Now I have the full macro picture. Let me write the post.

The key drivers this week:

– **Strait of Hormuz reopening** after US-Iran ceasefire → oil crashed ~10% back to pre-war levels → hammered NOK, weighed on commodity bloc

– **Fed hawkish dot plot** (June 17) — held at 3.50-3.75% but median flipped to imply a hike, 9 of 18 dots above current rate → supported DXY

– **Commodity bloc sold off** — AUD/NZD hit by Fed hawkishness + commodity drops (copper -3.66%, gold -3.44%)

– **GBP resilience** — barely moved vs USD despite dollar strength

Here’s the post:

—

- Norwegian krone posted the week's biggest G10 loss as oil crashed nearly 10% on Strait of Hormuz reopening

- Dollar index gained half a percent after the Fed's hawkish dot-plot flip implied at least one rate hike in 2026

- Commodity bloc (AUD, NZD) fell over 1.4% against the greenback as copper, gold, and crude all dropped sharply

The Week in the Dollar

The dollar ground higher for the week as a hawkish Fed dot plot and collapsing oil prices crushed the commodity bloc, pushing DXY to 101.4 — up 0.506% over five sessions.

The dominant force was oil. Brent crude dropped 9.84% to $71.99 and WTI fell 9.62% to $69.23 after the Strait of Hormuz effectively reopened following the US-Iran ceasefire accord. US Energy Secretary Chris Wright confirmed flows through the strait had returned to near pre-war levels, with 20 million barrels transiting in a 24-hour window. That wiped out months of geopolitical risk premium in days.

The Fed’s June 17 decision reinforced dollar strength. While the committee held rates at 3.50-3.75% unanimously, the dot plot flipped hawkish — the 2026 median moved up to 3.8%, implying a hike. Nine of 18 officials now see at least one increase this year, and 17 of 18 flagged upside risks to inflation. That shift kept rate-cut expectations firmly off the table and gave the greenback a bid that lasted all week.

Beyond oil, commodities sold off broadly: gold dropped 3.44% to $4,079, and copper fell 3.66%. Both reinforced the pressure on resource-linked currencies.

Key Pair Breakdown

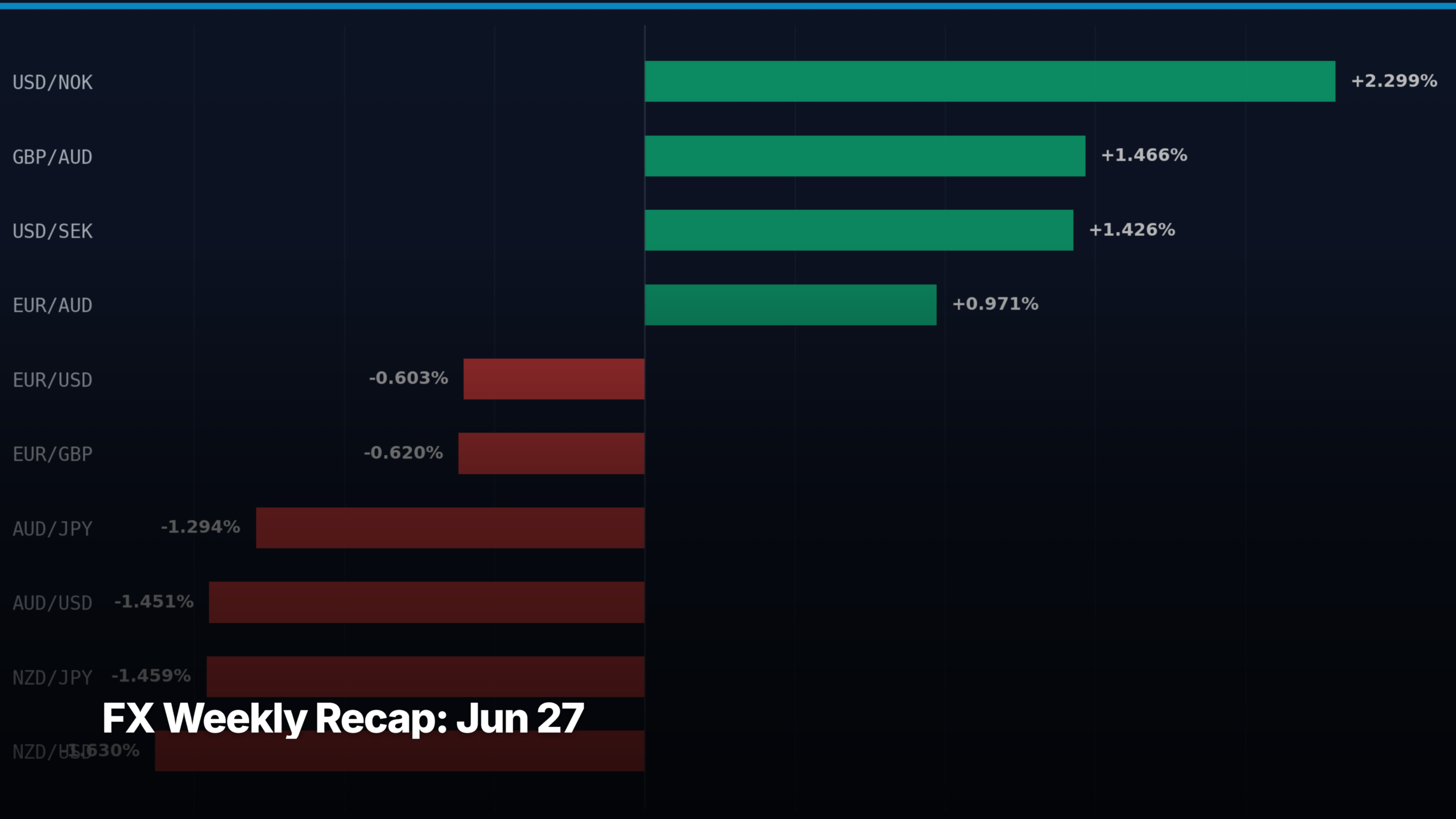

USD/NOK +2.299% to 9.9208 — The week’s biggest G10 mover and it wasn’t close. Norway’s oil-dependent krone took the full force of crude’s collapse back to pre-war levels. With Brent nearly 10% lower and the dollar bid on the hawkish dot plot, the krone had nowhere to hide. The pair is testing the 10.00 handle, a level that would mark a fresh multi-month high for the dollar against NOK.

NZD/USD −1.630% to 0.56411 — The kiwi led the antipodean selloff, weighed by three headwinds: broad dollar strength, falling commodity prices, and a hawkish Fed that widened the policy divergence with the RBNZ (on hold at 2.25% since February). NZD/USD is now below the 0.57 handle with little technical support until the 0.5550 area.

GBP/AUD +1.466% to 1.9136 — Sterling’s resilience against a weak Aussie dollar made this the second-largest G10 cross move of the week. GBP/USD was effectively flat at 1.3198 (−0.030%), while AUD/USD dropped 1.451% to 0.69013 — the divergence did the work. The pair is pressing toward 1.92, its highest level since early 2024.

NZD/JPY −1.459% to 91.205 — A pure risk-off cross. The kiwi’s weakness against the yen reflects both NZD selling and modest safe-haven flow into JPY. USD/JPY itself barely moved (+0.156% to 161.68), so the drop here was almost entirely driven by the NZD leg.

AUD/USD −1.451% to 0.69013 — The Aussie broke below 0.69, its weakest in three months. Copper’s 3.66% drop hit directly — Australia exports more copper than any G10 country. Analysts at UOB flagged AUD/USD as oversold but still vulnerable. The RBA’s hawkish hold earlier this month wasn’t enough to offset the commodity headwinds and widening rate differential with the Fed.

USD/SEK +1.426% to 9.7255 — The Swedish krona weakened alongside the Norwegian, though less severely. SEK lacks NOK’s direct oil linkage but trades as a beta to European risk sentiment. With EUR/USD down 0.603% to 1.139, the Scandis both felt the pinch of a stronger dollar and weaker European growth expectations.

AUD/JPY −1.294% to 111.58 — Same dynamic as NZD/JPY: commodity-currency weakness against a stable yen. The pair has shed ground in three of the last four weeks, reflecting the persistent drag from China slowdown fears and falling base metals.

Week Ahead Setup

This week’s oil crash and the Fed’s hawkish pivot set up two threads for the week ahead. First, whether the Strait of Hormuz ceasefire holds — Trump flagged alleged Iranian drone violations on Friday, and any re-escalation would snap oil and NOK back violently. USD/NOK near the 10.00 psychological level is the clearest binary trade on the board.

Second, the commodity bloc looks stretched. AUD/USD below 0.69 and NZD/USD below 0.565 are oversold readings by most measures, but oversold doesn’t mean finished. Watch for any bounce in copper or a shift in China stimulus expectations to trigger a squeeze.

On the calendar, US PCE data lands Friday — the Fed’s preferred inflation gauge. After the dot-plot shock, a hot print would lock in September hike expectations and extend dollar strength. A soft number could finally give the commodity currencies room to breathe. EUR/USD at 1.139 looks like it’s consolidating for a directional move; a break below 1.13 would signal a broader dollar rally is underway.

Bottom Line

The dollar owned this week on the back of a hawkish Fed and an oil market in free fall — commodity currencies paid the price while the majors (EUR, GBP, JPY) barely flinched. The pair to watch into next week is USD/NOK at the 10.00 door: if oil stabilises, the krone bounces hard; if ceasefire doubts grow, it breaks through.

Read next: FX Markets · How to Read the COT Report · What Is a Bond?

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!