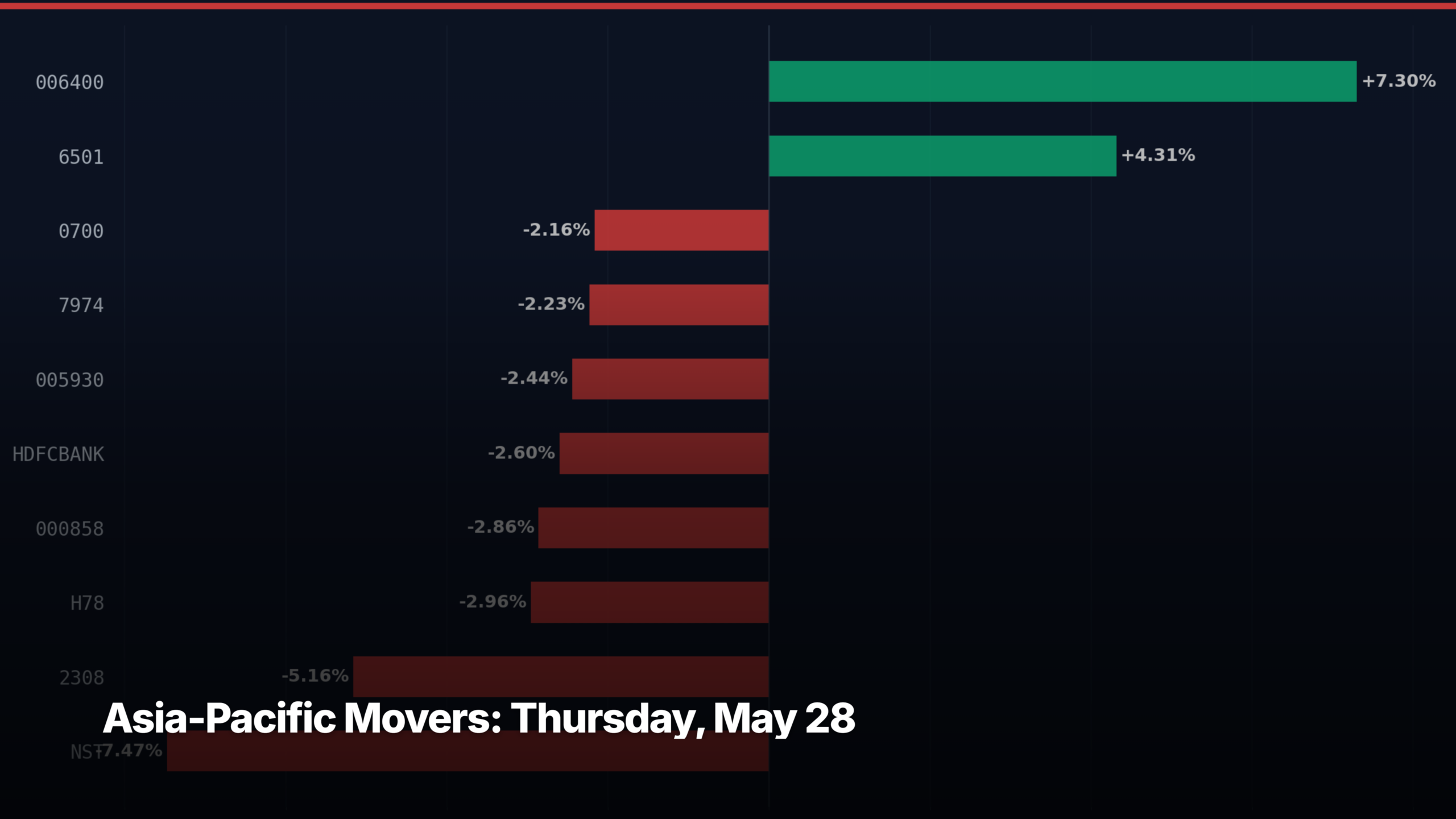

- NST led Australia with a -7.47% move on 2026-05-28

- Covered 10 exchanges — 9 with notable gainers, 10 with notable decliners

- Includes ASX, HKEX, mainland China, TSE, SGX, KOSPI, TWSE, NSE, and NZX coverage

Here are the standout movers across Asia-Pacific’s major exchanges for the session of Thursday, May 28, grouped by market.

Australia (ASX)

↑ WES +1.19%

Large-cap · 78.48 (local)

Why: Wesfarmers ticked higher with no clear single catalyst — likely defensive rotation into quality consumer names as broader ASX traded steady around session highs.

Pattern: Looks like low-beta momentum continuation in a defensive large-cap; isolated move rather than part of a sector-wide thrust, consistent with grind-higher behaviour.

↓ NST -7.47%

Mid-cap · 18.2 (local)

Why: Northern Star slid after walking away from the Egina Gold Project, handing full control back to Novo — market read it as a strategic retreat on a key growth asset.

Pattern: Sharp single-name catalyst drop — looks like event-driven gap rather than sector rotation, since broader ASX gold peers did not show the same magnitude of move.

Hong Kong (HKEX)

↑ 1810 +0.56%

Large-cap · 28.56 (local)

Why: Xiaomi edged higher despite a bearish Jefferies note flagging smartphone margin pressure — buyers shrugged it off, possibly leaning on the EV and AIoT growth story.

Pattern: Mild bid against negative sell-side flow looks like dip-buying or short-cover; isolated rather than tracking a broad Hang Seng tech rally given Tencent traded sharply lower.

↓ 0700 -2.16%

Mega-cap · 425 (local)

Why: Tencent fell despite a headline PayPal–WeChat Pay tie-up — investors likely focused on ByteDance’s reported $70B AI capex plan, which intensifies competitive pressure on Tencent’s cloud and AI spend.

Pattern: Looks like mean-reversion off recent highs combined with a competitive-threat repricing; weighs on the wider Hang Seng Tech complex rather than a clean single-name story.

China — Shanghai (SSE)

↑ 600036 +0.32%

Large-cap · 37.12 (local)

Why: China Merchants Bank crept higher with no fresh catalyst — likely steady rotation into mainland banks as defensive yield plays while growth names lagged.

Pattern: Low-volatility drift higher in a large-cap bank fits a slow rotation pattern; isolated rather than part of a broad SSE rally, consistent with mainland defensive positioning.

↓ 600519 -2.07%

Mega-cap · 1276 (local)

Why: Kweichow Moutai dropped with no clear headline — likely continued de-rating of premium baijiu as soft consumption data and weak banquet demand keep weighing on the sector.

Pattern: Looks like momentum continuation lower in China consumer-luxury — part of the ongoing premium-spirits theme rather than an isolated single-name catalyst.

China — Shenzhen (SZSE)

↑ 002594 +0.69%

Large-cap · 95.88 (local)

Why: BYD nudged higher as Europe EV registrations jumped 38% with Chinese brands gaining share, and as the company is reportedly weaning itself off supply-chain finance — both incremental positives.

Pattern: Modest follow-through fits sector-rotation into China EV exporters; broader theme as European EV demand re-accelerates and Tesla rebounds also help sentiment.

↓ 000858 -2.86%

Large-cap · 81.49 (local)

Why: Wuliangye dropped without a single headline — premium baijiu peers like Moutai also weakened, suggesting the move tracks ongoing concern about high-end liquor demand in China.

Pattern: Coordinated weakness with Moutai signals sector-wide momentum continuation lower in premium consumer — not isolated, fits the broader baijiu de-rating theme.

Japan (TSE)

↑ 6501 +4.31%

Large-cap · 5174 (local)

Why: Hitachi jumped after announcing it will build an AI platform for software-defined vehicles with subsidiary Astemo — investors read it as a fresh AI-monetisation lever in the auto stack.

Pattern: Looks like a catalyst-driven breakout in a Japanese AI-adjacent industrial; fits the broader ‘AI-meets-traditional-industry’ theme that has lifted Japanese large-caps.

↓ 7974 -2.23%

Mega-cap · 6972 (local)

Why: Nintendo slid with no fresh headline — likely profit-taking after recent strength, with no Switch 2 update flow to drive incremental buying.

Pattern: Mean-reversion off recent highs in a mega-cap consumer-tech name; isolated rather than part of broad Topix weakness, consistent with sentiment cooling post-run.

Singapore (SGX)

↑ C6L +0.90%

Mid-cap · 6.7 (local)

Why: Singapore Airlines rose modestly with no specific catalyst — likely benefiting from continued resilience in Asia travel demand and steady jet-fuel cracks.

Pattern: Quiet drift higher in a mid-cap airline fits low-beta momentum continuation; isolated SGX move, not part of a broad regional travel-stock surge.

↓ H78 -2.96%

Mid-cap · 7.54 (local)

Why: Hongkong Land fell with no clear catalyst — likely tracking the broader Hang Seng property weakness as China commercial real estate sentiment stayed soft.

Pattern: Move fits the ongoing HK/China property downtrend — momentum continuation lower in a regional landlord, not an isolated Singapore-specific event.

South Korea (KOSPI)

↑ 006400 +7.30%

Mid-cap · 6.76e+05 (local)

Why: Samsung SDI surged with no clear single headline — likely a sharp re-rate on improving EV battery sentiment after strong European EV registration data lifted the entire Korean battery complex.

Pattern: Looks like a momentum breakout on a sector-rotation theme into Asian EV battery names; broader move beyond a single catalyst, fits Europe-EV-demand spillover.

↓ 005930 -2.44%

Mega-cap · 2.995e+05 (local)

Why: Samsung Electronics fell on coverage flagging Android takes a bigger hit than Apple from AI memory shortages, even as a generous worker pay deal and Micron’s gains highlight HBM competitive pressure.

Pattern: Looks like macro-catalyst weakness within the AI-memory complex — Samsung lagging Micron/SK Hynix in HBM fits the broader ‘losing share in the AI build-out’ theme, not isolated.

Taiwan (TWSE)

↓ 2308 -5.16%

Mid-cap · 2390 (local)

Why: Delta Electronics fell sharply with no clear headline — likely profit-taking in Taiwan AI-server power supply names after a strong run, possibly tracking TSMC-led tech weakness.

Pattern: Looks like mean-reversion off extended highs in an AI-infrastructure beneficiary; part of broader Taiwan AI-supply-chain cooling rather than an isolated company event.

India (NSE)

↑ TCS +0.35%

Mega-cap · 2284 (local)

Why: TCS edged higher after launching its SovereignSecure Cloud for European public sector clients and on news India is testing core banking and Aadhaar systems against AI threats — both supportive for IT services demand.

Pattern: Mild positive drift on incremental new-business signals; isolated single-name story rather than a broad Nifty IT rally, consistent with quiet accumulation.

↓ HDFCBANK -2.60%

Mega-cap · 758.7 (local)

Why: HDFC Bank dropped after media reports flagged a $4.71M allegedly-disguised payment to a state-owned board to attract large deposits — a governance/optics overhang that hit sentiment.

Pattern: Catalyst-driven single-name selloff with headline risk; isolated rather than reflecting broader Indian bank weakness, since metals and other Nifty names rallied.

New Zealand (NZX)

↑ SPK +1.82%

Mid-cap · 1.96 (local)

Why: Spark New Zealand rose with no clear catalyst — likely a defensive bid into a yield-paying telco as NZ rate-cut expectations support income names.

Pattern: Looks like low-volatility momentum recovery off recent lows; isolated NZX move in a defensive telco, not part of a broader regional theme.

↓ MEL -0.85%

Mid-cap · 5.84 (local)

Why: Meridian Energy slipped modestly with no fresh headline — likely routine profit-taking in a utility after recent strength, with no NZ power-market catalyst on the tape.

Pattern: Small mean-reversion drift in a defensive utility; isolated single-name pullback rather than a broader NZX or regional utilities selloff.

Reading the Session

The exchange-by-exchange breakdown above surfaces both market-specific catalysts and cross-border themes. When multiple exchanges move together, look for a macro driver (USD move, commodity price, risk-on/off shift). Isolated single-exchange moves tend to reflect local earnings, regulatory news, or sector rotation.

Read next: Asia Pacific Markets · What Is a P/E Ratio? · What Is a Dividend?

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!