Now I have the macro context. Let me write the post.

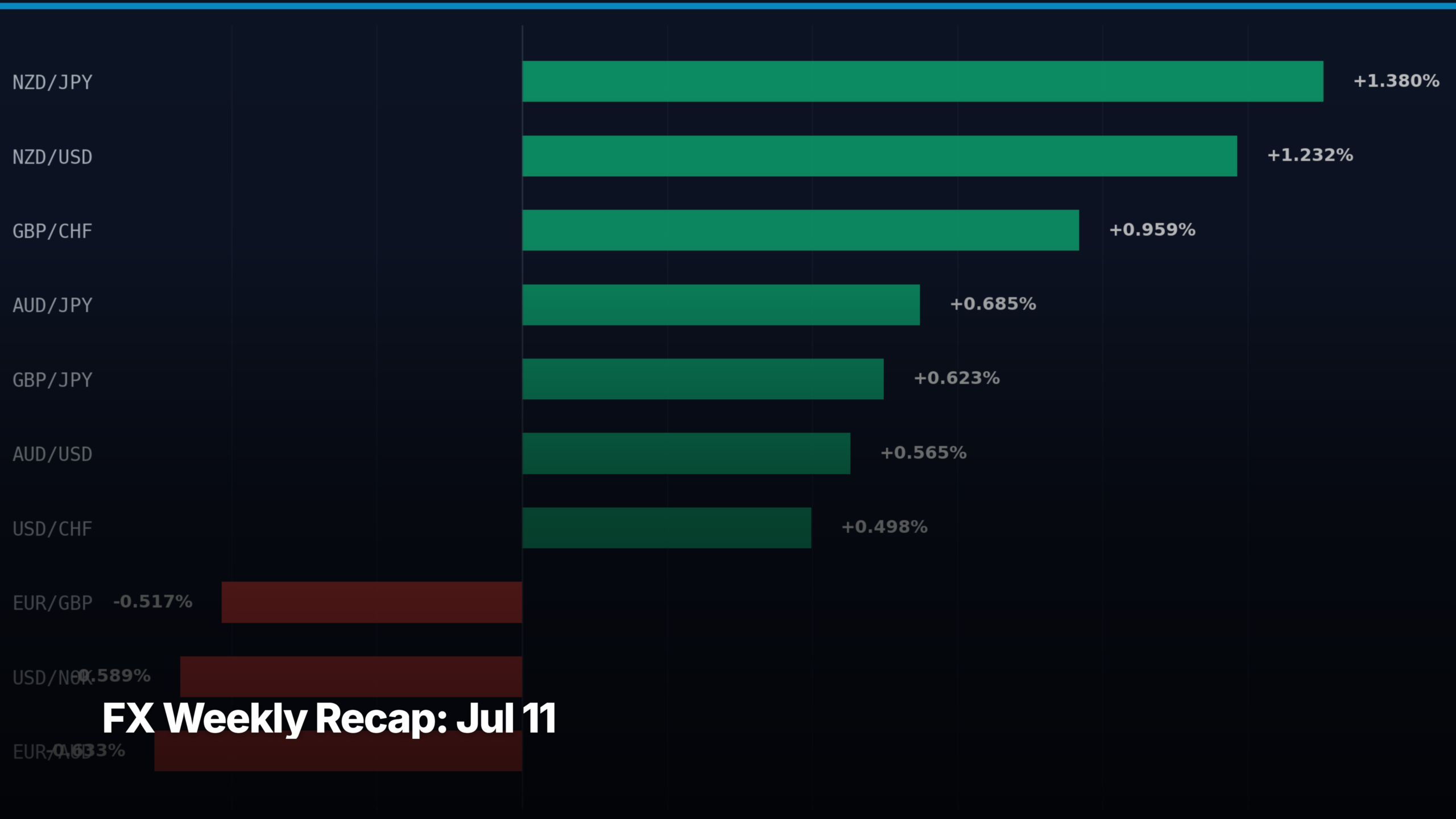

- NZD led G10 after RBNZ hiked to 2.50% — NZD/USD +1.23%, NZD/JPY +1.38% for the week

- Oil surged (Brent +5.85%) on US-Iran strikes and Hormuz disruption, lifting NOK and the commodity bloc

- DXY flat at 101 (+0.10%) — US CPI on July 14 is the next catalyst for dollar direction

The Week in the Dollar

The dollar index closed the week at 101, up a negligible 0.10%, as two opposing forces cancelled each other out: safe-haven demand from the US-Iran military escalation versus softer rate expectations after the June FOMC minutes showed no urgency to hike. The result was a flat week for the greenback that masked sharp moves underneath.

The real action was in the commodity complex. Brent crude surged 5.85% to $76 and WTI jumped 4.11% to $71.51 after US strikes on Iran and threats to reimpose the Strait of Hormuz naval blockade. That shock rippled straight into FX: USD/NOK dropped 0.59% as Norway’s petro-linked krone caught the bid, while USD/CAD slipped 0.27%. Copper’s 2.79% rally supported AUD/USD, which gained 0.57% to 0.6955. Gold’s modest 0.39% gain to $4,129 reflected a muted safe-haven impulse — the yen barely moved, with USD/JPY drifting to 161.67 (+0.14%), suggesting carry appetite remained intact despite the geopolitical flare-up.

Key Pair Breakdown

NZD/USD — 0.5763, +1.23%. The week’s standout performer. The RBNZ hiked the OCR to 2.50% on Wednesday — the first increase in three years — and did it unanimously. That consensus surprised markets that remembered May’s deadlocked 3-3 vote. The kiwi rallied hard against the flat dollar, reclaiming the 0.5750 handle. Next resistance sits near 0.5800; a push through there targets the 0.5850 zone last tested in early June.

NZD/JPY — 93.158, +1.38%. The biggest mover on the board this week, combining NZD rate-hike strength with persistent yen weakness. The BoJ remains the outlier dove among G10 central banks, and the carry trade into high-yielders like NZD continues to find buyers. The pair is pressing toward 94 — a level that historically draws verbal intervention noise from Japanese officials, though none materialised this week.

Week Ahead Setup

Tuesday’s US CPI print for June is the week’s defining event. Headline inflation ran at 4.2% in May; consensus points to a pullback toward 3.9%. A miss in either direction moves the dollar and resets rate-cut expectations for the back half of the year. A soft print would likely extend the commodity-bloc rally — AUD/USD is already knocking on 0.70, and NZD/USD has room to push toward 0.58.

The oil story isn’t finished. If Hormuz disruption escalates, Brent above $80 drags NOK and CAD higher while feeding into the next round of inflation prints globally. Watch EUR/USD around 1.1420 — it went nowhere this week (-0.03%) and needs CPI to break the range. GBP/USD at 1.3398 (+0.45%) has quietly strung together a second week of gains; UK jobs data on Tuesday could extend the move toward 1.3450.

Bottom Line

FX markets spent the week absorbing an oil shock and an RBNZ hike while the dollar stayed flat — a holding pattern that breaks the moment Tuesday’s CPI lands. NZD/JPY at 93.16, where rate divergence meets carry momentum, is the pair traders are most likely watching into next week.

Read next: FX Markets · How to Read the COT Report · What Is a Bond?

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!