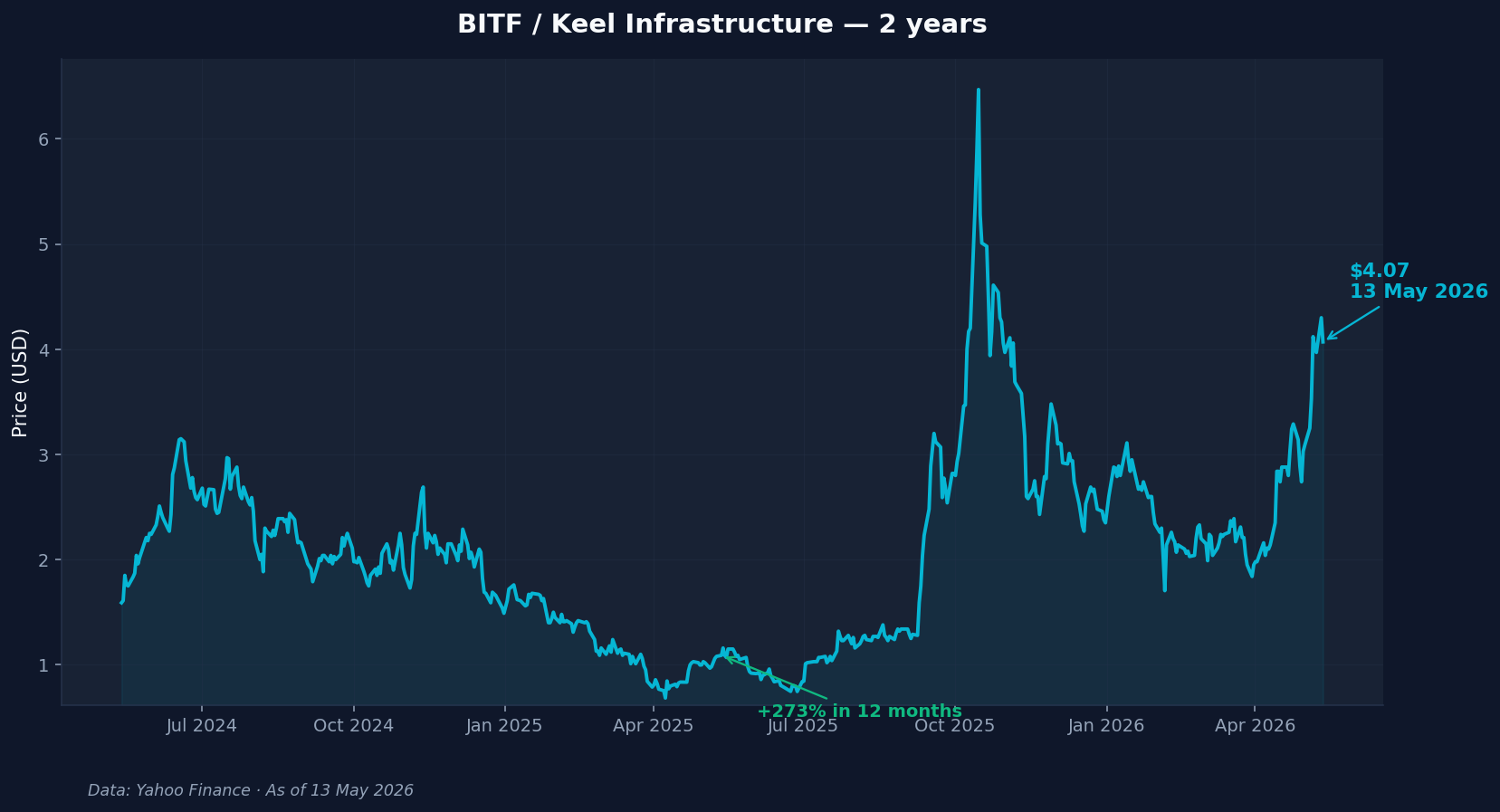

- Bitfarms sold all its Bitcoin and rebranded as Keel Infrastructure, pivoting from crypto mining to AI and high-performance computing colocation.

- Miner sites collapse hyperscale data-center build timelines from four to six years to roughly eighteen months at a fraction of greenfield capex — that arbitrage is why hyperscalers are signing long-term colocation contracts.

- The dispersion between pivoted miners (CIFR +485%, BITF/KEEL +251% TTM) and pure-play Bitcoin holders (MARA -22%) is the market separating two business models in real time.

The pivot has been six months in motion. In November 2025, Bitfarms announced a $128 million binding deal to convert an 18-megawatt Washington facility into high-performance computing colocation for AI tenants. The company sold its last Bitcoin in Q1 2026, completed the rebrand to Keel Infrastructure in April 2026, and is targeting commercial go-live at the Washington site for December 2026.

The stock — ticker BITF, now trading as KEEL — last printed $4.15 going into publication on May 14, 2026, and is up roughly 251% in the trailing twelve months. This is no longer a crypto trade. It’s a power-asset trade dressed up in a miner’s old clothes, and the broader pattern is the one Wall Street still hasn’t fully priced.

The thesis

The AI infrastructure buildout has one binding constraint, and it isn’t what most retail discourse focuses on. It isn’t GPUs. It isn’t capital. It isn’t talent. It’s electrons.

Hyperscalers can write nine-figure checks for Nvidia silicon in a single quarter. They cannot will new gigawatt-scale data centers into existence in less than three to five years. Grid interconnect queues in PJM and WECC — the two largest US transmission organizations relevant to data center siting — now show backlogs measured in years rather than months. The IEA’s Electricity 2024 report flagged data center power demand as the fastest-growing line item in OECD electricity forecasts, and the gap between projected demand and committed new generation is widening, not closing.

Bitcoin miners spent the last decade quietly hoarding the exact asset hyperscalers cannot build fast enough: cheap, permitted, grid-connected, industrial-scale power capacity. They built it for one purpose. They are now sitting on infrastructure that has become — almost by accident — the most asymmetric picks-and-shovels position in the AI cycle.

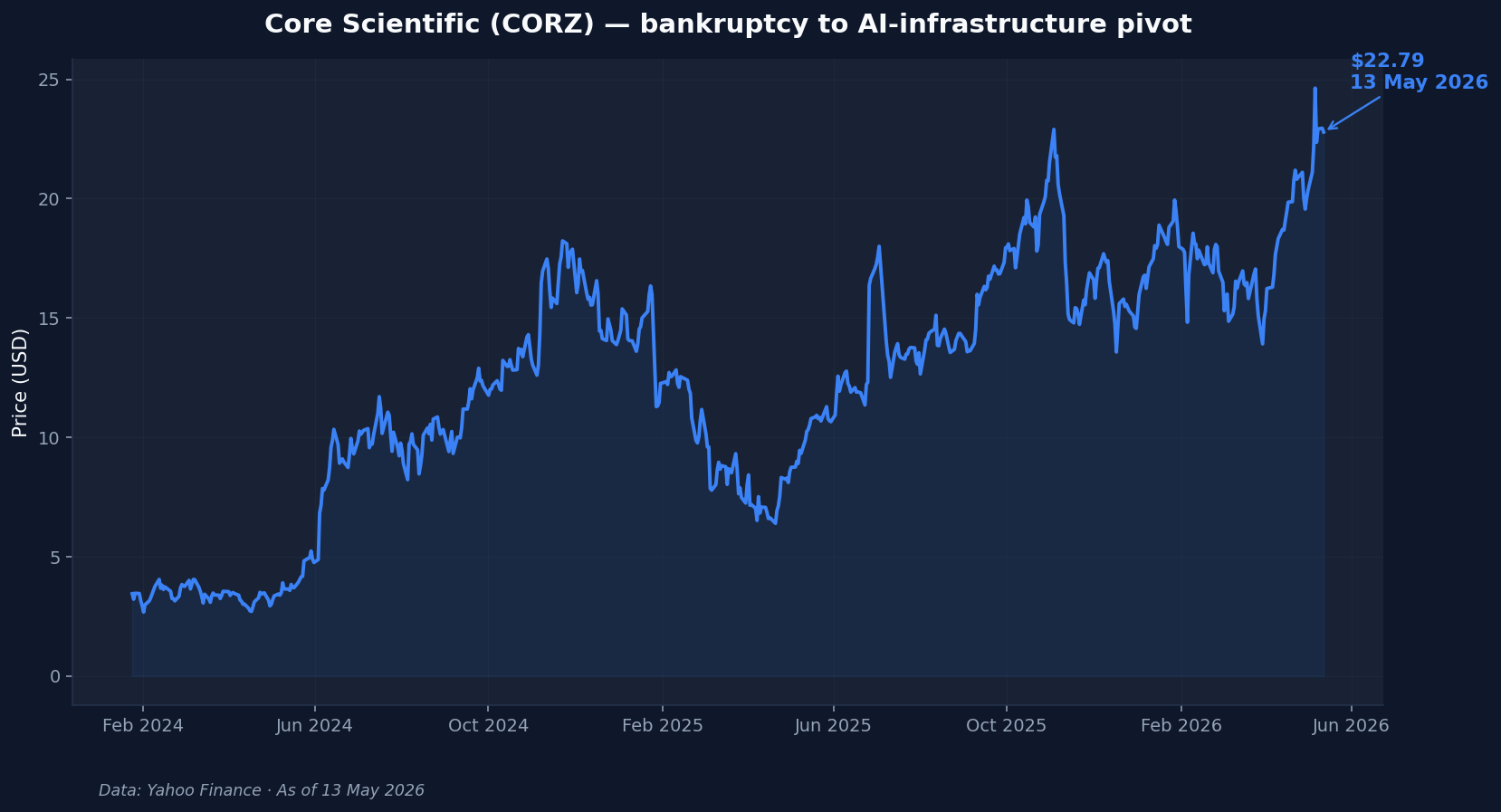

BITF is the lead case study. Core Scientific (NASDAQ: CORZ) wrote the playbook three years ago. The rest of the publicly-listed miners are now standing roughly where CORZ stood at the start of 2023 — and the market is starting to figure out which ones are about to follow the same arc.

Why bitcoin miners AI infrastructure is repricing now

The thesis sits inside a single comparison.

Marathon Digital (MARA), which has explicitly maintained a pure-play Bitcoin mining strategy, is down 22% over the trailing twelve months. Cipher Mining (CIFR), which has announced HPC tenant agreements, is up 485%. Bitfarms — mid-pivot, mid-rebrand — is up 251%. Core Scientific, already operating an HPC business at scale, is up 123%. Riot Platforms (RIOT), which has hedged its position with selective HPC announcements while continuing to mine, sits at +171%.

This dispersion isn’t random. It’s the market separating two business models in real time. If you own megawatts in the right grid zone and you’ve signed contracts with HPC tenants, you’re an infrastructure company trading at infrastructure multiples. If you haven’t pivoted, you’re a leveraged proxy on the Bitcoin halving cycle. The spread between those two valuations is now wider than at any point in the sector’s history.

The BITF → KEEL anatomy

Bitfarms’ transformation is the cleanest case in the sector because management didn’t hedge. They didn’t keep half a mining operation running while pivoting the other half. They liquidated the entire Bitcoin position, exited self-mining as a business line, and re-incorporated the company under a new identity — Keel Infrastructure — that explicitly markets itself as an HPC and AI colocation provider.

The anchor transaction is the 18MW Washington State facility conversion. The deal is a binding $128 million commitment with a named HPC tenant, targeting commercial go-live in December 2026. The economics are what matter: Bitfarms acquired the site as a mining facility years before the AI capex cycle began. The power purchase agreements, the grid interconnect, the substation infrastructure, the cooling buildout, the site permitting — all of it existed already. The $128 million is conversion capex, not greenfield buildout.

For comparison, a new-build hyperscale data center of similar capacity, starting from raw land in a comparable grid zone, would take an estimated four to six years from site selection to commercial operation, and the all-in capex would run several multiples of the conversion figure. The miner sites collapse that timeline to roughly eighteen months and a fraction of the cost. That arbitrage — time and capex versus organic buildout — is the entire reason hyperscalers are willing to sign multi-year colocation contracts with companies that were mining crypto eighteen months ago.

The market’s response has been to re-rate the equity ahead of the operational milestone. KEEL still trades at a market cap near $1.2 billion at the time of writing, which — relative to the power capacity now under HPC contract and the announced pipeline — implies a substantial discount to where pure-play data center REITs trade on the same megawatt basis. The valuation gap is the trade. Whether it closes depends on execution.

Core Scientific wrote the playbook

The reason this thesis isn’t speculative is that it’s already played out once, and the data is observable.

Core Scientific filed for Chapter 11 bankruptcy in December 2022 during the worst of the crypto winter, with hash prices collapsing while electricity costs were spiking. At the time, CORZ was treated by markets as a wipeout. The equity went to single-digit cents and stayed there. The conventional wisdom was that the company was structurally broken — too levered, too exposed to a single commodity cycle, too capital-intensive to recover.

What actually happened next is the template. Through the restructuring, the company’s most valuable assets were revealed: not the Bitcoin miners themselves, but the underlying infrastructure — the megawatts, the grid interconnects, the long-term power purchase agreements at sub-market rates. When CoreWeave, the GPU cloud provider, needed to scale capacity quickly to meet AI tenant demand, the cheapest and fastest path was to colocate inside existing Core Scientific facilities rather than build from scratch.

The resulting agreement — publicly reported as a multi-billion-dollar, twelve-year colocation commitment covering approximately 1.2 gigawatts of capacity — re-rated CORZ from a bankruptcy survivor into a critical AI infrastructure provider. The stock has climbed from sub-dollar levels to the low-twenties in roughly two years, and the multiple expansion reflects the market’s recognition that the underlying business was never really crypto. It was always power.

This is the template KEEL is explicitly following. The difference — and it matters — is that BITF chose the conversion proactively, with the balance sheet still intact, before being forced into it by another crypto downturn. The execution risk is lower because the company isn’t operating under court supervision. The market is already pricing some of the expected re-rating, which is why the BITF chart looks the way it does. The remaining gap to CORZ-style infrastructure multiples is the asymmetric piece.

The picks-and-shovels framing

The most common framing of the AI trade is the Nvidia trade — buy the chip designer. The second-order framing has been the hyperscaler trade — buy Microsoft, Amazon, Google. Both have already had their re-ratings priced in. The third-order trade, which is still partially mispriced because it sits in the wrong sector classification, is the power and colocation layer.

Hyperscalers pay a premium for four things, in this order: power, land with grid interconnect, cooling infrastructure, and operational uptime guarantees. Bitcoin miners have spent the last decade optimizing for the first three. Power costs are the single largest line item in mining economics, so every site selected over the past decade was selected for cheap, abundant, reliable power. Cooling at industrial scale is required to run ASICs at 100% duty cycle. Grid interconnects were the gating constraint on every facility build. The miners didn’t know they were building AI infrastructure. They were building it anyway.

The conversion isn’t free. HPC tenants demand higher operational standards than self-mining — true redundant cooling, higher-grade UPS systems, fiber-grade connectivity, SLA guarantees the miners never had to offer themselves. The retrofit capex is meaningful. But it’s a fraction of greenfield, and the underlying scarce asset — the permitted, energized, grid-connected megawatt — is what the contract is paying for.

The basket of names that own this asset profile sits in plain sight on any miner-sector watchlist. CIFR has already begun the re-rating. CORZ is mid-cycle. KEEL is at the start of its operational milestone curve. RIOT has hedged. MARA, the largest by name recognition, remains the laggard precisely because it hasn’t committed to the pivot — and the chart is the score.

What could invalidate this

Every thesis worth writing has a bear case. Three are credible here.

First — the AI capex cycle slows. The entire conversion thesis depends on hyperscaler demand continuing to outrun new-build supply. If Microsoft, Amazon, or Google announce material capex pullbacks in their next earnings cycles, the bid for colocation capacity disappears. The 2026 hyperscaler capex guidance has so far accelerated rather than slowed, but that can turn. A demand-side shock would expose miners mid-conversion with elevated capex and softening tenant demand — the worst possible position.

Second — power pricing risk. “Stranded power” isn’t always synonymous with “cheap.” Many of these facilities were sited on long-term power purchase agreements priced years ago. When those PPAs roll over, the new rates reflect current grid economics, which are deteriorating for industrial buyers. Some of the perceived margin advantage will compress over the next three to five years as PPAs renew at higher prices. The thesis assumes a margin profile that may not survive renewal.

Third — execution risk on the operational pivot. Running a mining facility and running HPC-grade colocation are different businesses. SLA requirements, security expectations, customer support obligations, and operational complexity are materially higher. CORZ had the benefit of CoreWeave essentially financing and operationally co-managing the transition. KEEL is doing this with a $128 million contract — significant but not transformative — and a balance sheet that’s healthier than CORZ’s was but smaller than CORZ’s is now. The conversion can succeed and still produce thinner margins than the market is currently pricing.

There’s also the competitive question. Pure-play data center REITs like Equinix and Digital Realty are themselves accelerating expansion, with cheaper cost of capital and better operational track records. They aren’t winning the speed-to-market race against miner conversions, but they may compress pricing across the sector over time. The miner re-rating works because they’re undervalued relative to their assets — not because they have a permanent moat.

What we’re watching

The sector trades with extraordinary volatility, the underlying business model is still mid-transition, and any of the bear cases above can materialize without much warning. What’s observable is the structural pattern: a category of companies whose accounting still classifies them as crypto miners is mid-way through becoming infrastructure providers, and the market is repricing them name by name as evidence of the pivot becomes contractually concrete.

The cohort splits into three observable groups: power-asset holders that have signed HPC tenants, those still leaning on crypto narratives, and a middle band where the pivot is in motion but unproven. Historically, multi-name structural transitions like this one have produced clearer separation between winners and losers on a 12-month horizon than on a 1-month horizon — making cohort-level observation more reliable than any single-name view.

Catalysts to watch

Four signals would either confirm or invalidate the thesis over the next two quarters:

- KEEL operational update — the Q3 2026 disclosure on the Washington facility conversion timeline and any expansion announcements beyond the initial 18MW

- Hyperscaler capex guidance — Microsoft, Amazon, and Google’s next earnings releases; any directional change in AI capex growth is the demand-side leading indicator

- Cipher and Riot capital allocation — the next two announcements from CIFR and RIOT will signal whether the broader miner basket follows BITF’s full-conversion model or hedges

- US grid interconnect queue data — public PJM and WECC interconnect filings; if backlog continues to grow, the scarcity premium for already-energized capacity grows with it

The miners-to-infrastructure pivot is the most under-reported structural trade in the current AI cycle. CORZ already happened. KEEL is happening now. Whoever the next two are will be obvious in retrospect — and the data to identify them is already public.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings (like KEEL) and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!