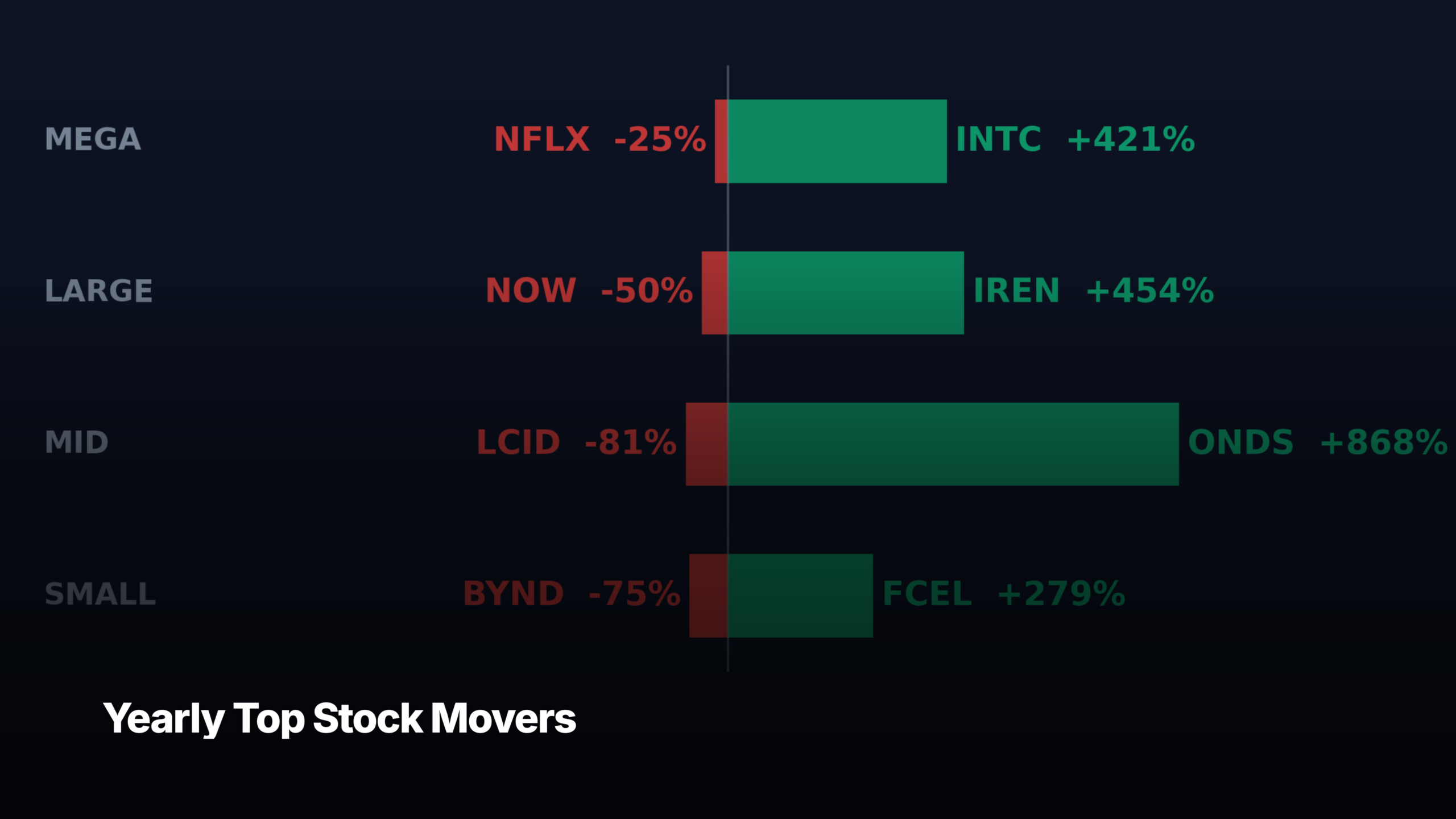

- Ondas (ONDS) printed the biggest US-listed annual gain at roughly +868%; Lucid (LCID) was the worst, down 81%.

- The S&P 500 returned +25% over the same window — every cap tier produced multiple winners that beat the index by more than 4x.

- AI infrastructure (silicon turnarounds, miners-pivoting-to-HPC, satellite direct-to-device) dominated the winners; IT services squeezed by AI, EV pure-plays, and consumer-discretionary names led the losers.

The past year’s top stock movers list separates structural re-ratings from momentum fades. The stocks at the top aren’t the same names that led weekly or monthly boards — they’re the names that compounded a thesis across twelve months of tape. Ondas (ONDS) led the entire universe with a roughly +868% gain; Lucid (LCID) printed the worst return at -81%. The dispersion between best and worst tells you what kind of market this was.

How we built this top stock movers list

We pulled adjusted-close returns for every ticker in our curated ~145-name US universe over the 251 trading days from May 20, 2025 to May 19, 2026, filtered for at least $1M average daily dollar volume, and sorted by current market cap (mega ≥$200B, large $10B–$200B, mid $2B–$10B, small $300M–$2B). For each cap tier we show the top three gainers and top three losers. The cap tier is computed at today’s market cap, not last May’s — so names that re-rated upward through the year sit in the tier that screens against them today, even if they started the window two tiers lower.

For context: the S&P 500 (SPY) returned +25.2% over the same window. The Nasdaq 100 (QQQ) printed +35.5%, the Russell 2000 small-cap benchmark (IWM) +32.0%, and the Dow (DIA) +17.5%. Small-caps and Nasdaq names outpaced large-cap value by a wide margin, and the spread between the best-performing cap tier and the worst-performing single name printed at roughly 949 percentage points (ONDS +868% vs LCID -81%). That kind of internal dispersion is what makes annual cap-tier rankings useful: it isolates where the structural bid sat and where the structural bleed was.

Mega-cap leaders ($200B+)

Winners.

- INTC +421% — Intel re-rated harder than any other mega-cap on the back of three things: Lip-Bu Tan taking over as CEO in March 2025, the US government’s $8.9B equity stake funded by CHIPS Act + Secure Enclave grants, and high-volume manufacturing on 18A starting late 2025 with Panther Lake shipping. Worth flagging: Intel was a large-cap at the start of this window (~$92B market cap, $21 share). The re-rate alone pushed it across the mega-cap threshold and back into this leaderboard.

- AMD +265% — Hyperscaler design wins on the MI-series accelerator line plus enterprise inference traction that didn’t exist a year ago. Pattern read: steady share-take against NVDA in inference workloads, with the gross-margin profile that comes from a second-source position.

- CAT +149% — Caterpillar isn’t a chip company, but it’s an AI-capex play. The order book for prime-power gas turbines and gensets supplying AI datacenters built across the year. The same story powering NEE, VST, and CEG showed up here on the equipment side.

Losers.

- NFLX -25% — Ad-tier growth slowed, password-sharing tailwind faded, and the subscriber-growth print stopped impressing. Mega-cap streaming as a re-rating story is done.

- HD -17% — Housing transaction volumes stayed depressed under high mortgage rates; project demand softened with the consumer. Notable that HD is the only mega-cap loser in our list that isn’t tech-adjacent — confirms the de-rate was a macro-rate-and-consumer story, not the AI displacement narrative weighing on NOW and ACN further down.

- IBM -15% — Cyclical drag in consulting and infrastructure software. The AI-narrative bid that lifted enterprise software broadly didn’t extend to IBM’s mix; the multiple didn’t keep pace with the index.

Large-cap leaders ($10B–$200B)

Winners.

- IREN +454% — Iren Limited (formerly Iris Energy) executed the cleanest bitcoin-miner-to-AI-infrastructure pivot of the cohort. New HPC contracts, GPU rollout, and a re-rating of the energy-asset base under an AI multiple. Tape pattern: classic structural breakout with rising volume.

- HUT +454% — Hut 8 ran the same playbook as IREN with a tighter time horizon. Started this window as a small-cap (~$1.5B); is now firmly large-cap ($10.9B) on the same miner-pivot thesis. Tier re-rate is the entire story.

- ASTS +252% — AST SpaceMobile’s direct-to-device satellite-to-cellular thesis kept compounding. Commercial deals signed with AT&T (continental US) and Verizon (October 2025), plus successful two-way broadband video calls from BlueBird satellites. CEO Avellan reiterated the 45-satellite target into year-end.

Losers.

- NOW -50% — ServiceNow’s multiple compressed sharply. The growth-stock-with-AI-tailwind framing didn’t hold once enterprise IT spend slowed and AI integration costs showed up in operating margin.

- RBLX -46% — Roblox bookings and DAU growth softened against a heavy expectation bar. The consumer-internet de-rating extended into the platform.

- ACN -44% — Accenture printed the worst large-cap loss in IT services. Federal contract cuts and the perception that generative AI permanently reduces demand for labor-intensive consulting hit the multiple. Mizuho cut its price target from $309 to $280 in March 2026.

Mid-cap leaders ($2B–$10B)

Winners.

- ONDS +868% — Ondas Holdings was the single biggest US-listed gainer in our universe. The transformation from a small-cap industrial radio business into a defense-drone platform via six 2026 acquisitions (Mistral and World View among them) lifted pro-forma backlog from ~$10M at the start of 2025 to $457M by March 31, 2026. Revenue printed +500% YoY in Q3 2025 and tenfold in Q1 2026. Started this window as a sub-$1 stock.

- OPEN +480% — Opendoor was the textbook meme-rally of the year. Stock printed a record low of $0.51 in June 2025, then ran more than 2,000% off the bottom to $10.87 by September on a Reddit/X retail bid. The September CEO change (Kaz Nejatian) and Wu/Rabois board return is the founder-driven AI-pivot leg. Whether the rally holds is a separate question from whether it ran.

- CIFR +397% — Cipher Mining ran the miner-pivot-to-HPC playbook from the mid-cap end. Same thesis as IREN and HUT, smaller asset base, larger percentage move because of the starting point. CIFR was a small-cap at the start of the window; the re-rate pushed it into mid-cap territory and onto this leaderboard.

Mid-cap is the tier where the structural shifts and the meme rallies overlapped the most. ONDS’ transformation from a sub-$1 stock into a defense-platform consolidator is a real-economy story. OPEN is a retail flow story. CIFR sits next to its larger cousins in a thematic bucket the market re-priced. The tape doesn’t distinguish — readers should.

Losers.

- LCID -81% — Lucid was the worst-performing name in our entire universe. The EV pricing war, balance-sheet draw, and ongoing dilution overhang weighed across the whole year. The Saudi PIF backstop didn’t translate into multiple support.

- MNDY -74% — monday.com saw the sharpest SaaS multiple compression in our mid-cap cohort. The story was clean: bookings decelerated, productivity-SaaS was the highest-multiple corner of software, and the de-rate found it first.

- HIMS -63% — Hims & Hers re-rated downward on the GLP-1 transition. The FDA’s February 2026 announcement of “decisive steps” against compounded GLP-1s knocked 16% off in a session; Novo Nordisk’s lawsuit (later voluntarily dismissed) and Q1 2026 earnings miss compounded it. The platform is pivoting from compounded margins to branded distribution at lower unit economics.

Small-cap leaders ($300M–$2B)

Winners.

- FCEL +279% — FuelCell Energy led the hydrogen rally. Fuel-cell names re-rated on the back of datacenter prime-power conversations and a thinly-traded float that amplified flow.

- BLDP +201% — Ballard Power printed the same hydrogen rally with similar mechanics. Both names sit in the small-cap thematic basket that retail investors discovered after the AI-power story matured.

- GLSI +155% — Greenwich LifeSciences is a binary-catalyst biotech name with a single Phase III readout (FLAMINGO-01) coming. The +155% is anticipatory positioning rather than a delivered result. Worth flagging the binary risk: a negative readout would reverse this with similar magnitude.

Losers.

- BYND -75% — Beyond Meat continued the consumer-brand collapse. The plant-based category structurally undershipped early projections, and the balance-sheet pressure tightened across 2025.

- ASAN -63% — Asana’s productivity-SaaS de-rate paralleled MNDY’s at the smaller end. Same story, lower multiple to start, similar magnitude decline.

- CHPT -56% — ChargePoint’s EV-charging build-out kept burning capital faster than utilization caught up. Sits well below the small-cap threshold now at ~$140M market cap; included here because the story is a small-cap thesis that fell through the floor.

Worth noting: four names that started this window in our small-cap bucket — MVIS, BLNK, EVGO, CHPT, and SPCE — have fallen through the $300M floor into micro-cap territory. That’s a quiet structural story. The retail-favourite small-cap clean-energy and EV cohort that ran into 2021–2022 has been continuously de-rating, and the bottom of the small-cap tier is where you see it most clearly.

What the past year’s top stock movers tells us

Three patterns read across the four tiers. AI-capex was the dominant theme on the long side, and it expressed at every cap. Mega-cap had Intel’s silicon turnaround and AMD’s inference share-take. Large-cap had IREN, HUT, and the satellite-DTD story in ASTS. Mid-cap had Cipher and Ondas’ pivot-to-defense-AI. Even Caterpillar — the most boring name on this list — is an AI-capex play through gas-turbine and prime-power supply.

The losers cluster on the other side of the same trade. ServiceNow, Accenture, and the productivity-SaaS cohort (MNDY, ASAN, RBLX) all printed material de-rates as the market priced AI as a labor-replacement risk for them, not a tailwind. EV pure-plays (LCID, CHPT) and consumer-brand collapses (BYND, HIMS, FUBO-adjacent) rounded out the bottom. The dispersion between the best and worst printed at ~950 percentage points within the mid-cap tier alone (ONDS +868% vs LCID -81%) — the widest tier-internal spread in any of our multi-timeframe boards.

Compared with our past 6-month leaderboard and our past 3-month board, the annual view shows how many of the shorter-window leaders held their gains across the full year — bitcoin miners, AI-infrastructure names, and ONDS all sit on both. The year filters out the noise the daily boards can’t.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!