Canlon’s bread and butter — are a structurally challenged category as Chinese real estate completions decline. A –14% revenue print is not a cyclical low; it’s the trend. The display tech pivot needs to outrun a shrinking base.

What we’re watching

The 2026 trajectory will resolve most of this. Five specific things to track, ranked by load-bearing weight.

Jiazhi Cai’s 2025 ¥55M performance commitment outcome. The cleanest test. Canlon’s 2025 annual report should disclose whether Jiazhi Cai hit the target on a stand-alone basis. If yes, the bull case has a real anchor. If no, watch for the compensation disclosure.

Display segment revenue share in H1 2026. Should exceed 20% of group (up from 12.37% in 2025) for the re-rating to be sustained. The first half of 2026 will be the first six-month period with Jiazhi Cai in the prior-year comparable base, so the growth print will be clean.

Non-GAAP net profit turning positive at the group level. The –¥55M+ adjusted loss is the bear case in one number. Watch for it to flip. Anything less than a clearly positive non-GAAP print in 2026 keeps the valuation argument paper-thin.

Named customer wins disclosed via SZSE filing. Specific BOE or TCL CSOT contract announcements would substantiate Jiazhi Cai’s competitive position. Generic statements about “deepening industry relationships” don’t move the needle.

The 2026-002 follow-on 18% stake closing. If approved and completed, Canlon would hold 69% of Jiazhi Cai, raising the alignment with Chen Xianfeng’s incentive structure and making Jiazhi Cai the dominant earnings engine. Watch for the completion disclosure.

The Canlon display pivot will eventually resolve in one of two directions. Either the 2026–2027 numbers vindicate the re-rating, or the H2 2025 pattern persists and the multiple normalises downward. The market has placed its bet at 266 times earnings. The numbers have a few quarters to catch up.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings (like 300715) and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!