- Vanguard's 50-year study shows lump-sum investing beats dollar-cost averaging in roughly two-thirds of all rolling 12-month windows, with an average lead of 2.4 percentage points.

- The 33% of windows where DCA wins matter more than they look — they cluster around 1929, 1973, 2000, and 2007. DCA isn't optimising returns; it's insurance against your own panic-sell.

- The smart hybrid: lump-sum tax-advantaged accounts (Roth IRA, HSA, 401(k)) where a 10% withdrawal penalty acts as a behavioural fence; DCA the taxable balance over 6–12 months.

A $50,000 bonus lands. An inherited account opens up. Your RSU tranche vests. The lump sum vs DCA decision lands in your lap, and the internet’s advice splits between “Vanguard says lump sum, just deploy it” and “be careful — the market’s at all-time highs.” Both camps cite real data. Both are right about something narrow and wrong about something bigger.

This piece walks the math: what Vanguard’s 50-year backtest actually shows, why the 33% of windows where DCA wins matters more than the 67% where it loses, and the hybrid most financial planners use but no one publishes.

The Bottom Line

If you only read sixty seconds of this post, here’s the decision framework.

Lump sum if: you can hold through a 20% drop in month one without selling; the money is going into a tax-advantaged account (Roth IRA, 401(k), HSA) where the 10% early-withdrawal penalty acts as a behavioural fence; your time horizon is ten years or more.

DCA over 12 months if: you’d realistically panic-sell at –15% and lock in the loss; the windfall is more than half your current invested net worth, which adds psychological weight to every tick; you’re investing in a taxable account and need the optionality to abort.

Hybrid — the underrated answer most planners actually use: lump-sum the tax-advantaged portion (Roth IRA, HSA, any unused 401(k) room), then DCA the taxable balance over six to twelve months.

That’s the decision. The rest of this post shows why.

Lump Sum vs DCA: What 50 Years of Data Actually Says

The most-cited number in this debate comes from Vanguard’s 2012 study, Dollar-Cost Averaging Just Means Taking Risk Later. The researchers backtested rolling 12-month windows across US, UK, and Australian markets from 1926 to 2011. Lump-sum investing produced higher ending wealth in 67% of all rolling windows, with an average outperformance of 2.4 percentage points over the 12-month DCA period for all-equity portfolios.

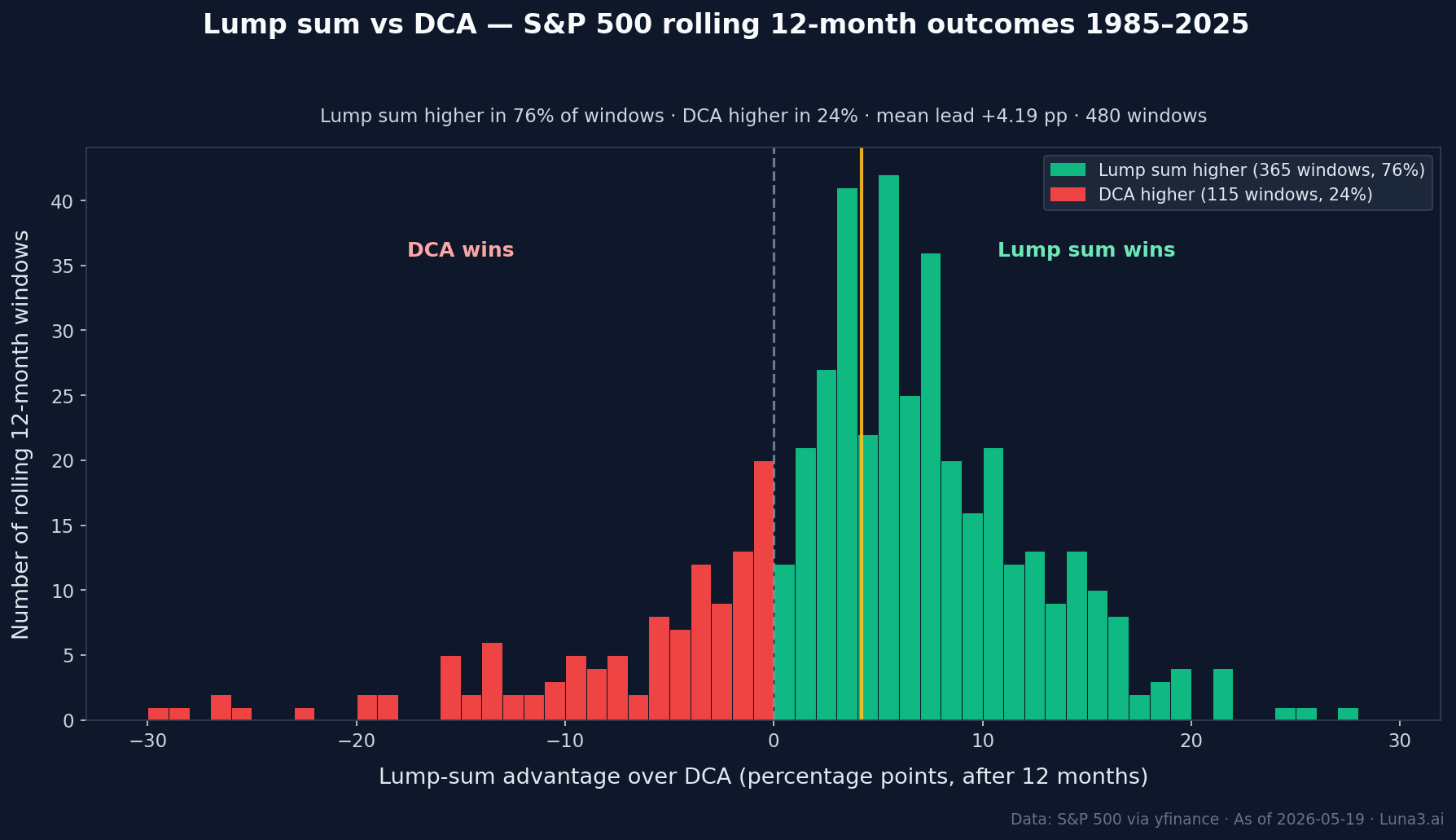

Vanguard re-ran the analysis in February 2023 on MSCI World data from 1976 to 2022. Virtually identical result: lump sum won 68% of the time at the one-year mark. Our own replication of the test on the S&P 500 from 1985 to 2025 ran even hotter — lump sum won 76% of 480 rolling 12-month windows, with a 4.2 percentage-point average lead — because the past forty years skewed bullish relative to the longer Vanguard sample.

Three things people miss about the headline figure.

The 67% measures outcomes at the end of the 12-month investing period, not in the long run. Twenty years out, the lump-sum lead is much wider — because the lump sum had a full extra year of compounding while the DCA was still sitting in cash.

The 2.4 percentage-point gap is the average. The median is closer to 1.8. The distribution is right-skewed: most outcomes cluster near zero, but lump sum’s wins in roaring bull years are very large.

The 33% of windows where DCA wins are not random. They concentrate around 1929, 1973, 2000, and 2007 — the lead-ins to major drawdowns. DCA didn’t win on average; it won by avoiding cliffs.

The honest reframe: lump sum beats DCA on average because the market goes up in roughly two-thirds of any given year. DCA is essentially buying a free option on a bear market — and most years, that option expires worthless.

The Dollar Math: $100,000, Three Outcomes

Forget percentages for a second. Here’s what the math looks like on a real number — $100,000 — across three market paths.

Setup: $100,000 windfall deployed into VOO (Vanguard S&P 500 ETF) at $545 per share. The lump sum buys 183 shares on day zero. The DCA plan buys $8,333 per month for twelve months.

Path A — bull year (+20%): the lump sum’s 183 shares are worth 183 × $654 = $120,000. The DCA, with an average buy-in price around $575, ends up with roughly 174 shares worth $113,800. DCA underperformed lump sum by $5,900.

Path B — sideways year (0%): both strategies finish near $100,000. Roughly a wash.

Path C — bear year (–20%): the lump sum’s 183 shares are worth 183 × $436 = $80,000. The DCA, with an average buy-in price around $510, accumulates ~196 shares worth $85,500. DCA outperformed lump sum by $5,700.

Weighting by Vanguard’s historical frequencies (lump-sum wins ~67% of the time, DCA ~33%), the expected one-year outperformance of lump sum on a $100,000 windfall is roughly +$2,300. Compound that out twenty years at a 7% real return and the gap reaches about $8,900 in 2026 dollars. Real, but not life-changing.

That’s the actual price of DCA’s optionality. The question is whether that price is worth it for your specific risk tolerance — not whether the strategy is “correct.”

Why DCA Wins Anyway for Most People

The math says lump sum. The data on actual retail behaviour says DCA — because the math leaves out sequence-of-returns regret.

If you lump-sum $100,000 on Friday and the market drops 18% the following Monday, you have lost $18,000. You will not feel a 20-year compounded outcome. You will feel the $18,000 loss every single day for six months.

Dalbar’s 2025 QAIB report — the 30th annual edition of the canonical retail-investor-behaviour study — found the average equity-fund investor earned 16.54% in 2024 against the S&P 500’s 25.02%. That’s an 8.48 percentage-point behaviour gap, the second-largest in a decade. The gap is overwhelmingly driven by selling during drawdowns and missing the rebound — exactly the failure mode that the lump-sum math invites.

DCA isn’t an optimisation strategy. It’s insurance against your own future self. The 2.4-percentage-point annual cost is the premium.

The right framework for the decision isn’t “which has the higher expected return.” The math already answered that. The real question is: if I lump-sum and the market drops 20% in month one, will I still be holding in five years? If yes — lump sum. Take the expected-value win. If the honest answer is “I’d probably sell” — DCA. The 2.4-point giveaway buys you the discipline you don’t otherwise have.

This is why the hybrid works. Tax-advantaged accounts (Roth IRA, 401(k), HSA) have a 10% early-withdrawal penalty under age 59½. That penalty is a behavioural fence — most retail investors who would panic-sell a taxable account won’t pay a 10% tax to do it inside a Roth. Taxable money has no fence. The optimal split mirrors the psychological one.

The Smart Hybrid

This is the version most financial planners actually run for clients but never publish, because it doesn’t make a clean headline.

Step 1 — lump-sum the tax-advantaged buckets. Per the IRS’s 2026 contribution limits, a married couple where both spouses are under age 50 with family HSA coverage can deploy:

- Spouse 1 Roth IRA: $7,500

- Spouse 2 Roth IRA: $7,500

- HSA (family coverage): $8,750

- Total tax-advantaged lump sum: $23,750 — roughly 24% of a $100,000 windfall.

These dollars get deployed on day zero. The 10% early-withdrawal penalty inside the Roth and the HSA is the behavioural fence — you won’t sell.

Step 2 — DCA the taxable balance. The remaining $76,250 goes into a brokerage VOO position at $6,354 per month over twelve months. The cash earns roughly 4.0–4.2% APY in a high-yield savings account while it waits, producing about $1,700 of interest over the year — partially offsetting the DCA giveaway.

This beats both pure strategies on three dimensions. It captures most of the lump-sum upside, because the retirement-account portion gets a full year of compounding from day zero. It removes the regret risk on the taxable portion, where panic-selling actually happens. It earns roughly $1,700 in HYSA interest during the wait, recovering about a quarter of the expected DCA cost. And it removes the “deploy now or wait?” decision fatigue by answering both, in the right ratios.

This is the version most planners build into the financial models that robo-advisors hardcode. It’s also the version retail blogs almost never write — because “Vanguard says lump sum” is a cleaner clickbait line.

Common Mistakes

DCA over 24 months or longer. The lump-sum advantage scales with the DCA period. Twelve months is the sweet spot. Stretch beyond eighteen months and you’ve forfeited so much expected return that the optionality isn’t worth it. Vanguard’s own analysis shows lump sum winning roughly 92% of the time when DCA stretches to 36 months.

Holding the windfall in cash because “the market is at all-time highs.” JPMorgan’s Guide to the Markets notes the S&P 500 has set a new all-time high on roughly 7% of all trading days since 1950 — ATHs are a feature of any uptrending market, not a warning sign. JPMorgan’s measurement from 1970 forward: investing at an ATH has produced a 9.6% average twelve-month forward return, essentially identical to the 9.4% averaged across all other days. The “wait for the pullback” instinct doesn’t show up in the data.

DCA-ing into individual stocks instead of an index. DCA averages your cost basis on a diversified basket. On a single name with binary outcomes — bankruptcy, buyout, fraud — DCA can mean averaging down into a falling knife. If you’re deploying into anything other than a broad index, the strategy doesn’t work the same way.

Forgetting to harvest tax losses during the DCA window. If you DCA into taxable and the market drops mid-deployment, the higher-cost-basis lots can be sold and rebought to realise losses you can deduct against gains. Most retail investors miss this — and it can claw back 50 to 100 basis points of the DCA giveaway.

Confusing “DCA” with regular contributions from salary. They’re not the same. Salary DCA is forced — you can’t lump-sum money you haven’t earned. The Vanguard math only applies to windfalls, where the lump-sum option actually exists.

Treating Nick Maggiulli’s “Even God Couldn’t Beat Dollar Cost Averaging” as a vote for DCA over lump sum. It isn’t. The piece argues that even with perfect foresight, you’d struggle to time market bottoms across a multi-decade career — which is an argument for not waiting. The most-quoted DCA-friendly post on the internet is actually a lump-sum argument in disguise.

What to Read Next

- Roth vs Traditional IRA: The Breakeven Math Nobody Shows You — once you’ve decided how to deploy a windfall, the next decision is which account type to put it in. The breakeven math is simpler than most guides admit.

- VOO vs VTI: Which Vanguard ETF Actually Makes More Sense? — practical follow-up: what to actually buy with the lump sum once it lands in the brokerage.

- ETF Expense Ratios: The Small Number Quietly Destroying Your Returns — the 2.4-percentage-point DCA giveaway and a 0.30% expense ratio are the same arithmetic, just on different time scales.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!