- A Shenzhen 'gold investment' app collected an estimated $1.4 billion from 22,000 retail investors — and never actually purchased any physical gold.

- Behind the marketing was an unlicensed leveraged options book in which JWR was the opposite-side counterparty to every customer bet, with leverage reaching up to 40 times.

- When gold prices surged in January 2026, customer positions moved into profit. JWR could not pay. The Shuibei market redemption queue formed the next morning.

The china gold scandal of 2026 — the collapse of a Shenzhen platform called JWR that left roughly 22,000 retail investors locked out of CNY 10 billion (about $1.4 billion) in funds — was visible on the street before it was visible in any regulator’s announcement. On the morning of January 27, families queued outside the company’s Shuibei offices in Luohu District demanding to withdraw money they had been told was held in gold. Police arrived to keep order. Two days later, the Luohu District government released what it called a “Situation Report” naming a special task force. The number circulating in the petition lists, compiled by investors and reported via Yicai, was 10 billion yuan. The platform’s WeChat customer service had gone dark a week earlier.

This is the story of how an app that called itself “gold investment” turned out to be running an unlicensed leveraged options book against its own customers — and what the rally in gold prices made visible when it pushed those customers into profit.

What JWR Was Selling

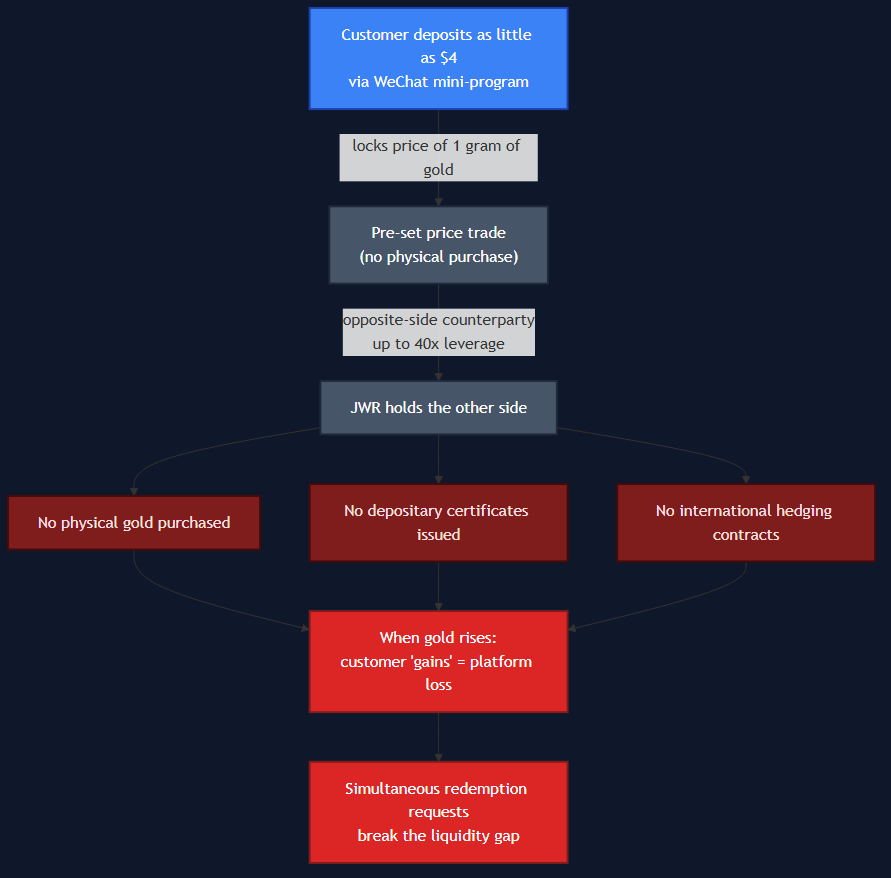

The company on the door was Shenzhen Jie Wo Rui Jewelry Co., Ltd., registered in the Shuibei Industrial Zone of Luohu District — the southern Chinese city’s traditional gold-jewellery quarter. JWR (the platform brand, written sometimes as Jieworui in English-language Chinese coverage) operated as an app-based gold-investment service that customers reached through a WeChat mini-program. The marketing was straightforward: zero-fee gold exchanges, attractive buyback prices, and a product called “pre-set price trading” that let users lock in the price of one gram of gold with a deposit as small as four US dollars.

That product is the spine of the story. It looked, to most customers, like gold-buying. It functioned, on the platform’s books, as something else entirely.

JWR did not hold a precious-metals broker licence. In China, those licences carry minimum-capital requirements, audited custody disclosures, and trading-venue reporting — the friction that exists for the same reason it exists in every other major jurisdiction: to make sure an entity selling claims on metal can actually deliver metal. JWR bypassed all of it by structuring itself as an “online intermediary for gold deposits,” a category that in 2025 sat outside the formal licensing perimeter for gold trading.

The numbers South China Morning Post reported, derived from mainland investor estimates compiled by Yicai, are imprecise on purpose. There may have been roughly 22,000 retail investors with active pending redemptions when the platform froze. Total platform users, by BeInCrypto’s later count, ran north of 150,000. The unpaid-funds figure circulated as 10 billion yuan (~$1.4 billion) in official-adjacent communication; The Standard in Hong Kong reported 13.4 billion yuan; authorities later called the 13.4-billion figure “significantly exaggerated” without offering an audited alternative. The exact gap is still being reconciled.

How the China Gold Scandal Mechanic Worked

Pre-set price trading was, mechanically, leveraged options trading. The customer paid a deposit to lock the price of an amount of gold. The contract settled, days or weeks later, on the difference between the locked price and the current spot price. Positions could be closed at will, on demand, without any physical gold ever moving — because no physical gold ever entered the chain.

That is the part that matters. SCMP’s follow-up reporting on the second platform crisis, citing the same mainland sources that the Tiger Brokers digest later picked up, is unambiguous: JWR did not purchase physical gold, did not issue depositary certificates, and did not hold international hedging contracts. The platform was the opposite-side counterparty to every customer bet, and the leverage in those bets reached up to forty times.

What does that mean in plain English? When a customer paid four dollars to lock the price of one gram of gold, they were not buying gold and they were not buying a futures contract from a regulated exchange. They were entering a leveraged bilateral wager against JWR. If gold went up, JWR owed them the difference. If gold went down, JWR pocketed the deposit. There was no clearinghouse, no margin account at a third-party prime broker, no settled custody on either side. The platform’s only obligation was a row in its own database.

A regulated bullion dealer makes money on the spread between buy and sell prices on metal it actually holds. A regulated futures broker collects commissions while taking no directional position. JWR was running neither of those businesses. It was running an unlicensed bookmaker — and like any bookmaker that takes one side of every bet, its solvency depended on the bets going the right way more often than they went the wrong way.

While the float of customer positions mostly cancelled out, the arrangement worked. Customers came in, locked prices, closed positions at small profits or small losses, and the float of unredeemed deposits financed the operation. The marketing — shareable referral codes, WeChat groups, jewellery-quarter foot traffic — pulled in the next cohort. The exposure lived on JWR’s side of the book, hedged by nothing except the assumption that gold would not move sharply in one direction.

The Gold Price That Broke It

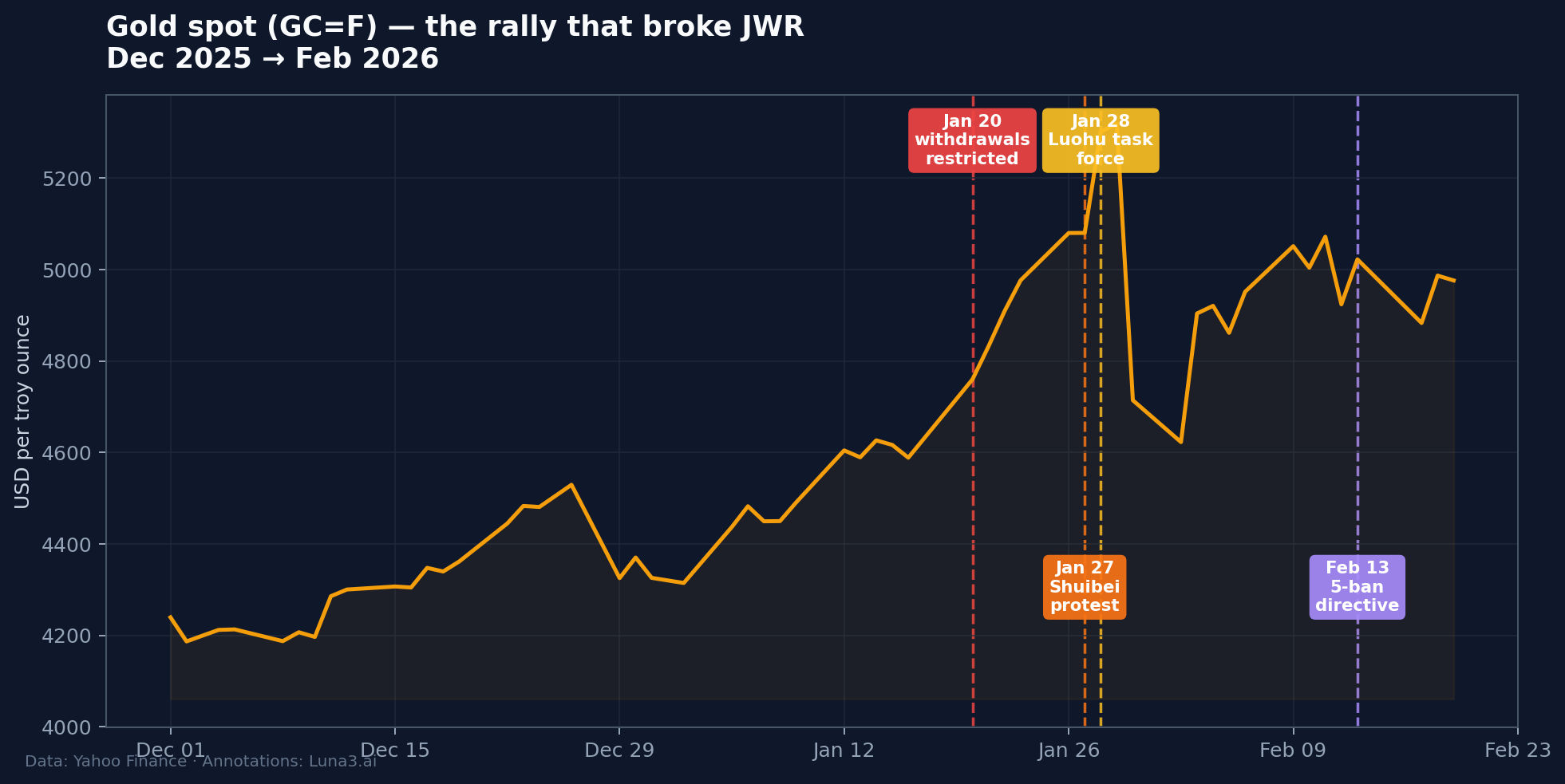

Gold went up. Not gradually — sharply.

The rally that began in late 2025 — driven by central bank reserve diversification, Middle East risk repricing, and a wave of Chinese retail buying — accelerated through early January 2026. Reports from Money Metals and other commodity trackers documented Shanghai Gold Exchange premiums widening over COMEX in the same window, an institutional tell that mainland physical demand had become a one-way flow. (Real institutional gold positioning, by contrast, is visible in weekly disclosures like the CFTC Commitments of Traders report — public, audited, and routed through a clearinghouse, none of which described JWR’s book.)

On JWR’s side of the trade, that meant something specific. The customer positions opened during the previous range — all those $4 locks on a gram of gold — moved into profit, sometimes deep into profit, because forty-times leverage on a single-digit-percent gold move compounds quickly. Customers began closing positions and requesting their winnings. The platform owed them an amount that grew with every tick of the gold price. And the float, the unredeemed deposits that had been financing day-to-day operations, started flowing out faster than new deposits flowed in.

There is no hedging contract in the chain. There is no physical gold in the vault — because there is no vault. There is only the same balance sheet that has been running an unhedged short position against forty-times-leveraged customer bets, and that balance sheet does not have ten billion yuan to settle the claims.

How the China Gold Scandal Unfolded

The collapse moved faster than the reporting around it. Here is what the public timeline looks like, reconstructed from mainland coverage carried in Yicai Global, Caixin Global, and SCMP’s follow-up cycle:

- January 20 — withdrawals first restricted. Daily caps of roughly $69 in cash or one gram of gold per user. Within days, full suspension of both cash withdrawals and physical-delivery requests.

- January 27 — investor protest escalates at the Shuibei jewellery market. Families queue outside JWR’s offices; police arrive for crowd control. The story breaks into mainland financial press.

- January 28 — Luohu District government releases a “Situation Report” announcing a special task force. The JWR WeChat mini-program updates its “clearance process” to require submitting an inventory list, confirming a repayment amount, signing agreements, and uploading payment details.

- January 31 — local authorities announce that repayment processing has begun. The first installments under the platform’s newly published compensation terms start to clear.

- February 13 — Shenzhen Municipal Financial Regulatory Bureau, jointly with ten government departments, issues a five-ban directive on gold trading (detailed below). A second platform — Ydd007 — discloses three severe runs in the same window.

The number publicly circulating in the second week — 10 billion yuan, approximately $1.4 billion at the prevailing exchange rate — came from investor petition lists compiled and verified against platform redemption queues. The Standard in Hong Kong cited a figure of 13.4 billion yuan, which authorities subsequently called “significantly exaggerated.” Neither side has produced an audited reconciliation. The 22,000-investor headcount tracks active pending redemptions in the Luohu task force’s communication; the broader user base — including dormant accounts and small positions — appears to be much higher, with BeInCrypto reporting over 150,000 users on the platform at the time of suspension.

Who Paid, Who Walked, What Changed

The compensation terms JWR offered, once the WeChat mini-program updated its “clearance process,” ran on two tracks. A customer could take a lump-sum payment at 20 percent of principal, or accept 40 percent paid out across twelve monthly installments. Both options required the customer to sign an agreement that, per BeInCrypto’s reporting, included a “criminal pardon letter” waiving the right to pursue further legal recourse. In practice, the payouts often fell short of even the 20-percent floor. One investor on a $5,100 deposit received an initial payment of $1,219 (roughly 24 percent) followed by a second application that returned just $244. Another, holding over $44,400 in position value, recovered about $2,800 — close to six percent.

On the regulatory side, the response moved with more force than the platform-clearance side. On February 13, the Shenzhen Municipal Financial Regulatory Bureau — with nine other government departments co-signing — issued a comprehensive directive aimed at the platform structure that had produced JWR and was now being replicated by Ydd007 and others. The directive is the first time mainland regulators codified, in writing, what a non-licensed gold-trading platform is not allowed to do:

- Ban on irregular pre-pricing and leveraged or deferred transactions where customers lock a future price with a deposit and settle on the difference.

- Ban on misleading marketing — slogans like “gold will surge” or “get rich by buying gold” are explicitly prohibited.

- Ban on price-fixing schemes conducted via WeChat groups, mini-programs, apps, or websites where customers deposit funds to lock prices and settle on price differences rather than via physical delivery.

- Ban on illegal fundraising via gold custody, leasing, or repurchase arrangements that promise fixed returns or guaranteed principal.

- Ban on unauthorised gold-entrusted investment activities in which firms persuade customers to buy physical gold but redirect those funds into investment schemes instead of delivering the metal.

Read together, those five bans describe JWR’s business model in detail. The platform structure that operated, marketed, and grew over the years leading up to January 2026 is, after February 13, formally proscribed within Shenzhen’s jurisdiction. What remains unclear in the weeks since is whether the directive will be enforced consistently across other mainland jurisdictions where comparable platforms operate — and whether the customers JWR took money from will see anything beyond the six-to-twenty-four-percent recoveries already on the record.

The Claims-Without-Custody Archetype

JWR is not a one-off. The platform that mainland media has been most prominently tracking since the Luohu task force formed — Ydd007, operating from the same Shenzhen ecosystem — disclosed three severe runs in late January and early February, per SCMP’s follow-up reporting. Both platforms shared the same architecture: app-based gold-investment marketing, deposit-to-lock-price product, no independent custody, and a regulator that was a beat behind. (For the way the same Shenzhen apparatus reads through disclosure at a more typical listed company, the contrast is sharp: a licensed issuer files audited statements with the exchange; a non-licensed app-based platform files nothing.) The February 13 directive was, in effect, an admission that the platform category had outgrown the licensing perimeter.

What ties this to a broader archetype — and why this story matters past the specifics of Shenzhen — is the structural gap, not the geography. Platforms that sell claims on assets they do not custody, audited by no third party, with marketing that emphasises a return profile rather than a custody profile, recur in every major retail-investing market on a long-enough timeline. The names change. The mechanism does not.

The structural tells are consistent. App-as-broker without independent custody attestation. Deposit-to-lock-price marketing rather than deposit-to-purchase. A “investment” that resembles, on the platform’s books, a leveraged book against the customer base. Customer service that runs through a messaging app rather than a regulated complaints channel. Marketing language that emphasises guaranteed returns, fixed yields, or “the platform always wins for you.” When one of those tells is present, an investor should slow down. When two or more are present together, the platform should be presumed to be carrying counterparty risk that the marketing does not disclose.

This is the same structural risk that surfaces in the 2026 private credit redemption gates that hit Blue Owl, Apollo, and Ares earlier this year, even though the asset class and customer profile look nothing alike. In both stories, the platform marketing emphasised steady returns; the platform structure carried risk that was visible only at the redemption window; and the cascade arrived faster than the regulatory framework was prepared to respond to. The asset changes — gold, private credit loans, crypto, tokenised real estate — but the pattern is the same: claims that compound while the custody attestation does not.

Five Questions Before You Send Money To A ‘Gold App’

Generic risk framing applies — this is observation, not personalised advice — and applies regardless of whether the app in question is selling gold, silver, “tokenised” anything, or the next variant of the same structure. Before sending money to any platform that markets exposure to a physical asset, an investor with the time to do the work can ask five questions:

- Who custodies the asset? An independent third-party vault, a licensed depository, or the platform itself? If the answer is “the platform itself,” or if the platform cannot answer, that is the JWR structure.

- Who audits the custodian? A big-four accounting firm, a government-recognised auditor, or a reference that resolves to a real audit report? A platform that cannot produce an audited custody attestation is not selling what it appears to be selling.

- What licence does the platform hold? Local commodities-exchange membership, securities broker-dealer registration, precious-metals-dealer licence, or none? The JWR collapse was, structurally, what “none” looks like.

- What regulator backstops it? In China: the CSRC, the PBoC, SAFE, or membership in the Shanghai Gold Exchange. In the US: the CFTC, the NFA, the SEC, FINRA. In the UK: the FCA. In Australia: ASIC. “Local market regulator” without a named agency is a non-answer.

- What physical-delivery terms actually apply? Minimum holding period before physical delivery? Storage fees? Lead times? Documented delivery process with a third-party logistics partner? If physical delivery is “available on request” with no operational detail, the platform is most likely selling claims, not gold.

None of those questions catch every fraud. Some platforms that pass all five turn out to have other problems. But the platforms that fail any one of them are almost always selling something other than what their marketing describes. JWR failed all five.

The story Luna3 will keep watching is what happens next in the Shenzhen ecosystem. The February 13 directive defines a perimeter that did not exist on January 20. Whether that perimeter is enforced, whether comparable platforms in other mainland jurisdictions adapt or wait it out, and whether the 22,000 retail investors get anything beyond the pennies-on-the-dollar recoveries already documented — those are the open questions that will determine whether the directive becomes a real constraint or a paper one.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!