- The 50/30/20 rule assumes your needs fit in half your income — but once housing passes the 30% cost-burdened line, needs overrun the bucket and the math stops working.

- Cash flow budgeting flips the order: pay yourself first, automate savings and investing off the top, then spend what is left — no line-item tracking required.

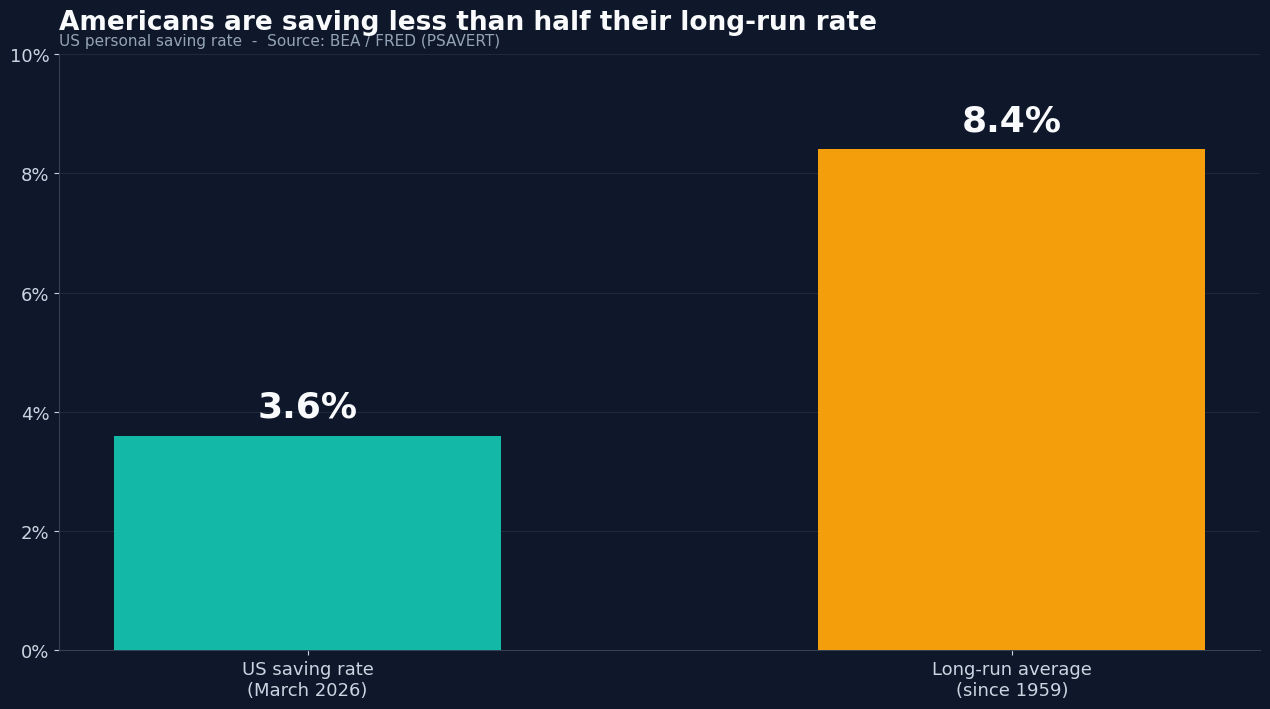

- Your savings rate is the one number that matters. The US average has fallen to 3.6%, less than half the long-run 8.4%.

Cash flow budgeting starts from a blunt fact: the budgeting rule almost everyone quotes no longer fits the math. The 50/30/20 rule — half your take-home on needs, 30% on wants, 20% to savings — assumes your essentials comfortably fit inside half your income. In 2026, for a lot of people, they don’t. Say you bring home $5,000 a month. The rule says $2,500 covers every need. But if your rent alone is $1,700, that’s already 34% of your take-home — past the 30% line the government uses to call a household “cost-burdened” — and you still haven’t paid for food, insurance, or getting to work. When needs blow past 50%, the rule can only balance if savings drops to zero. So millions of people quietly let it.

Why the 50/30/20 rule stopped working

The 50/30/20 rule isn’t a bad idea — it was a great one. Senator Elizabeth Warren and her daughter Amelia Warren Tyagi popularised it in their 2005 book All Your Worth, and its genius was simplicity: three buckets, no spreadsheet. The problem is the assumption baked into the first bucket. It only works if “needs” fit in 50% of after-tax income.

That assumption has quietly broken. The federal government considers a household “cost-burdened” once housing eats more than 30% of income, and a large and growing share of households are over that line. Stack food, insurance, and transportation on top, and the needs bucket routinely runs well past half of income for renters and recent buyers. There’s simply no version of “needs at 60%, wants at 30%, savings at 20%” that adds up to 100%.

Most budgeting guides respond by handing you a new ratio — 60/30/10, 70/20/10, pick your inflation. But that misses the real issue. A ratio is still a category-policing system: it asks you to sort every dollar into a bucket and check the percentages at month’s end. That takes willpower, every month, forever — and willpower is exactly the thing that runs out. The proof is in the national numbers: the US personal saving rate has fallen to 3.6%, which is what “save whatever’s left” produces in practice.

How cash flow budgeting actually works

Here’s the reframe: stop budgeting like a household policing its categories, and start managing money the way a business manages cash flow. A company doesn’t agonise over every coffee. It pays its obligations, reinvests a target slice of revenue first, and lets the rest fund operations. You can run a paycheck the same way.

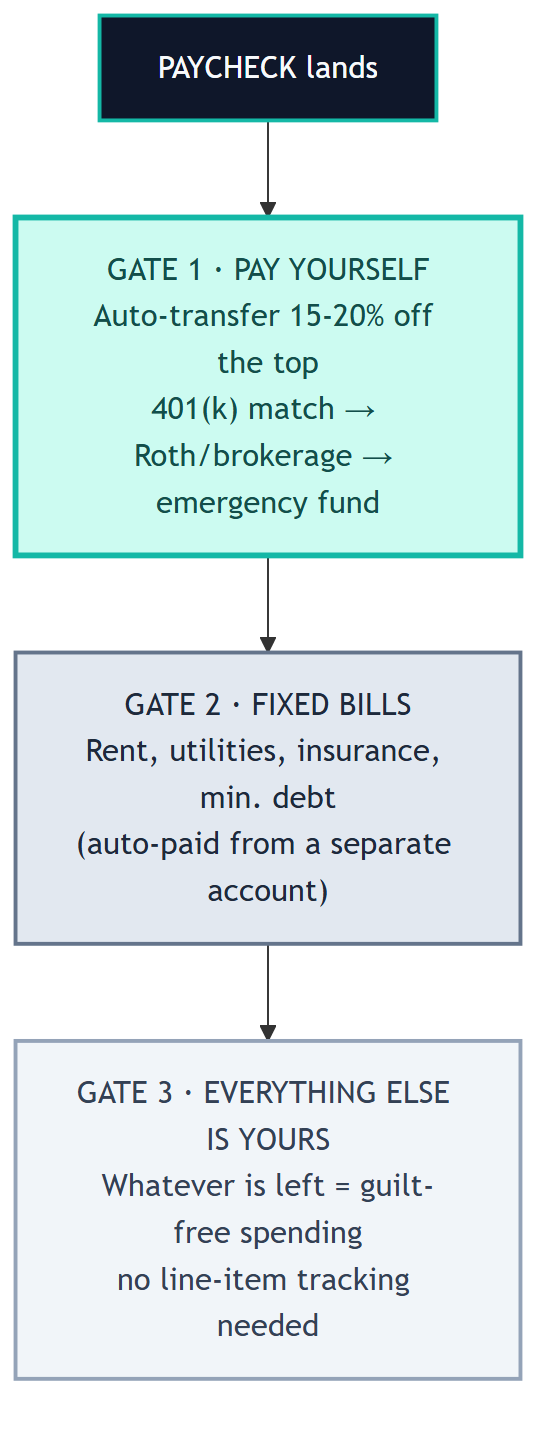

The method has a plain-English name: pay yourself first (sometimes called reverse budgeting). Instead of saving what’s left after you spend, you save first and spend what’s left. The trick is that you don’t rely on remembering to do it — you automate it. Think of it as a waterfall: the moment your paycheck lands, the money flows through three gates, in order.

Gate 1 — Pay yourself (automated, off the top). An automatic transfer moves your savings-and-investing target out before you can touch it: enough in your 401(k) to capture the full employer match, then your Roth IRA or brokerage auto-investment, then a top-up to your emergency fund. A common target is 15–20% of take-home, but the right number is whatever you can sustain — more on that below.

Gate 2 — Fixed bills (automated). Rent, utilities, insurance, and minimum debt payments auto-pay from a dedicated account, ideally separate from your spending account — so the balance you actually see is money you’re free to spend.

Gate 3 — Everything else is yours. Whatever’s left in checking after Gates 1 and 2 is guilt-free spending. No line items, no app logging every latte. If the money is there, you can spend it — because the saving and the bills already happened.

The reason this works where category budgets fail is that it removes the monthly decision. You set the automation once, and discipline becomes a default instead of a willpower test you have to pass thirty times a month.

It also collapses your whole financial life down to one number worth watching: your savings rate — the share of take-home you save and invest, or (saved + invested) ÷ take-home. Think of it as your personal free-cash-flow margin, the same metric an analyst uses to judge whether a company is building value or just running in place. A household saving 20% is on a fundamentally different trajectory than one saving 3%, regardless of what either spends on coffee. Track that one number and you can ignore the other forty.

The 2026 numbers

None of this makes the old ratios useless — they’re fine as a sanity check on the spending side. The shift is which number you treat as fixed. In category budgeting, savings is the leftover. In cash flow budgeting, your savings rate is the fixed input and spending is the leftover. If you want a target ratio that fits 2026 reality, here’s the menu:

| Framework | Needs | Wants | Save / Invest | Best for |

|---|---|---|---|---|

| 50/30/20 (classic) | 50% | 30% | 20% | Lower cost-of-living; the original target |

| 60/30/10 | 60% | 30% | 10% | High rent / high inflation |

| 70/20/10 | 70% | 20% | 10% | Expensive metros, tight cash flow |

| Pay-yourself-first | leftover | leftover | 15–20% locked FIRST | Anyone who’d rather automate than track |

The reason the method matters more than the ratio is in the data. The US personal saving rate was just 3.6% in March 2026 — less than half the 8.4% long-run average going back to 1959. Only 47% of Americans say they could cover a $1,000 emergency, and just 30% could pay it from savings, per Bankrate’s 2026 survey. Revolving credit-card debt sits at $1.25 trillion. This is the cost of “save what’s left”: for most households, nothing is.

Where people go wrong

Even with the right system, a few mistakes show up again and again.

Saving whatever’s left. The single most common one — and the whole point of paying yourself first. If saving isn’t automatic and first, it competes with spending, and spending wins.

Confusing budgeting with tracking. You do not need to log every coffee. If your saving and bills are automated, the leftover in checking is already your spending limit. Over-tracking is the leading reason people quit budgeting entirely; automation is what makes the tracking optional.

Investing before you have a buffer. Order matters. A small starter emergency fund comes before investing, then the 401(k) match (it’s free money), then paying down high-interest debt, then long-term investing. Skip the buffer and the first flat tire lands on a credit card at 24%.

Treating 20% as a law. If you can’t hit 20% yet, that’s fine — start at a rate you can actually sustain and ratchet it up. The most painless way is to save the raise: each time your income rises, route most of the increase straight into Gate 1 before lifestyle creep absorbs it. A savings rate that climbs from 5% to 15% over a few years beats a 20% target you abandon in month two.

Going deeper

The cash you set aside in Gate 1 needs somewhere to sit and somewhere to grow. Our explainer on high-yield savings accounts covers where the emergency-fund slice belongs, and what a 401(k) is walks through the employer match that should be your very first automated transfer. For the long-term end of the waterfall, the 4% rule shows what that savings rate is ultimately building toward.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!