- Both VOO and VTI carry a 0.03% expense ratio, but VTI holds ~3,520 stocks vs VOO's 504 — the extra exposure is roughly 12% mid-cap and 6% small-cap appended to the same S&P 500 core.

- Daily-return correlation between the two ETFs is 0.9956 over a decade — in virtually every market regime, they are functionally interchangeable.

- The real decision isn't 'more diversification is better' — it's whether you want an 18% mid-and-small-cap tilt baked into one ticker, or prefer a pure S&P 500 building block.

Pick any random Reddit thread on VOO vs VTI and you’ll get the same conclusion: “VTI has more diversification, so it’s the safer pick.” That’s true in the sense that 3,520 stocks is more than 504. It’s also useless as a decision rule, because both ETFs have moved in lockstep for the past decade — daily-return correlation 0.9956, total-return delta of about half a percentage point per year — and the part of VTI that isn’t S&P 500 is small enough that the entire debate hinges on inputs nobody mentions in the thread.

This piece builds the quantitative framework the Reddit answer skips: what each ETF actually holds, how similar they really are when you look at the receipts, and the four inputs that should determine your choice (none of which are “more diversification = better”). If you already know what VOO and VTI hold, skip to the framework section.

What VOO and VTI actually hold

VOO is the Vanguard S&P 500 ETF — 504 stocks (the index occasionally holds 503-505 due to multi-class shares), tracking the S&P 500 Index. 0.03% expense ratio. Quarterly dividends. About $1.5 trillion in assets, which makes it one of the most-traded equity instruments in existence.

VTI is the Vanguard Total Stock Market ETF — 3,520 stocks as of the Q1 2026 fact sheet, tracking the CRSP US Total Market Index. Same 0.03% expense ratio. Same fund family. Same tax treatment.

Here’s the reframe most “VTI is more diversified” arguments miss: VTI is not a different exposure layered on top of VOO. It’s the S&P 500 again — at roughly 82% of the weight — plus a 12% mid-cap allocation and a 6% small-cap allocation rounding out the total US listed market. So you’re not really asking “do I want more diversification?” You’re asking “do I want an 18% mid-and-small-cap tilt baked into a single ETF?”

That reframing changes everything. If the answer is yes and you don’t already own a small-cap fund, VTI is the cleaner one-ticker solution. If the answer is no, or you already own a separate small-cap holding like VB or IJR, VOO is the more honest building block — because owning VTI on top of a separate small-cap ETF means you’re double-counting the small-cap exposure and pretending you weren’t.

How similar are they, actually?

Most posts assert “they’re basically the same” without showing the math. The math is worth showing because the size of the gap determines whether the choice matters at all.

Three numbers worth memorising:

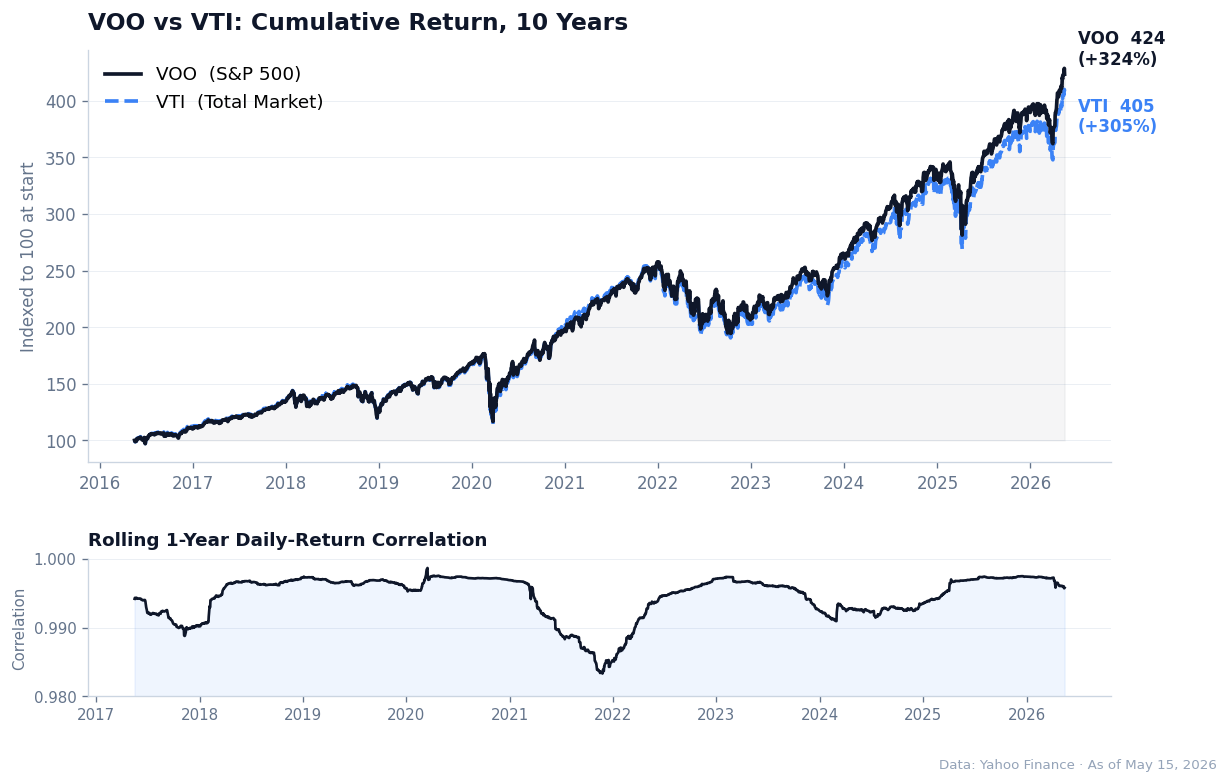

- Daily-return correlation, 10 years: 0.9956. About as close to 1.0 as two real-world securities ever get. The rolling 1-year correlation has stayed between 0.983 and 0.998 over the entire decade — even through the COVID crash, the 2022 bear market, and the 2023 mega-cap concentration spike. There’s no regime where they meaningfully decouple.

- 10-year cumulative return: VOO +324%, VTI +305%. A ~19-percentage-point gap in absolute terms, which sounds large until you annualise it. That’s 15.53% per year for VOO vs 15.01% for VTI — a delta of about 52 basis points per year.

- Holdings overlap: the top ~500 names in VTI are the S&P 500 components, weighted proportionally, then diluted by about 18% to make room for the extended market. There is no scenario where one ETF holds a stock the other doesn’t with any meaningful weight in the top quartile.

The 52bp/yr delta over the past decade has a specific explanation: mega-cap tech outperformed the broader market by an unusually wide margin. Nvidia, Apple, Microsoft, Amazon, Meta, Alphabet — all sit at roughly the same weight in both ETFs, but VOO has more of them as a share of total assets because there’s no mid- and small-cap dilution. When the mega-caps lead, VOO wins. When small-caps lead (think 2020-2021 reflation), VTI wins. Average that over a full cycle and the gap shrinks dramatically.

That decade-specific tailwind is doing more work in the “VOO outperforms” headline than the structural design of either fund. Don’t extrapolate it forward.

VOO vs VTI: the four inputs that actually decide it

A quant-style decision framework, not a vibe check. Four inputs, ordered by how much they matter in practice.

1. What else is in your portfolio?

This is the load-bearing input. The question isn’t “VOO or VTI in a vacuum.” It’s “VOO or VTI given everything else I already hold.”

- Single-ETF US equity allocation (you hold one fund as your entire US stock sleeve): VTI is the cleaner pick. The 18% mid-and-small-cap allocation is exposure you’d otherwise have to assemble manually, and the marginal expense ratio cost is zero.

- You already own a separate small-cap or extended-market ETF (VB, VBR, IJR, AVUV, IWN, anything similar): VOO is the cleaner pick. Owning VTI on top of a dedicated small-cap holding means your portfolio’s true small-cap weight is the small-cap ETF weight plus another 6% from VTI’s extended-market portion. You’re double-allocating and probably didn’t notice.

- You own VOO and a small-cap separately, and you’re considering “consolidating” into VTI: that consolidation reduces your small-cap weight unless you maintain the small-cap holding alongside VTI. Most people who make this switch end up under-allocated to small-caps because they didn’t run the math.

2. Are you tax-loss harvesting?

If you systematically tax-loss harvest (selling at a loss to bank the deduction, then immediately buying a near-substitute to stay in the market), the “harvest partner” question matters.

The conventional pair is VOO ↔ IVV: Vanguard’s S&P 500 ETF and BlackRock’s iShares S&P 500 ETF, both tracking the same index. Different fund families, different prospectuses, different boards — but the IRS has never formally ruled on whether two ETFs tracking the same index count as “substantially identical” under the wash-sale rule. Tax-community consensus splits roughly into two camps: the conservative reading treats them as substantially identical (same index, near-identical holdings, near-identical performance); the more aggressive reading treats them as distinct securities issued by unrelated entities. Both views have credible advocates; neither has been tested in court. This is general information, not personalised tax advice — if you’re actually harvesting, talk to a CPA.

The cleaner pair from a wash-sale-risk perspective is VOO ↔ VTI. Different indices (S&P 500 vs CRSP US Total Market), demonstrably different holdings (3,016 stocks that VTI holds and VOO doesn’t), demonstrably different performance over short windows — much harder for any reasonable interpretation to call them substantially identical. The trade-off: every time you cycle through the pair, you briefly take on (or shed) about 18% small-and-mid-cap tilt. For a quarterly harvest cycle on a small fraction of the position, this is usually noise. For a portfolio-wide flip on a large position, it’s a structural change.

If TLH is a meaningful part of your strategy, VOO has cleaner partner availability (VOO ↔ VTI, with the caveat above; VOO ↔ SPLG as a tighter same-index pair with the same IVV-style debate; VOO ↔ SPY as a third option). VTI’s partner set is narrower: ITOT comes closest, but it tracks the S&P Total Market Index rather than CRSP’s, so it’s actually a slightly safer “different index” play than VOO ↔ IVV.

3. Trade structure (only matters at scale)

VOO trades at tighter bid-ask spreads than VTI in average market conditions. Daily volume is higher on VOO. Premium and discount to NAV behave similarly under normal conditions but VOO holds tighter during volatile sessions because the underlying is more liquid.

At a $1,000 single-trade size, this is invisible. At a $10,000 trade in a normal session, it’s still essentially zero. It only starts to matter at $100,000+ single trades in volatile conditions — at which point you’re probably either using limit orders specifically to avoid the spread, or working with a financial advisor who handles the execution layer. For most retail readers, this input is a footnote, not a decider.

4. Do you believe in the small-cap premium?

This is the input most retail investors ignore but that academically determines whether VTI’s small-cap allocation is “free exposure” or “uncompensated active risk you didn’t choose.”

The original Fama-French research from the early 1990s identified a roughly 5% annual size premium — small-caps outperformed large-caps over the 1972-1991 window by enough to justify a structural tilt. That premium has shrunk dramatically since — to under 1% per year over the 1991-present period, with multiple decade-long stretches of small-cap underperformance. Some researchers wrote the obituary; others argue the premium survives once you control for stock quality (filter out the deeply unprofitable, balance-sheet-impaired small-caps that drag the average down). The AQR-style “Size Matters, If You Control Your Junk” interpretation has gained ground; nothing is settled.

So: if you believe in some version of a quality-adjusted small-cap premium, VTI’s 18% extended-market allocation is “free exposure” you’d otherwise have to construct deliberately. If you don’t, that same 18% is uncompensated active risk — a tilt you didn’t explicitly choose, on a thesis you don’t necessarily endorse, embedded inside an index fund you bought for passive simplicity. Neither answer is wrong; the question is whether you’ve actually thought about it.

How a quant algorithm decides this

Two questions, four answers. Use this as a backstop when you’re spiralling on the Reddit threads.

| If you… | Hold a separate small-cap ETF? YES | Hold a separate small-cap ETF? NO |

|---|---|---|

| Tax-loss harvest? YES | VOO (clean TLH workflow, no double-counting) | VOO + harvest into VTI (gives you small-cap tilt for the harvest window) |

| Tax-loss harvest? NO | VOO (avoid double-counting small-caps) | VTI (single-fund US equity sleeve; small-cap exposure included) |

Three of the four cells point to VOO. That’s not because VOO is “better” — it’s because most multi-ETF portfolios already cover the small-cap angle elsewhere, and the cleanest building block is the one that doesn’t overlap.

What doesn’t matter (despite what the Reddit posts say)

- Fund size or liquidity risk. Both are massive — VOO around $1.5T, VTI around $1.7T. Neither is going to have a liquidity problem in any realistic scenario.

- Tracking error. Vanguard runs both with essentially zero tracking error against their respective indices. Whichever index you pick, the fund will give it to you.

- Dividend yield differential. Within five basis points, will fluctuate with composition, doesn’t compound to anything meaningful over a 30-year horizon.

- “VTI has more diversification.” Only true if you don’t already have small-cap exposure elsewhere. In a portfolio context, “more diversification” is meaningless without specifying what you’re diversified from.

- “VOO outperformed last decade.” A real number, driven by a specific (and not-obviously-repeatable) mega-cap concentration regime. Don’t extrapolate.

What to do next

Starting fresh: use the matrix. Either ETF is a defensible choice; the matrix just makes the choice explicit.

Considering a switch in a taxable account: probably don’t. The expected annual edge between VOO and VTI is tiny in either direction, and capital gains tax on a position you’ve held for years almost certainly outweighs that edge for decades. Switch in tax-advantaged accounts (IRA, 401(k), Australian super, etc.) where the tax cost is zero; leave taxable positions alone.

DRIPing (dividend reinvestment): easiest migration path is to redirect future contributions and dividends to the new ETF while leaving the existing position alone. Over a few years you naturally shift the weighting without realising any gains.

The honest summary: the VOO-versus-VTI decision matters less than almost anything else about your investing — less than your savings rate, less than your asset allocation between stocks and bonds, less than your behavior during the next bear market. If you’re spending more than ten minutes on this choice, you’re probably optimising the wrong variable. Pick one, contribute consistently, and revisit the decision only if your portfolio composition genuinely changes.

For more thesis-driven research on systematic decision frameworks (rather than vibe-checks), see our breakdown of how a quantitative framework reframes the bitcoin miners → AI infrastructure pivot — same idea applied to a different asset class. The full library of Luna3 intelligence pieces follows the same quant-first lens: replace the gut call with the math.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!