- Everspin is the only public pure-play MRAM maker and the sole U.S. volume producer of this non-volatile, SRAM-speed memory.

- A $40M U.S. Navy subcontract and a 10-year onshore Microchip foundry deal turned it into a domestic-defense supply story — and tripled the stock in under two weeks.

- The catch: GAAP profit sits near breakeven, the stock trades around 11x sales versus a roughly $18 analyst consensus, and a short-seller calls MRAM a 20-year-old niche, not an AI play.

Few small-cap names have re-rated as violently in 2026 as Everspin MRAM stock. The shares closed at $13.19 on April 29, ran past $40 by May 11, and printed an all-time high of $51.50 on May 13 — a triple in under two weeks — before sliding back to the mid-$20s. The trigger was not an AI-memory breakthrough or a blowout quarter. It was a defense contract.

That gap between the catalyst and the price reaction is the whole story here. Everspin Technologies makes a kind of memory most investors have never heard of, and a single $40 million subcontract reframed it from a sleepy industrial-chip supplier into something closer to a strategic national asset. The market repriced that overnight. The question is whether the business is repricing with it.

Everspin MRAM stock last changed hands at $27.11 going into publication on June 20, 2026 — roughly +350% over the trailing twelve months, yet still about a third below its May peak. That round-trip is the tell: this is now a momentum-and-narrative name where the price can decouple from the fundamentals in both directions.

The thesis

Everspin is pivoting from a niche, roughly $55 million-revenue MRAM supplier into the only domestic, ITAR-capable volume producer of magnetoresistive memory. Two deals signed weeks apart — a $40 million, 30-month U.S. Navy subcontract and a 10-year onshore Microchip foundry agreement — are what re-rated the thesis. The bet is that defense-grade, supply-secure memory demand converts the company’s record design-win backlog into durable revenue. The counter-bet, which a short-seller has put in writing, is that MRAM remains a small, slow-growing substitution market and the stock simply ran too far, too fast.

What Everspin and MRAM actually are

Everspin is the only publicly traded pure-play MRAM company and the sole U.S. volume producer of discrete magnetoresistive memory. It has shipped more than 115 million units to over 2,000 customers, holds 650-plus MRAM patents, and runs its own fab in Chandler, Arizona. That installed base — not raw performance — is the moat.

MRAM itself sits in an unusual spot in the memory hierarchy. It is non-volatile like flash — it keeps data with no power, no refresh, and no battery — but fast and effectively unlimited-endurance like SRAM. That combination makes it ideal for persistence-critical and harsh-environment roles: industrial controllers, aerospace and defense systems, FPGA configuration, and data-center write-cache. It is not a general replacement for DRAM. Per bit it is far more expensive than mainstream memory, and it is too write-power-hungry to ever displace the high-density DRAM and NAND that sit at the center of the memory market. MRAM wins a premium niche, not a volume one — a point that matters a lot for the bear case below.

The business has two engines. Product sales are the large majority — Toggle MRAM and STT-MRAM parts under the PERSYST brand. The smaller, higher-margin engine is licensing and royalty, anchored by Everspin’s relationship with GlobalFoundries, which offers Everspin’s STT-MRAM as embedded memory on its 22FDX platform and manufactures the company’s 300mm wafers. GlobalFoundries therefore reads through to this story on both sides — as a manufacturing partner and as a licensee.

The catalyst: a $40M Navy bet and an onshore fab

The headline catalyst is the Navy subcontract, and the structure matters. This is a $40 million indefinite-delivery/indefinite-quantity (IDIQ) subcontract in which Everspin is the subcontractor to prime contractor Amentum Services, supporting the U.S. Navy’s NSWC Crane microelectronics research-and-development program. It runs 30 months, from April 20, 2026 through November 21, 2028, and covers Toggle MRAM process technology plus engineering services to stand up domestic production for strategic government systems. Management framed it as a 50%-plus gross-margin profile and — critically — left it out of second-quarter guidance, so it lands as incremental upside as revenue is recognized rather than something already in the run-rate.

The second deal is quieter but arguably more structural: a 10-year onshore foundry agreement, signed April 8, 2026, to build a 200mm MRAM line at Microchip’s Fab 4 in Gresham, Oregon. First shipments are slated for the second half of 2027, ramping toward 1,300 wafers per quarter, with roughly $13.95 million in tooling reimbursement. It does two things at once — it relieves the prior single-fab capacity ceiling and adds ITAR-capable domestic second-source capacity. That is the supply backbone a defense-memory thesis actually requires.

Underneath the two marquee deals, the operating story has been quietly accelerating. Everspin logged 238 design wins in 2025, up from 178 the year before, with most expected to ramp into production across 2026 and 2027. Its high-reliability xSPI STT-MRAM roadmap is filling out — 128Mb production qualification around May and 256Mb around July, with volume availability targeted for the second half of 2026. On the data-center side, IBM’s FlashCore Module uses Everspin’s PERSYST 1Gb DDR4 STT-MRAM, with next-generation modules and hyperscaler reference designs in development. Every one of these threads advances the same narrative: Everspin as the supply-secure, domestic, harsh-environment memory supplier.

The financials, minus the narrative

Strip out the story and the numbers cool the room. In the first quarter of 2026, Everspin reported $14.9 million in revenue, up 14% year over year. The growth engine — MRAM product sales — rose 28% to $14.1 million. But the high-margin licensing line collapsed to $0.8 million from $2.1 million a year earlier, which is why headline growth lagged product growth. Gross margin held at a healthy 52.7%. On the bottom line, the company posted a small GAAP net loss of $0.3 million ($0.01 per share) but $2.6 million of non-GAAP net income ($0.11 per diluted share). It ended the quarter with $40.5 million in cash and no debt.

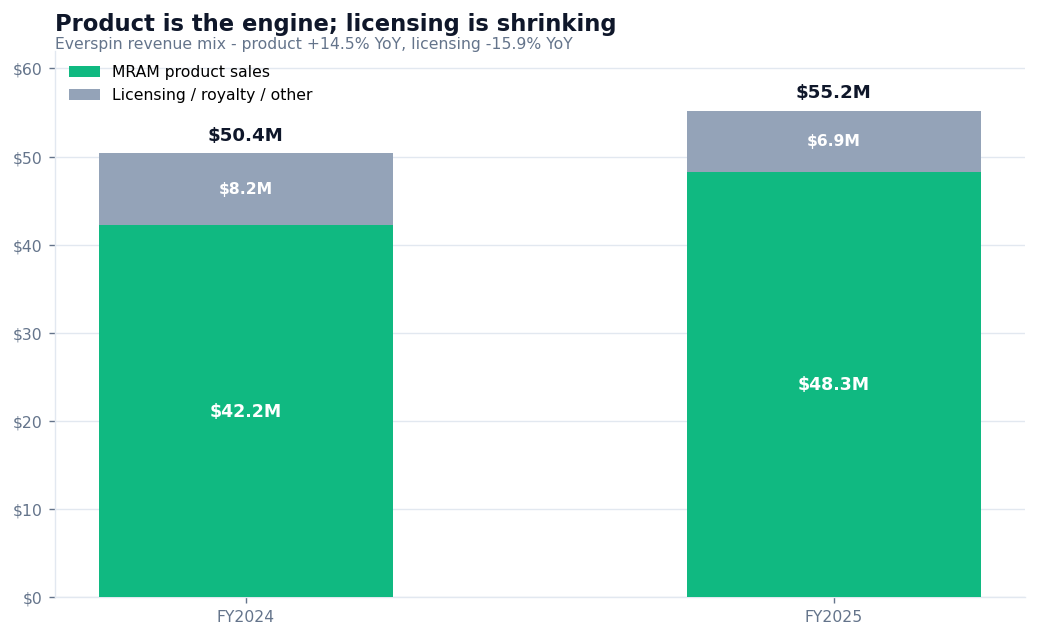

The full-year 2025 picture rhymes: $55.2 million in revenue (up 9.5%), with product up 14.5% to $48.3 million and licensing down 15.9% to $6.9 million. That mix shift tipped the company to a small GAAP net loss of $0.6 million for the year, versus a small profit in 2024. The structural read is simple — product is the durable, growing engine, and the lumpy licensing line is shrinking and dragging reported profitability with it.

Here is the snapshot, with everything reconciled to the most recent filings and live market data:

| Metric | Value | As of |

|---|---|---|

| Q1 2026 revenue | $14.9M (+14% YoY) | Q ended Mar 31, 2026 |

| Q1 2026 MRAM product sales | $14.1M (+28% YoY) | Q1 2026 |

| Q1 2026 gross margin (GAAP) | 52.7% | Q1 2026 |

| Q1 2026 net result | GAAP −$0.3M / non-GAAP +$2.6M | Q1 2026 |

| Cash & equivalents | $40.5M, zero debt | Mar 31, 2026 |

| FY2025 revenue | $55.2M (+9.5%) | FY ended Dec 31, 2025 |

| 2025 design wins | 238 (vs 178 in 2024) | FY2025 |

| Market cap | ~$636M | Jun 18, 2026 |

| Price / sales | ~11x (fwd P/E ~65x) | Jun 2026 |

| 52-week range | $5.76 – $51.50 | trailing 12 mo. |

| Analyst consensus target | ~$18 (Needham Buy, $18.50) | Apr–Jun 2026 |

The clean version: this is a small, near-breakeven, debt-free company growing its core product double digits. The deals are real and the balance sheet is sound. It is not yet a profit story. Full results and filings are on the Everspin investor relations site and in the company’s 8-K filings on SEC EDGAR.

The moat — and where it stops

What is genuinely defensible: Everspin is the only public pure-play, the sole U.S. volume producer, sits on a 115 million-unit installed base, runs its own Chandler fab, and is now adding a second domestic source in Oregon. The moat is supply position and manufacturing know-how, not a memory-performance edge. Where MRAM actually wins is the persistence-critical, last-line-of-defense roles where DRAM and SRAM are volatile and flash or EEPROM are too slow or wear out — the IBM FlashCore design-in, configuration memory validated across Lattice Semiconductor’s FPGA line, radiation-hardened parts for defense and space, and industrial and rail safety systems.

Where it stops: the same niche economics cap the upside. Avalanche Technology is the most direct standalone rival — and, as covered below, the litigant — pitching its own space-grade STT-MRAM as smaller and cheaper than Toggle MRAM for aerospace. Embedded-MRAM offerings from the large foundries validate the category but compete with Everspin’s licensing arm. And none of this is the high-bandwidth memory (HBM) that drives hyperscale AI capex — a distinction the bears lean on hard.

The bear case for Everspin MRAM stock

The strongest argument against the stock starts with valuation. At roughly 11x sales, about 10.5x EV/sales, and a forward P/E near 65x on a company growing revenue in the low teens, the shares trade well above the analyst consensus of about $18 — Needham, the most constructive house, sits at a $18.50 Buy, still meaningfully below the current price. Value-screen frameworks mark it lower still. Trailing P/E is meaningless on near-zero earnings.

The bear case got a named author on May 19, 2026, when short-seller Kerrisdale Capital published a report assigning a $14 fair value. Its argument: MRAM is a roughly two-decade-old substitution niche serving industrial, defense, and gaming markets — not the DRAM or HBM that powers AI — and revenue has been stuck in a $50–65 million band for years. Everspin’s rebuttal is the one this piece has laid out: record product growth, a real defense contract, accelerating design wins, and a contested-but-defendable IP position. Readers can weigh both; the point is that a serious skeptic has put a number on the downside.

Beyond valuation, four structural risks deserve attention. First, single-foundry dependence: Everspin’s own 10-K states it does not source advanced wafers from anyone other than GlobalFoundries, and the Oregon line does not ship until the second half of 2027. Second, customer concentration — the top two customers made up 33% of 2025 revenue. Third, litigation: Avalanche Technology filed a Delaware suit and an ITC complaint in early 2026 alleging STT-MRAM patent infringement, with the ITC instituting a Section 337 investigation that seeks an import ban; defense costs run around $1.6 million per quarter. Fourth, and hardest to dismiss, insiders sold heavily into the spring rally — one director sold roughly $8.5 million of stock, including a sale near the post-deal peak, alongside trims from the CFO and another director. Add a thin float of about 17 million shares and short interest around 14%, and you have a name that whipsaws.

The bottom line

Everspin has done the strategic work a defense-memory thesis requires: domestic capacity, an ITAR-capable second source, a real Navy contract, and a design-win backlog that is finally accelerating. The catalyst is genuine and the balance sheet is clean. But the market priced in a great deal, very quickly — a low-teens grower at GAAP breakeven trading at a double-digit sales multiple, well above where analysts and value frameworks mark it, with insiders selling into strength and a short report on the tape.

What we are watching from here is narrow and measurable: how much of the $40 million Navy revenue actually lands in the 2026 and 2027 prints, whether the 238 design wins convert to production on schedule, and whether the Avalanche litigation resolves cleanly or hardens into a real overhang. Those three lines decide whether the re-rating was the market seeing a structural shift early — or pricing a niche supplier as something it has not yet become. For readers who track these single-name catalyst setups, the same framework runs through our other catalyst-driven case studies.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings (like MRAM) and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!