- The SEC approved 30 fund companies in December 2025 — including BlackRock, JPMorgan, State Street, PIMCO, and Morgan Stanley — to add an ETF share class alongside existing mutual funds, with a further wave approved in April 2026.

- The $3.6 billion Sequoia Fund becomes the bellwether case: shareholders vote July 27, 2026, with the ETF launch targeted for mid-September 2026.

- Taxable mutual fund holders face a quiet timing question — if other shareholders bail before the ETF sibling launches, the remaining holders may carry the capital-gains hot potato.

In March, the board of the Sequoia Fund — the $3.6 billion active mutual fund run by Ruane Cunniff for more than fifty-five years — voted to convert itself into an ETF. Shareholders meet on July 27 to ratify it. If they approve, the legacy mutual fund disappears in mid-September and reopens as a New York Stock Exchange ticker. That is a fund older than most of the readers of this site changing wrappers, and it is the headline case in this year’s ETF share class wave.

Sequoia is just the loudest one. In a December 22, 2025 combined notice, the SEC quietly approved another thirty fund families to do something almost as significant: add an ETF share class alongside their existing mutual fund — same underlying portfolio, two wrappers. The plumbing has shifted. And if you hold an active mutual fund in a taxable account, the timing matters more than most coverage suggests.

What an ETF share class actually does

The mechanism is simpler than the regulatory drama. A dual share class fund holds one underlying portfolio — one set of bonds or stocks, one investment team, one prospectus. Investors then choose how they want to access that portfolio. Mutual fund holders get the legacy wrapper: shares priced once a day at the closing net asset value, bought and redeemed directly with the fund company. ETF holders get the modern wrapper: shares that trade intraday on an exchange, with creation and redemption handled in-kind by authorized participants — the big market makers like Jane Street, Susquehanna, and Goldman’s ETF desk.

Both share classes own the same securities. The difference is what happens at the wrapper level.

Mutual funds settle redemptions in cash. When you sell your mutual fund, the manager has to find cash — sometimes by selling appreciated securities, which triggers realised capital gains that the fund must distribute to the remaining shareholders. ETFs settle redemptions in-kind. When an authorized participant redeems creation units, the fund hands over a basket of underlying securities instead of cash. No sale, no realised gain, no distribution.

That single mechanism — in-kind redemption — is the entire reason ETFs are more tax-efficient than mutual funds. It is not a different investment strategy. It is a different plumbing layer. We unpacked this directly in our earlier piece on why the tax number favours ETFs over mutual funds, and the share-class wave is what makes that gap addressable from inside one fund family.

Vanguard had this structure protected by US Patent 6,879,964 from its 2005 grant through its May 2023 expiry; for those years no other fund family could legally bolt an ETF wrapper onto a mutual fund’s holdings. That is why every other major asset manager spent two decades running mutual funds and ETFs as separate vehicles — duplicating compliance, marketing, distribution, and trading desks. Now they do not have to.

The 30-firm roster

The December 22, 2025 SEC notice was a combined order — thirty applicants approved in a single document. The list reads like the entire active management industry: BlackRock, JPMorgan, State Street, Morgan Stanley, PIMCO, Schwab, Nuveen, Lord Abbett, John Hancock, Harbor, Thornburg, Victory, Hartford Mutual Funds, Impax Asset Management, Thrivent Mutual Funds, Natixis Investment Managers — among others. Dimensional Fund Advisors got its own order earlier, in October 2025, becoming the first non-Vanguard firm with this capability and the first to offer it on actively managed strategies.

An April 2026 wave added Goldman Sachs, Franklin Templeton, T. Rowe Price, and Columbia Funds. By industry estimates, roughly eighty fund families have applied; the SEC is now working through them in batches. Fidelity has applied and is being approved across the 2025-2026 waves — the largest mutual fund family in the country is in the pipeline.

Sequoia Fund is a slightly different case. Sequoia is not adding an ETF share class; it is converting its entire mutual fund into an ETF outright, then dissolving the legacy structure. The Sterling Capital Short Duration Bond Fund and Sterling Capital Ultra Short Bond Fund did the same on March 30, 2026 — straight conversions, no dual share class.

Both mechanisms reach the same destination from different routes. Conversion is cleaner for smaller funds with a homogeneous shareholder base; dual share class is the right move for fund companies that still need to serve 401(k) plans, which generally require the legacy mutual fund wrapper for record-keeping.

Why the ETF share class wave matters now

Three forces converge to make 2026 the inflection year for the ETF share class.

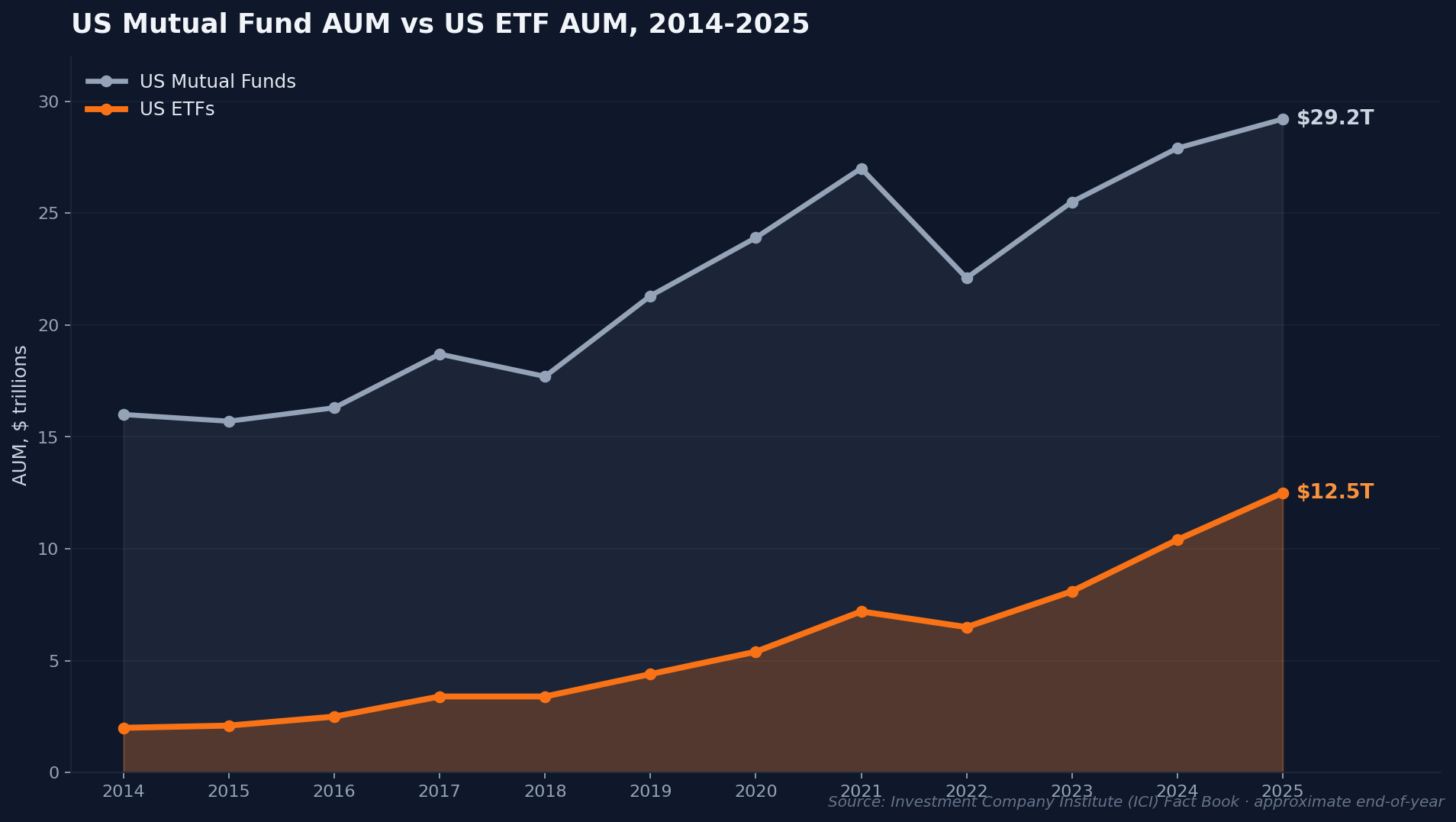

First, the tax efficiency arbitrage that has quietly bled mutual funds for years now has nowhere left to hide. The Investment Company Institute’s flow data tells the story: US long-term mutual funds have run multi-year net outflows — including $1.2 trillion in 2025 alone — while ETFs have absorbed net inflows almost every year since 2008. Most of that money is not leaving the asset class — it is just moving to a more tax-efficient wrapper. Until December 2025, making that switch meant leaving your fund manager entirely. Now the same fund firm can offer you the ETF wrapper without forcing you to change strategies or relationships.

Second, Vanguard’s structural moat is gone. From 2001, when Vanguard first launched its ETF share class under what would become Patent 6,879,964, until that patent’s expiry on May 16, 2023, no other firm could legally pair a mutual fund and an ETF on a single portfolio. Vanguard built trillions of dollars in combined ETF and mutual fund assets behind that moat. Every other manager spent the same period watching their tax-efficient wrapper compete with one hand tied. The wall came down in May 2023; the SEC exemptive relief that comes on top of patent expiry is what unblocks the regulatory side, and that arrived in late 2025.

Third, the 401(k) and mutual fund stickiness problem finally has a solution. Most retirement plans still default to mutual funds for record-keeping reasons — plan administrators are built around the legacy daily-NAV settlement cycle. A fund family that wanted to chase ETF flows had to either fork their product line (Vanguard-style) or abandon the 401(k) channel. Dual share class lets one portfolio serve both audiences. The retirement plan gets the mutual fund; the taxable brokerage account gets the ETF. Same manager, same holdings, two wrappers.

The tax math: why taxable mutual fund holders should pay attention

Here is the mechanism that should make you pay attention if you own an active mutual fund in a taxable brokerage account.

Mutual funds distribute realised capital gains annually, usually in October, November, or December. Critically, those distributions are taxable in the year they are paid — and they are paid to whoever owns the fund on the record date, regardless of when you bought in or whether you sold anything yourself. If the fund manager sold appreciated holdings during the year to fund other shareholders’ redemptions, that realised gain gets passed through to you. (For the underlying concept, see our primer on capital gains tax.)

This is benign in years when fund flows are balanced. It becomes a problem when other shareholders bail in size.

Imagine you own a $50,000 position in an active mutual fund that has been running for fifteen years and has roughly 20% embedded unrealised gains in its underlying holdings. The fund’s other shareholders include a large pool of taxable investors who decide, in late 2026, to swap into the new ETF share class — but the swap is not tax-free in every case, so some of them choose to sell instead. The fund manager has to sell appreciated securities to fund those redemptions. Realised gains pour into the fund. The fund must distribute them to the remaining holders by year-end. You — who did not sell anything — receive a 1099-DIV in January reporting a large long-term capital gain. You owe federal tax (and state, depending on where you live) on a distribution you did not choose.

The risk is not theoretical. It is the same dynamic that hit Fidelity Magellan holders in 1996, when the fund paid out a roughly 16%-of-NAV capital gains distribution after a portfolio manager change forced large realised gains onto remaining shareholders.

The pre-conversion timing question is real, but the answer is not obvious. Some funds will be able to manage the transition in-kind — distributing securities directly to the new ETF share class without triggering realised gains. Some will not, depending on the fund’s shareholder mix (IRAs and 401(k) accounts get the mutual fund regardless), the portfolio’s liquidity profile, and how aggressively other taxable holders move first.

Things worth weighing if you hold an active mutual fund in a taxable account: the fund’s embedded unrealised gain percentage (visible in semi-annual reports), your cost basis relative to NAV, your marginal tax bracket, whether the fund family has announced an ETF share class filing, and whether the fund has signalled in-kind conversion. None of this is investment advice — it is the input list for a conversation with a tax professional.

The Vanguard patent backstory

The patent that protected the structure was US 6,879,964, titled “Investment company that issues a class of conventional shares and a class of exchange-traded shares in the same fund.” Vanguard filed it on March 7, 2001 — the same year it launched its first ETF share class (Vanguard Total Stock Market ETF, ticker VTI, on a portfolio that also offered an Admiral mutual fund share class). The patent was granted April 12, 2005 and expired on May 16, 2023.

The inventors named on the patent are George U. Sauter — then Vanguard’s chief investment officer and one of the architects of low-cost indexing — and Walter Lenhard. By Bloomberg’s estimate, the structure delivered roughly one hundred billion dollars in additional gains to Vanguard clients over its protected lifetime, mostly through avoided capital gains distributions. The SEC needed to grant exemptive relief on top of the patent expiry; that started arriving in late 2025 and accelerated through the December 22, 2025 combined notice and the April 2026 wave.

Watchlist and bottom line

Three signals worth tracking through the rest of 2026:

Sequoia Fund (September 2026 ETF launch) is the bellwether. Shareholders vote on the conversion July 27. The tax outcome here — whether Sequoia executes the conversion in-kind without triggering capital gains for legacy holders — will set the template for the next dozen conversions. Watch the Ruane Cunniff investor letters.

Hartford Mutual Funds, Thrivent, Sterling Capital are the broader rollout cohort. Hartford and Thrivent are adding ETF share classes; Sterling has already gone the straight-conversion route on two of its bond funds. Q3 2026 capital-gains-distribution warnings (typically posted to fund company websites in late October and November) will tell us whether the transitions are tax-efficient or whether distributing shareholders are getting hit.

The ICI quarterly flow data is the macro signal. Net flows from existing mutual fund share classes into newly-launched ETF share classes (visible in the ICI mutual fund and ETF flow reports) will tell us whether investors are actually switching when given the option, or whether 401(k) inertia keeps the legacy wrapper sticky. The first batch of dual share classes from the December 2025 cohort should launch over the summer and fall — we will have flow data by Q4.

The plumbing change is not dramatic, but it shifts who absorbs the tax friction in the system. If you hold an active mutual fund in a taxable account, the half-hour it takes to read your fund’s most recent semi-annual report, look up its embedded unrealised gain percentage, and check whether the firm has filed for an ETF share class is worth the time. Distribution season this October and November is going to be the most interesting one in a decade.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!