- Four-day trading week (Memorial Day Monday closed); the macro and earnings calendar still punches above its weight.

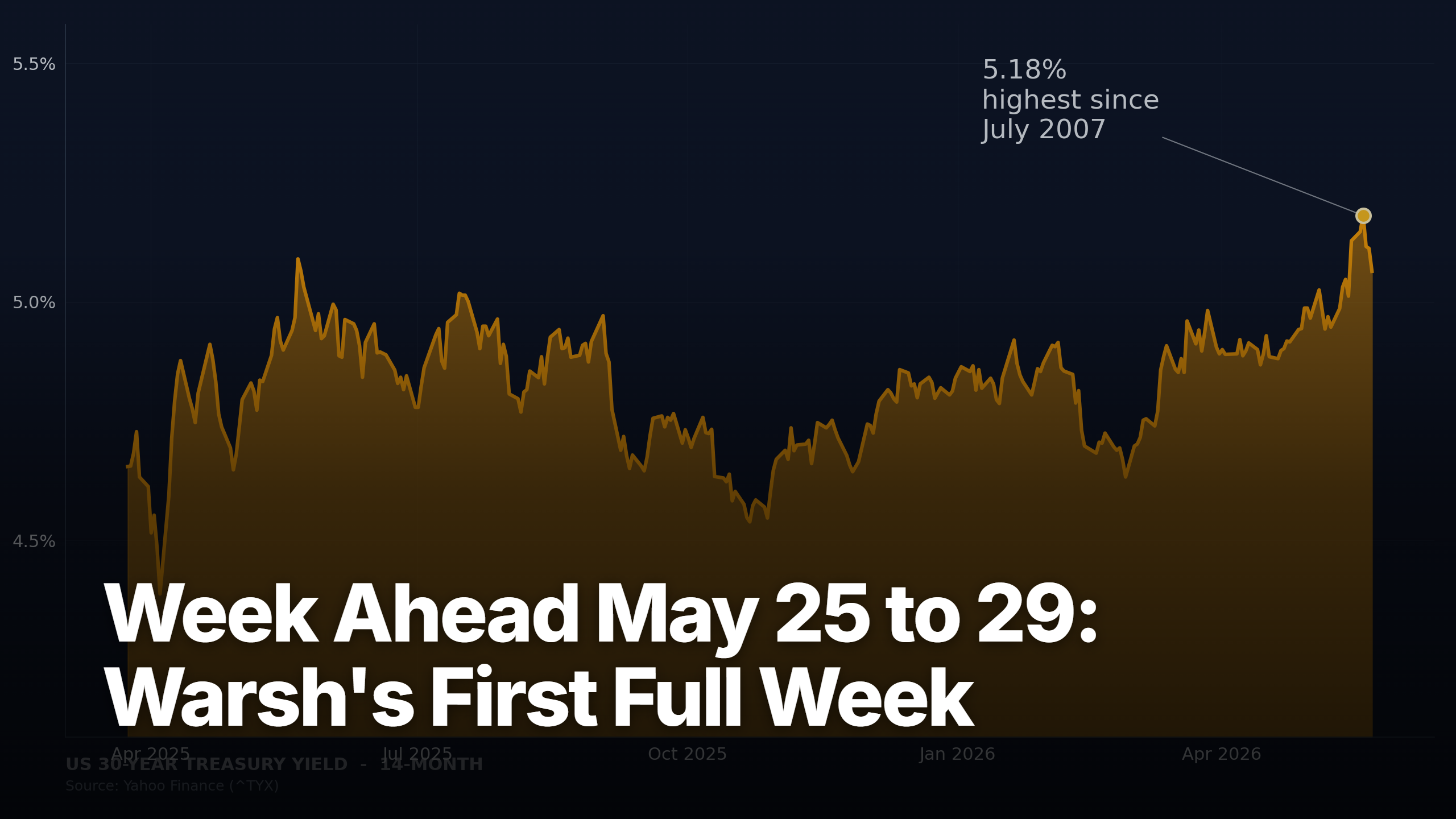

- Kevin Warsh's first full trading week as Fed Chair after Friday's White House oath; the 30-year yield brushed 5.20% last week, the highest since 2007.

- Thursday delivers an April PCE + Q1 GDP revision double-header, while MRVL, CRM, SNOW (Wed) and DELL (Thu) test whether AI capex is converting to revenue.

Welcome back to the Market Pulse Digest. Monday is closed for Memorial Day, but the four trading sessions that follow carry more weight than a normal full week — a brand-new Fed Chair sitting down behind a 30-year yield near 19-year highs, a Thursday PCE + GDP double-header landing right into his lap, and the AI infrastructure earnings cluster (MRVL, CRM, SNOW, DELL) trying to prove the capex story is real.

The setup heading in is the cleanest divergence we have seen all year: the S&P 500 closed Friday at 7,473 — within touching distance of its all-time high — while Conference Board consumer confidence sits near record lows and the long end of the curve is pricing something the equity tape does not want to acknowledge.

The market pulse digest in three threads

Thread 1 — Warsh’s first full week as Fed Chair

Kevin Warsh was sworn in last Friday (May 22) by Justice Clarence Thomas at the White House — the first Fed Chair to take the oath there since Alan Greenspan in 1987. There is no FOMC meeting this week, so the bond market will be reading any unscripted commentary closely. The tonal contrast with the Powell era is what desks are listening for: Warsh built his reputation as a hawkish voice on the FOMC during 2006-2011 and has been publicly sceptical of zero rates and large balance sheets.

One unusual wrinkle worth tracking: Powell is not leaving the Board immediately. Outgoing Chairs typically depart the institution on handover day. Powell staying as a Governor changes the dissent-vote dynamic at the next FOMC, and gives the new Chair an immediate test of whether the committee speaks with one voice.

Thread 2 — The Thursday data double-header

At 8:30 AM EDT Thursday, the BEA drops two prints in the same release window: the Q1 2026 GDP second estimate and the April Personal Income & Outlays report (which carries the April PCE deflator). Q1 GDP came in at +2.0% on the advance read — a bounce after the late-2025 government shutdown drag reversed — and the second estimate will tell us whether private demand or inventories drove the rebound. The Cleveland Fed’s inflation nowcast has April core PCE at roughly 3.28% year-over-year. An upside print on PCE, in a week where the 30-year yield closed Friday at 5.06% after brushing 5.197% on May 19, is the tape risk to watch.

Earlier in the week, Tuesday at 10 AM ET brings the Conference Board Consumer Confidence Index. Pair it with Thursday’s Costco and Dollar Tree commentary and the picture of the post-Memorial Day consumer becomes very specific, very quickly.

Thread 3 — The AI infrastructure earnings cluster

Wednesday after close delivers three tests of the AI-capex-to-revenue conversion: Marvell guides Q1 FY27 revenue at roughly $2.4 billion (analyst EPS consensus $0.75; company guide $0.79 plus or minus five cents), and the market is watching custom-silicon momentum and optical-interconnect commentary for the non-NVDA side of the data-center build. Salesforce reports consensus revenue near $11.2 billion with EPS around $2.30; the swing item is how aggressively Agentforce AI revenue is being recognised. Snowflake guides product revenue of $1.262-1.267 billion (about 27% year-over-year growth) with consensus total revenue near $1.32 billion — a direct read on enterprise AI workload spend.

Thursday before the open, Dell Technologies prints the picks-and-shovels report. Last quarter Dell disclosed a $43 billion AI server backlog and guided full-year FY27 AI revenue toward $50 billion. The market will tolerate a soft current-quarter print if the backlog and pipeline language strengthen — and it will not tolerate a soft backlog read regardless of the headline beat.

The calendar

| Day | Macro | Earnings (AC = after close · BMO = before market open) |

|---|---|---|

| Mon 25 | US MARKETS CLOSED — Memorial Day | — |

| Tue 26 | Conference Board Consumer Confidence (10am ET) | AZO, ZS |

| Wed 27 | April new home sales | DKS, MRVL AC, CRM AC, SNPS, SNOW AC |

| Thu 28 | Q1 GDP 2nd estimate · April PCE (8:30am ET) · Weekly jobless claims | DELL BMO, DLTR, MDB, BBY, COST AC, ADSK, GAP |

| Fri 29 | Quiet | — |

What the market isn’t talking about

Two things sitting under the surface that the chatter is missing.

Consumer confidence plus the COST and DLTR tape is a real-time tariff-passthrough read. If Dollar Tree commentary on Thursday surprises sour — heavier discounting, weaker low-end traffic, margin pressure language — that is the data point that has historically led broader retail revisions by one to two quarters. The SPX near ATH currently ignores it; bond market clearly does not.

Bond markets test every incoming Fed Chair in their first month. The 30-year yield closed Friday at 5.06% — pulled back from the 5.197% intraday high on May 19 but still near 19-year highs — before Warsh has spoken in his new role. Historically, a new Chair’s first six weeks are when the curve reprices its assumption of the reaction function. If the long end holds above 5% through June, the equity-vs-bonds disagreement that has defined 2026 so far moves from “ignorable” to “load-bearing.”

Charts to watch heading in

- US 30-year Treasury yield, 14-month (hero chart above). The 5.197% intraday print on May 19 is the highest since July 2007. The level the curve holds while Warsh starts speaking is the cleanest tell on bond-market confidence.

- Marvell (MRVL) 6-month price. Custom silicon plus optical interconnect = the proxy for non-NVDA AI infrastructure conviction. The post-earnings reaction Thursday morning will set the tone for the entire AI hardware ex-NVDA cohort.

- S&P 500 vs Conference Board Consumer Confidence (6-month). The widening gap between the index and the survey is the structural tension of the moment. If consumer confidence prints another low Tuesday while SPX is still 1% from ATH, the divergence becomes the headline.

One read before the bell

CBS News’ write-up of the Warsh swearing-in at the White House is worth ten minutes — not for the politics, but for the framing of how the incoming Chair characterised independence, the dual mandate, and the size of the balance sheet. Those are the three vocabulary choices that will be parsed every time he speaks for the next six months. We will be reading every word.

And as a bonus, the CNBC piece from May 19 on the 30-year yield brushing 5.197% is the cleanest summary of where the long end is positioned heading into Warsh’s first full week.

Last week’s digest is over at the May 18 week-ahead piece, and Friday’s open take sets up the long-weekend handoff into this one.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!