- BlackRock declared the 60/40 portfolio dead in March 2026 — but it returned ~15% in 2023, 2024, and 2025 after its 2022 crash.

- The real issue isn't the 60/40 split — it's that the stock-bond correlation flipped positive in 2022 and stayed above 0.5 for three years. By September 2025 it had fallen back to 0.16.

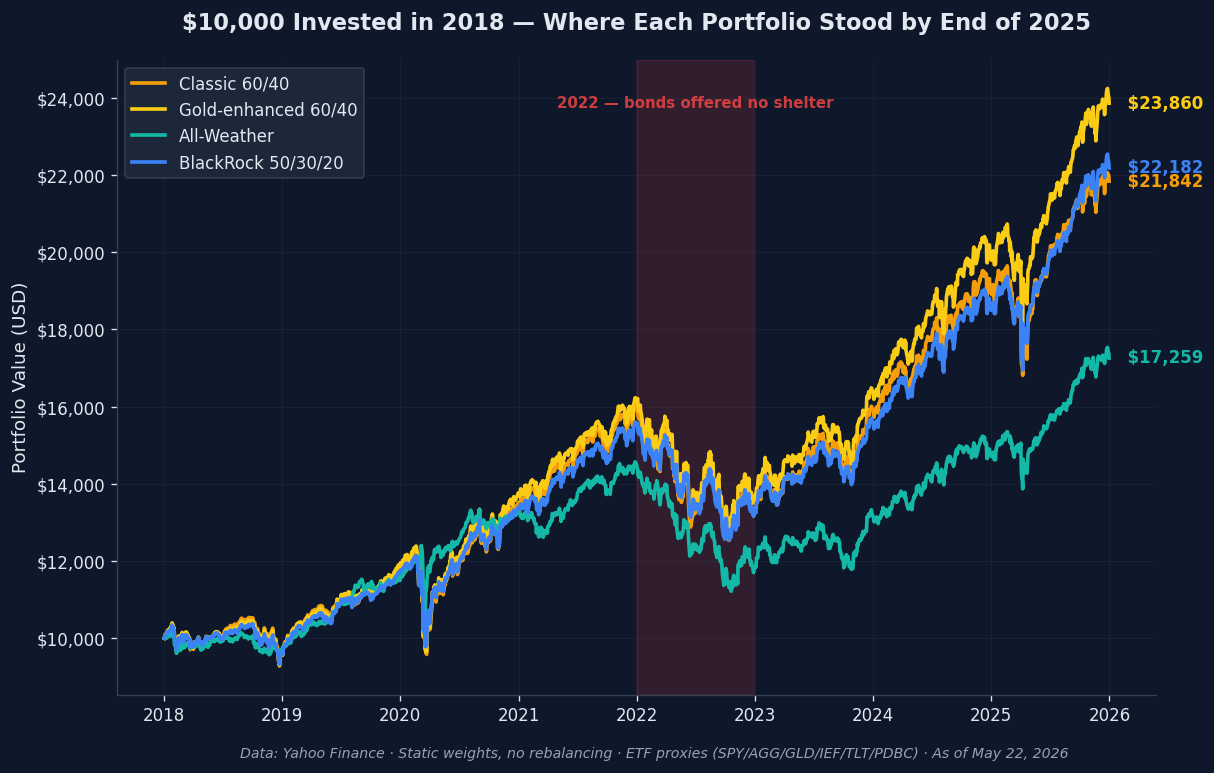

- Of the four allocation models we tested with real ETF returns from 2018–2025, gold-enhanced 60/40 led at +139%, classic 60/40 came second at +118%, and Ray Dalio's All-Weather lagged badly at +73%.

The 60/40 portfolio was built on one assumption — that bonds go up when stocks go down. In 2022, that assumption failed for the first time in 20 years. In March 2026, BlackRock said it’s permanently broken.

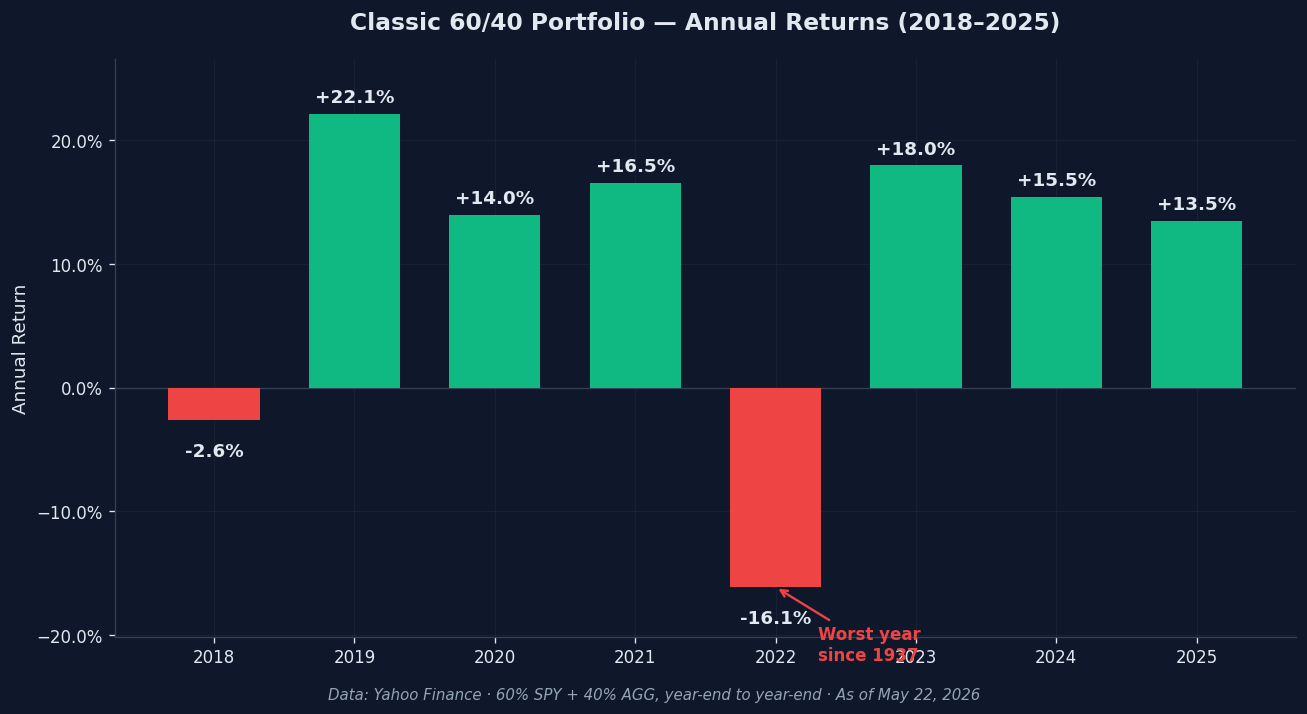

Here’s the part most coverage skips: a $100,000 classic 60/40 portfolio lost roughly 17.5% in 2022 — its worst year since 1937, per Morgan Stanley’s calculation. Different bond indices put the loss between -16% and -18%. Either way, that hit landed while inflation averaged 8.0% for the year and peaked at 9.1% in June. The real-terms drawdown was somewhere near 25% in a single year. Both ends of the portfolio went down at the same time, and the diversification math that retail investors had been taught for 30 years stopped working.

Then 60/40 returned roughly +17% in 2023, +16% in 2024, and another ~14% in 2025. So is it dead, or did it just have one bad year? BlackRock declared the 60/40 portfolio dead and proposed a 50/30/20 replacement. We took every alternative they cited — plus Ray Dalio’s All-Weather and a gold-enhanced 60/40 — and ran the actual return numbers. The answer is more useful than either side of the debate makes it sound.

The trap most guides set

When you Google “is 60/40 dead” you get two flavours of answer. The first says “it’s fine — look, it recovered.” True, but incomplete. The second says “it’s dead — buy alternatives.” Also incomplete, because nobody shows what those alternatives actually returned. You’re left with vibes and nothing to act on.

The honest question isn’t “is 60/40 dead.” It’s: what specific assumption broke, and does that assumption apply to you? If the answer changes depending on whether you’re 35 or 62, then the headline-level debate is useless. You need the underlying mechanism — and you need the numbers.

How the 60/40 portfolio actually works

The 60/40 split — 60% in US stocks, 40% in US bonds — has been the default retirement portfolio since the 1950s. The pitch was simple: stocks deliver the long-term return; bonds smooth out the ride. The whole thing rested on one statistical relationship: stocks and bonds tend to move in opposite directions during a crisis. When equities crash, investors flee to Treasuries. The Fed cuts rates. Bond prices rise. The 40% bond leg cushions the 60% equity leg, and the portfolio bounces back faster than stocks alone.

That relationship — the negative stock-bond correlation — held for roughly two decades. Then 2022 happened. The Federal Reserve hiked rates at the fastest pace in 40 years to fight inflation. Higher rates mean lower bond prices (bond math is brutal). At the same time, the rate shock spooked equities. Both legs fell together. According to State Street’s analysis, the stock-bond correlation went positive and stayed above 0.5 from 2022 through 2024 — a level that meant the bonds weren’t hedging anything.

That correlation has since normalised. It peaked at 0.80 in July 2024, then fell to 0.16 by September 2025 — not the deeply negative -0.3 to -0.5 of the 2010s, but not the crisis-level +0.8 either. Bonds are partial hedges again. Not perfect ones.

The 2026 numbers — what BlackRock and the alternatives actually propose

BlackRock’s recommendation in their March 2026 note, and again in their 50/30/20 framework BlackRock now recommends via CNBC: take 10 percentage points off equities, take 10 off bonds, put the freed-up 20% into “alternatives” — private markets, liquid alts, gold, bitcoin, emerging-market hard-currency debt. They argue the diversification benefit has to come from somewhere other than bonds, because bonds aren’t reliably hedging stocks anymore.

Two other established alternatives keep coming up in the debate: Ray Dalio’s All-Weather portfolio (30% stocks, 40% long-term Treasuries, 15% intermediate Treasuries, 7.5% gold, 7.5% commodities), and the gold-enhanced 60/40 (substitute 10% of bonds with gold). Here’s how they all stack up over the last 8 years, using real ETF prices.

| Portfolio | Composition | $10K → 8 years (end 2025) | CAGR |

|---|---|---|---|

| Gold-enhanced 60/40 | 60% SPY · 30% AGG · 10% GLD | $23,860 | +11.48% |

| BlackRock 50/30/20 | 50% SPY · 30% AGG · 10% GLD · 5% PDBC · 5% TLT | $22,182 | +10.47% |

| Classic 60/40 | 60% SPY · 40% AGG | $21,842 | +10.26% |

| All-Weather (Dalio) | 30% SPY · 40% TLT · 15% IEF · 7.5% GLD · 7.5% PDBC | $17,259 | +7.06% |

Three things jump out. First, gold-enhanced 60/40 beat classic 60/40 by 122 basis points per year — almost exactly the +140bps real-return gap that multi-decade studies show alternatives fit in with. Substituting 10% gold for 10% bonds isn’t a regime call; it’s a structural diversification upgrade that’s worked across five decades.

Second, BlackRock’s 50/30/20 essentially matched classic 60/40 in our 2018–2025 window. The 20-percentage-point alternatives bucket added defensive diversification without sacrificing return. That’s the BlackRock pitch, and the numbers actually support it — at least for the alternatives a retail investor can access (gold, broad commodities, long-duration Treasuries). The private-markets piece they recommend for institutions doesn’t show up in this comparison because most retail accounts can’t buy it.

Third, All-Weather lagged badly. The 30% equity allocation is structurally low — Dalio designed it to perform consistently across any economic regime, not to maximise returns when equities are the dominant engine. The 2018–2025 window was equity-heavy. In a different regime (1970s-style stagflation), the ranking would invert.

The 2026 numbers — limits and what’s structurally changed

The original 60/40 was designed for a different financial world. Retirements lasted 10–15 years, not 25–30. Inflation was reliably anchored around 2% (or even below). The Fed always cut rates in a crisis, which made bonds the perfect hedge. Most of that has changed.

What’s actually different in 2026: the 10-year Treasury yields around 4.6% (the 30-year sits above 5%). That’s the highest sustained level since 2007. The bond leg of 60/40 actually earns real returns again — back in 2020, when 10-year yields sat near 0.9%, the 40% bond allocation was a return-free risk bucket. That’s not the situation today. A bond yielding 4.6% can absorb a small rate move and still deliver a positive total return.

The flip side: inflation hasn’t fully gone away. Core inflation has been sticky in the 3% range, and any sustained reflation would re-correlate stocks and bonds the way 2022 did. That’s the case BlackRock is making — not that 60/40 is dead in absolute terms, but that the assumption it was built on (negative stock-bond correlation in a low-inflation regime) is no longer reliable. The alternative bucket is insurance against the regime shift.

Where investors get this wrong

Mistake 1: Reacting to one bad year by abandoning the model. The 60/40 portfolio’s 2022 drawdown was its worst since 1937. It was also followed by three consecutive years of double-digit returns. An investor who panicked out of 60/40 in late 2022 and parked in cash missed roughly a 50% cumulative recovery. That’s not a hypothetical — it’s what would have happened to anyone who treated “60/40 is dead” as a sell signal.

Mistake 2: Adding “alternatives” without understanding what you’re actually buying. BlackRock’s 20% alternatives bucket sounds clean. In practice, it includes private markets that most retail investors can’t access (or pay 2-and-20 fees for if they can), hedge-fund liquid alts that have lagged simple index portfolios for a decade, and bitcoin exposure that adds volatility most retirement portfolios don’t need. The retail-accessible version is the gold and commodities slice — and that piece does work, as the gold-enhanced 60/40 numbers above show.

Mistake 3: Ignoring your own timeline. A 35-year-old with 30 years to retirement and a 25-year-old’s risk tolerance has no business in a 60/40 portfolio at all — they should be closer to 90/10 with a far heavier equity tilt. The same person at 62, three years from drawing income, faces a sequence-of-returns risk that 60/40 was specifically built to address. The withdrawal rate math that drives a sustainable retirement requires at least 50% equities to function — which means even a “conservative” retiree shouldn’t drop below 50/50. The same allocation, two completely different decisions, depending on your timeline. The way you split your equity exposure matters at every age, but the equity-vs-bond split matters most as you approach retirement.

The bottom line

BlackRock is half right. The assumption behind the classic 60/40 portfolio — that bonds reliably hedge stocks — is materially weaker than it was a decade ago. The stock-bond correlation can flip positive in an inflation shock, and 2022 proved that the diversification math fails exactly when you need it most.

But “the assumption is weaker” is not the same as “the portfolio is dead.” Three simple takeaways from the numbers:

- If you’re more than 20 years from retirement, the 60/40 question is the wrong one — you should be far heavier in equities. Pick a 90/10 or 80/20 and ignore the BlackRock debate entirely.

- If you’re inside 10 years from retirement and 60/40 is your benchmark, the cleanest upgrade is to substitute 10 percentage points of your bond allocation for gold. The 8-year numbers show +122bps of annual outperformance; multi-decade studies show closer to +140bps. Same risk profile, better diversification, accessible through a single ETF (GLD or IAU).

- The full BlackRock 50/30/20 framework only adds value over the gold-enhanced 60/40 if you can access the private-markets and hedge-fund pieces. Most retail investors can’t, which means the marginal benefit of moving beyond the gold-enhanced version is small.

The 60/40 portfolio isn’t dead. The assumption it was built on is weaker than it was — and the fix is one ETF, not a wholesale portfolio rebuild.

Going deeper

- The 4% Rule: How Much You Need to Retire (2026) — the withdrawal-rate math that determines whether your 60/40 (or any other allocation) actually lasts 30 years.

- Dividend ETFs vs Growth ETFs: Which Wins Over 20 Years? — once you’ve picked your stocks-to-bonds split, the next question is which kind of equity exposure to hold.

- Roth vs Traditional IRA: The Breakeven Math Nobody Shows You — your account type affects which allocation makes sense; tax-deferred vs tax-free changes the math.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!