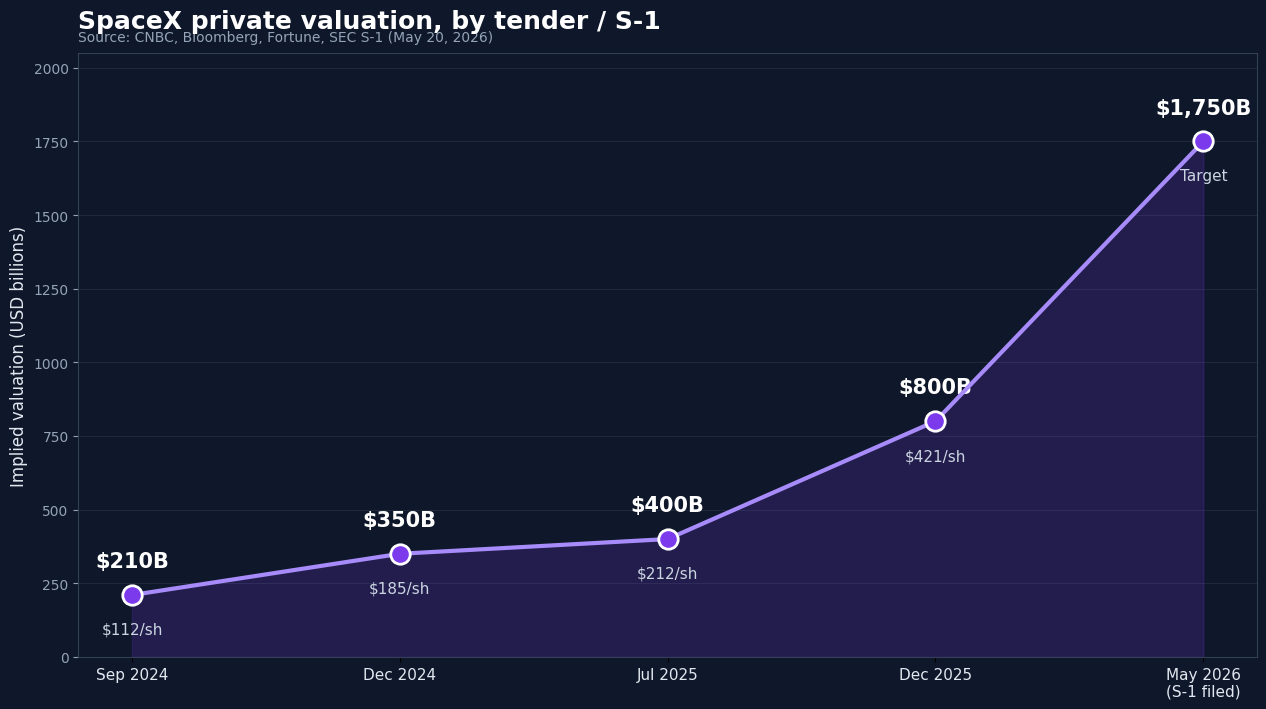

- SpaceX ran four insider tender offers between Sep 2024 and Dec 2025 — implied valuation climbed from $210B to $800B before the S-1 lifted it to $1.75T.

- The S-1 confirms Starlink as the entire profit story ($11.4B revenue, $4.4B operating income), while the consolidated xAI segment loses $6.4B per year — SPCX buyers get SpaceX + Starlink + xAI + X/Twitter in one ticker.

- S&P 500 fast-track inclusion is contingent on rule changes still under review (comments closed May 28). Under current rules, SpaceX's $4.94B 2025 net loss disqualifies it.

The SpaceX IPO will price on June 11 and list on Nasdaq as SPCX on June 12 — but the company has already been priced for 18 months in places retail investors couldn’t reach.

Between September 2024 and the S-1 filed on May 20, 2026, SpaceX ran four insider tender offers. The implied valuation moved from $210 billion to $350 billion to $400 billion to $800 billion to a $1.75 trillion target. That’s a five-fold move on the same business, in 18 months, before a single share trades publicly.

The May 20 S-1 confirmed three things the secondary market had already suggested. Starlink is the cash machine ($11.4 billion revenue, $4.4 billion operating income in 2025). The consolidated AI segment — actually xAI, merged into SpaceX in a $1.25 trillion share exchange on February 2, 2026 — is burning $6.4 billion a year against $3.2 billion in revenue. And Elon Musk wants an S&P 500 inclusion fast-track that doesn’t currently exist.

The open question on June 12 isn’t valuation. The secondary market already answered that. The question is whether the consolidated bear case — xAI burn, an IPO supply glut queued behind SpaceX, and S&P inclusion contingent on a rule change still under SEC comment — is priced at $1.75 trillion or not.

Rocket Lab (ticker RKLB) — the closest listed pure-play space company — last printed $150.23 going into publication on May 28, 2026, after running up roughly 80% year-to-date on the SpaceX IPO halo. We’ll return to RKLB and Intuitive Machines (LUNR) in the public-equity section below.

The secondary market record: 18 months of private pricing

SpaceX runs insider tender offers roughly twice a year. Employees and early investors sell stock; new investors buy in; the company itself buys back. Each tender sets a per-share price that becomes the de facto private-market mark for the next six months.

The verified record from those tenders:

- September 2024: $112 per share — the prior baseline cited in CNBC’s December 2024 coverage. Implied valuation roughly $210 billion.

- December 11, 2024: $185 per share — a $1.25 billion secondary transaction including a $500 million SpaceX buyback. Per Bloomberg and CNBC, the deal valued the company at $350 billion, up 67% in three months.

- July 2025: $212 per share — a $1 billion tender at a ~$400 billion valuation, per Fortune. Modest re-rating; Starlink subscribers still scaling, no merger yet.

- December 6–13, 2025: $421 per share — laid out in a memo from CFO Bret Johnsen, with a stock repurchase program up to $2.56 billion. Bloomberg and CNBC confirmed the $800 billion valuation. Musk publicly noted the company was targeting “about $1.5 trillion” for a 2026 IPO.

Two patterns stand out. First, each tender set a floor: open-market secondary bids on Hiive, Forge Global, and Nasdaq Private Market pushed above each prior tender within six months every time. Second, the slope steepened sharply. The December 2024 to December 2025 stretch was a 2.3× re-rating; the same period the year before was roughly flat. The S-1 effectively staples the next mark to a $1.75 trillion to $2 trillion valuation — a 2.2× lift again from December 2025. The pattern holds.

What the SpaceX IPO S-1 actually reveals

The S-1 broke SpaceX into three operating segments for the first time. Each tells a different story.

Starlink, the Connectivity segment, is the entire profit story. Revenue of $11.4 billion in 2025, operating income of $4.4 billion — a 39% operating margin on satellite broadband. That’s 61% of consolidated revenue. Connectivity revenue alone grew roughly 83% year-over-year (the full segment grew about 48% blended with hardware sales). Paid subscriptions: 8.9 million at end of 2025, 10.3 million by March 31, 2026, spread across Residential, Roam, and business plans in 155 countries. ARPU has compressed from $99 per month in 2023 to $66 per month in March 2026 as the subscriber mix shifted retail — typical for any SaaS-like product that crosses the early-adopter chasm.

The Space (launch) segment is profitable on Falcon, loss-making on Starship. Revenue $4.1 billion, operating loss of $657 million. Starship development is the entire delta — Falcon 9 is genuinely profitable; the Starship R&D burn is the cost of betting that the next-gen launch system pays off.

The AI segment is new — and “new” matters. Revenue $3.2 billion, operating loss of $6.355 billion. This segment did not exist in SpaceX’s pre-merger structure. It IS xAI, consolidated into SpaceX on February 2, 2026 in a $1.25 trillion combined-entity merger structured as a share exchange (1 xAI share = 0.1433 SpaceX shares). xAI itself had previously absorbed X Corp — formerly Twitter — in March 2025. Per Bloomberg and CNBC’s coverage of the merger close, the consolidated entity now sits at Space Exploration Technologies Corp. as the managing member of X.AI Holdings.

The structural implication is significant. SpaceX’s 2024 consolidated net income was $791 million. The 2025 figure flipped to a $4.94 billion net loss — and the swing isn’t Starlink decelerating or Falcon stumbling. It’s the retroactive consolidation of xAI’s losses. Investors buying SPCX on June 12 are buying SpaceX + Starlink + xAI + X/Twitter in one ticker, not pure-play rockets.

Capital allocation reinforces the point: $20.7 billion of total 2025 capex, of which $12.7 billion went to AI data centers, GPUs, and training infrastructure — well over half. Q1 2026 AI capex alone hit $7.7 billion. The company that won the small-satellite launch market is now also the company building one of the largest AI training clusters in the United States.

How the secondary market actually works

SpaceX has been the most-traded private stock in the United States for years, even though “trading” looked nothing like a public exchange. The pattern echoes how private capital has flowed into other trophy assets — most recently NFL franchises — over the same window.

The mechanism is what the platforms call Tape D transactions: employee sellers and early investors transferring stock to accredited buyers, brokered through marketplaces like Hiive (minimum investment around $25,000), Forge Global ($100,000 for SpaceX specifically), EquityZen ($5,000 to $200,000+ in pooled fund structures), and Nasdaq Private Market.

The accredited investor threshold the SEC uses for these transactions has been unchanged since the Dodd-Frank Act in 2010: $1 million net worth excluding primary residence, or $200,000 annual income individually ($300,000 jointly). Series 7, 65, or 82 license holders also qualify. The threshold is the framework that filters who can participate at all — it has nothing to do with whether the investment is sound and everything to do with whether the buyer is presumed capable of evaluating it independently.

The June 12 IPO compresses two things at once. The accredited-only restriction disappears: SPCX trades on Nasdaq like any other listed stock. And retail gets an outsized slice. Per CNBC’s reporting, SpaceX is reserving 30% of the $75 billion raise — roughly $22.5 billion — for retail allocations through Charles Schwab, Fidelity, Robinhood, SoFi, and E*TRADE. That’s described as “triple the historical norm” for a mega-IPO. If retail demand across all five brokerages collectively requests $100 billion against $22.5 billion available, allocations would fill at roughly 22.5 cents per requested dollar.

The gap between what accredited buyers paid at the December 2025 tender ($421 per share at $800 billion) and where the IPO prices on June 11 is the only “discount” or “premium” debate that actually matters.

The public equity angle: what moves around SPCX

Beyond SPCX itself, two listed pure-play space companies have already been re-rating on SpaceX-adjacent flow.

Rocket Lab (RKLB) competes most directly with SpaceX in small-satellite launch via the Electron rocket and is preparing the Neutron medium-lift vehicle for an H2 2026 debut. Q1 FY26 revenue: $200 million, up 64% year-over-year, against a $2.2 billion backlog including 31 new Electron and HASTE contracts plus 5 dedicated Neutron missions. RKLB is up roughly 80% year-to-date in 2026, with much of the move correlating to SpaceX IPO milestones rather than RKLB-specific catalysts.

Intuitive Machines (LUNR) sits in lunar logistics — NASA contracts plus the recently acquired Lanteris Space Systems business. Market capitalisation around $8.3 billion. 2026 revenue guidance: $900 million to $1 billion, with $943 million in backlog as of Q1. LUNR is up roughly 110% year-to-date.

Both names function as the public-market proxy for “space, but you can actually buy it pre-IPO.” A SpaceX IPO that prices well likely keeps the bid in both names; a soft IPO would likely compress the multiples that SpaceX adjacency has supported.

S&P 500 inclusion is the noisier sub-debate. Under current S&P 500 rules — 12 months listed plus GAAP profitability over a cumulative 12-month period and the most recent quarter — SpaceX does not qualify. The 2025 consolidated net loss of $4.94 billion forecloses the profitability test. But S&P Dow Jones Indices is actively reviewing the megacap eligibility rules: halving the listing period to six months and waiving the profitability requirement for companies that qualify as megacaps. The public comment period closed May 28, 2026 — yesterday. Implementation could land as early as June 8, four days before SPCX lists.

Inclusion is therefore not a base case. It’s a contingency on a rule change that may or may not pass as proposed. Anyone modeling SPCX day-one demand on automatic S&P 500 index buying is modeling the proposed rule, not the existing one. Apollo (APO), KKR, and Blackstone (BX) — the private-capital giants that have been building out infrastructure and AI compute exposure separately — are watching the same regulatory file for adjacent reasons; whatever S&P decides on megacap inclusion affects how every mega-IPO behind SPCX (OpenAI, Anthropic, Databricks) enters the index later this year.

What could break the thesis: the bear case

The bull case for SPCX at $1.75 trillion writes itself. The bear case has five pieces, all sourced from the S-1 itself.

The xAI consolidation is the load-bearing risk. Pre-merger SpaceX was profitable; consolidated SpaceX is not. xAI burned $6.4 billion against $3.2 billion of revenue in 2025, and Q1 2026 burned another $2.47 billion against $818 million of revenue. AI capex alone in Q1 was $7.7 billion. If xAI doesn’t reach revenue inflection — Grok monetisation, X advertising recovery, an enterprise API business at scale — within roughly two years, Starlink profits fund an open-ended cash drain at a structurally higher rate than pre-merger SpaceX ever ran. The S-1 narrative (“orbital data centers, vertically integrated”) sells the integration; the cash flow statement shows the cost.

Musk bandwidth. SpaceX execution has been historically remarkable, and that’s load-bearing to the bull thesis. But the management surface area now includes Tesla, xAI, X/Twitter, Neuralink, the Boring Company, and a Department of Government Efficiency role. The integration of an AI and social media operation with rockets and satellites is a fresh management problem on top of an already-full plate.

IPO supply glut. OpenAI is targeting H2 2026, Anthropic is targeting October 2026 at a reported $900 billion valuation, and Databricks is targeting Q3 2026. These deals compete for the same institutional allocation budget. SpaceX goes first, which raises a two-sided question: does SPCX absorb more than its share and leave the later deals struggling, or does the mega-IPO pipeline itself saturate demand and pressure SPCX after the first week?

The regulatory bottleneck is concrete. FAA launch licenses gate Falcon 9 cadence, and three Falcon 9 groundings inside three months in 2024 — the July 11 anomaly that lost 20 Starlink satellites, the August booster landing failure, and the September Crew-9 second-stage deorbit issue — show the precedent. Any extended grounding hits Starlink satellite replenishment directly. Starlink is the only segment carrying the profit.

Then the multiple. At $1.75 trillion on $18.7 billion of revenue, SPCX prices at roughly 94 times consolidated revenue. Allocate most of the valuation to Starlink at $11.4 billion of revenue and the segment multiple is closer to 153 times. Saudi Aramco’s 2019 record IPO priced at roughly 21 times projected earnings. Two different kinds of business, but the multiple gap is the conversation.

What to watch: timeline and signals

The next two weeks compress the entire price-discovery process that secondary markets distributed across 18 months.

- June 4: the roadshow begins. Institutional allocation signals start to leak — pre-IPO subscription levels are the most-watched private tell.

- June 8: earliest possible implementation date for the S&P Dow Jones megacap rule changes. Inclusion eligibility for SPCX hinges on this.

- June 11: IPO pricing. The number set here is the answer to the discount-versus-premium debate against the December 2025 $421 per share secondary mark.

- June 12: SPCX lists on Nasdaq. Day-one tape and the first-week drift will be the cleanest read on whether the secondary market over-priced or under-priced the IPO.

- First 30 days: RKLB and LUNR price action versus their own fundamentals will signal whether SPCX is pulling the rest of the space cohort with it or absorbing a fixed pool of sector flow.

- Q2 2026 earnings (post-listing): the first quarterly report as a public company. The Starlink subscriber number is the single most-watched metric on the line.

The cleanest framing of this whole event isn’t whether SpaceX is “worth” $1.75 trillion. It’s whether the secondary market — which has been correct on the direction of every six-month re-rating since 2020 — was correct on the magnitude this time. We’ll know the answer 14 days from now.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!