- The SG rate is 12% as of 1 July 2025 — the final scheduled step. From 1 July 2026, employers pay every payday under Payday Super.

- Modern ‘Balanced’ options run 70–85% growth assets. The label hasn’t caught up with the asset mix.

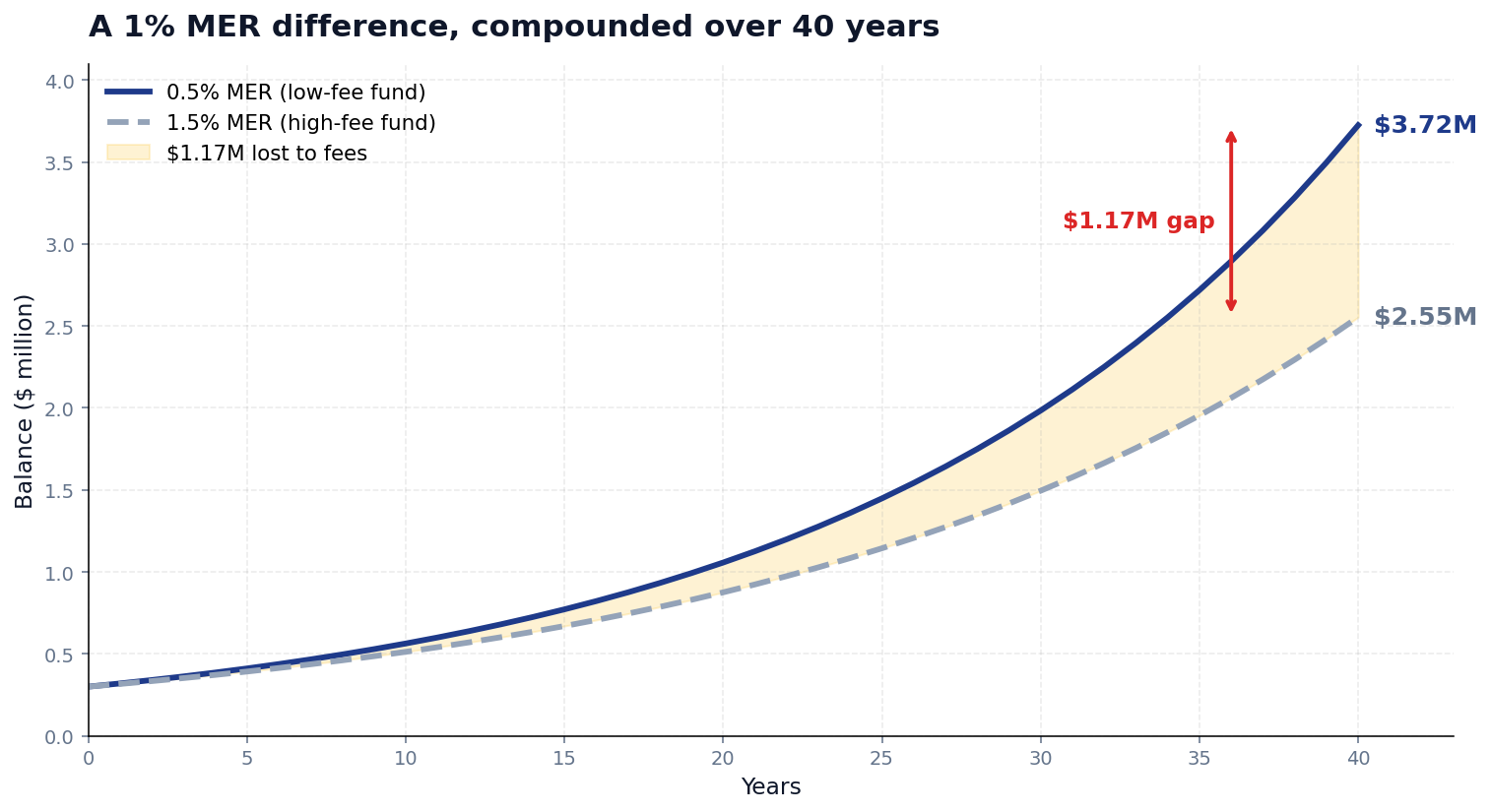

- A 1% MER difference on a $300k balance compounds to roughly $1.18 million in lost growth over 40 years.

Around 17 million Australians have a superannuation account. Most have never opened it. Understanding how superannuation works isn’t optional — over a working life this becomes the second largest asset you’ll ever own, and the decisions you didn’t make about it compound silently for four decades.

Why this matters more than your salary negotiation

The compounding asymmetry is the part nobody emphasises in school. Your annual pay rise is gone the moment it hits your account. A one-percentage-point difference in your super fund’s management fee, by contrast, compounds at the same rate as the market itself — for forty years.

Run the numbers on a $300,000 balance at 7% gross annual returns. A fund charging 0.5% MER grows to roughly $3.73 million over 40 years. A fund charging 1.5% MER grows to $2.55 million. That’s not a $40,000 fee drag or a $120,000 one. It’s $1.17 million in foregone retirement, paid quietly through quarterly statements nobody reads.

The contributions side has its own quiet structural change happening. The Super Guarantee rate reached 12% on 1 July 2025, the final scheduled step in a multi-year increase from 9%. That number isn’t rising further. But from 1 July 2026, Australia switches to Payday Super — employers must remit contributions every payday rather than quarterly. The rate stays at 12%; the change accelerates compounding by getting contributions invested weeks earlier than the current system allows. Worth knowing because the marketing copy your fund sends will conflate the two reforms.

How superannuation works under the hood

A super fund is, mechanically, a pooled investment vehicle. Your employer deposits 12% of your ordinary time earnings into the fund. The fund — regulated by APRA for prudential supervision and the ATO for contributions and tax — pools that capital with millions of other members and invests it across asset classes according to whichever investment option you (or, more likely, your default) have selected.

Returns are reported as unit prices, calculated net of investment fees and net of the 15% tax that super funds pay on earnings in the accumulation phase. Contributions come in three flavours: employer SG (mandatory, 12%), voluntary concessional (salary-sacrificed pre-tax, capped at $30,000 per year through 2025–26), and non-concessional (after-tax). Everything inside the fund grows in a 15% tax environment until you retire, at which point earnings on the first $2m (the transfer balance cap, indexed periodically) drop to zero tax.

The four investment options — and why the names mislead

Most funds offer four pre-mixed options, ordered by growth allocation:

- Conservative (~30% growth / 70% defensive) — weighted to fixed interest and cash, with a small equities sleeve

- Balanced (typically 70–80% growth / 20–30% defensive)

- Growth (~85% growth / 15% defensive)

- High Growth (~90%+ growth) — mostly equities, often with a private equity sleeve

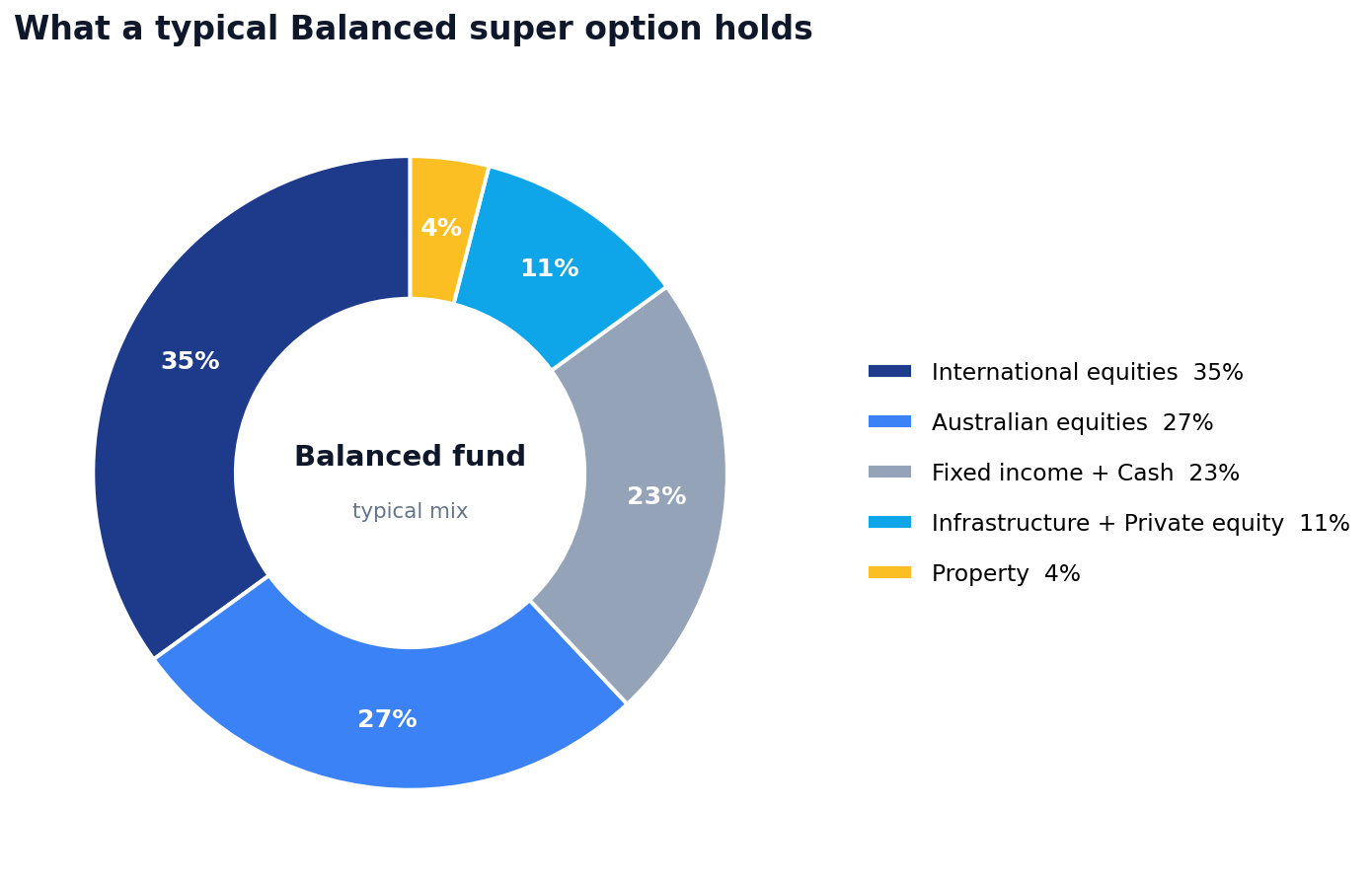

Here’s the part the label doesn’t advertise: modern “Balanced” options aren’t especially balanced. Industry data shows every Top 10 MySuper “Balanced” default is now running at 85%+ growth assets. The name dates from a time when defensive assets paid meaningful real yields. They mostly don’t any more, so funds have quietly shifted the asset mix without renaming the product. A 55-year-old in a “Balanced” default who assumes they’re conservatively positioned may actually be holding 85% equities and 15% fixed income.

The asset class mix inside a typical Balanced fund looks roughly like this:

The single biggest exposure is international equities — roughly a third of the portfolio, typically held through index ETFs or institutional mandates that track them. (VOO and VTI, two of the largest US ETFs, sit inside many Australian super funds’ international equity sleeves.) Australian equities come second, then a mix of unlisted infrastructure and private equity, then fixed income and cash for ballast. Property is usually the smallest line because direct property has gone out of fashion since 2022.

Who actually manages the money

Industry funds — AustralianSuper, Aware, UniSuper, Cbus, HESTA — mostly run hybrid models: in-house investment teams handling Australian equities, infrastructure and private equity, with external specialist managers for international equities, credit and emerging markets. Retail funds (the bank-owned ones) historically outsourced more, though that’s shifted post-Royal Commission as fees came under pressure.

The structural advantage industry funds have is unlisted assets. They’re large enough to take direct stakes in airports, toll roads, office towers and unlisted infrastructure deals that retail investors can’t access at any price. Whether that’s a real return advantage or a valuation timing trick is its own debate — unlisted assets aren’t marked daily, which can mask drawdowns that listed equivalents show in real time.

How an algorithm would pick your super fund

This is where the systematic lens earns its keep. Most super-fund “reviews” rank funds by last year’s return, which is roughly the worst possible filter (last year’s top performer is, on average, next year’s middle of the pack). A quant approach to the same selection problem looks completely different.

1. Fee drag as guaranteed negative return

Treat the MER as a known, certain headwind. Your expected net return is gross return − MER − admin fees. The gross return is uncertain. The fees are not. APRA’s 2025 benchmark fee data shows the median MySuper product charging just 0.25% in administration fees, with platform-based trustee-directed products running at 0.59%. Anything materially above 0.70% all-in is paying for distribution or active management you may not need.

2. Mean-variance optimisation across asset classes

Modern portfolio theory boils down to: for any target risk level, there’s an optimal mix of asset classes that maximises expected return. Super funds run this calculation internally and offer the result as their Balanced / Growth / High Growth products. The question for a member is which point on the efficient frontier matches your risk tolerance and time horizon — not which fund’s product was rebranded most aggressively.

3. Monte Carlo age-gating

This is the one almost no default option handles. A 25-year-old with 40 years to retirement should mathematically hold close to 100% equities — the variance of 40-year compound returns on equities is lower than the certainty of being underweight growth for four decades. A 55-year-old with 10 years to retirement faces sequence-of-returns risk that the 25-year-old doesn’t: a 30% drawdown three years from retirement is materially different from a 30% drawdown 35 years out.

A Monte Carlo simulation across 10,000 paths bakes this asymmetry into the recommendation. Most default Balanced options ignore your age entirely — you get the same asset mix at 22 and at 64. That’s a feature of the regulatory regime (MySuper rules require a single default), not a feature of good investing.

4. The screener approach — what we look for

The same logic the Luna3 stock screener applies to equities applies to super fund selection: define the filter criteria, then rank surviving candidates. A reasonable filter list:

- 10-year net return above the MySuper median (signals competent investment management, not just one good year)

- Total MER below 0.70% (above this you’re paying for distribution, not return)

- Investment option granularity — at minimum: Conservative, Balanced, Growth, High Growth, plus single-asset-class options (Australian shares, international shares, fixed income) for members who want to build their own mix

- Insurance opt-down available — you should be able to reduce default cover without leaving the fund

- Passed the APRA performance test for the most recent 3 years (a low bar, but funds that fail it have demonstrated they can’t even beat their own self-selected benchmark)

Run that filter against the APRA fund-level data and the universe of 50+ MySuper products narrows to maybe a dozen. Pick by 10-year net return within that surviving group. That’s the entire decision — a thirty-minute exercise that, for most members, will be the highest-return half hour they spend on personal finance in their working life.

Where most Australians get this wrong

Five patterns repeat in the ATO and APRA data:

1. Staying in the default option forever

If you started work before November 2021, your fund was almost certainly chosen by an employer’s default. Since stapling reform began, your existing fund follows you to new jobs — which solves one problem (account proliferation) but doesn’t solve the deeper one: the default investment option inside that fund is unlikely to be optimal for your specific age and risk tolerance. The default exists to satisfy regulation, not to maximise your outcome.

2. Ignoring the fee number

A 1.5% MER fund versus a 0.5% MER fund is a guaranteed 1% per year of underperformance before investment skill enters the equation. The active manager has to add 1%/year after fees just to match the index fund. Most don’t. The data on this is unambiguous and has been for decades.

3. Picking “Balanced” because it sounds prudent

The name was invented decades ago for a 60/40 split that no longer exists. A 25-year-old in “Balanced” is often more conservatively positioned than is optimal for their horizon. A 58-year-old in a modern 85%-growth “Balanced” option may be more aggressively positioned than they realise — particularly in a sequence-of-returns scenario where a drawdown in the five years before retirement permanently damages the outcome.

The fix is to read the actual asset allocation, not the product label. If you want 60/40, look for a fund that actually offers 60/40.

4. Not consolidating multiple accounts

The stapling reform in November 2021 fixed most of the duplicate-account problem — 79% of Australians now have a single super account as of June 2025, up from 76% in 2022. But that still leaves around 1 in 5 holding multiple accounts. Each one charges its own admin fee, and most carry default insurance premiums you may have forgotten you’re paying. Consolidating through the ATO portal takes about ten minutes and is the most reliably profitable ten minutes of admin most people will ever do.

5. Auto-paying for the wrong insurance

Default insurance inside super is opt-out by design — you have it unless you cancel it. Whether it’s good value depends sharply on which cover type. ASIC’s default insurance review found average claims ratios of 87% for TPD, 80% for death cover, but only 61% for income protection. Income protection is the weakest line item: members are paying $1 in premiums to receive 61 cents in eventual claims on average, with the difference funding insurer costs and margins.

The right action depends on your situation. A 25-year-old with no dependants probably needs less death cover than the default. A 45-year-old with a mortgage and two kids probably needs more. A self-employed contractor may be better off with standalone income protection outside super, where premiums are tax-deductible and definitions tend to be more generous.

The bottom line

Super is the only investment portfolio most Australians own, and it’s the only one they never check. Understanding how superannuation works — what the fund actually holds, what it charges, and how the default differs from what would be optimal for your age — isn’t about chasing the top-performing fund of the year. It’s about removing the structural drag points: high fees, mismatched age-appropriate allocation, duplicate accounts, and insurance you didn’t choose.

Do that thirty-minute audit once and the compounding does the rest of the work for forty years.

Going deeper

- VOO vs VTI: Which Vanguard ETF Actually Makes More Sense? — the same index ETF mechanics that sit inside most super funds’ international equity allocation

- Pepperstone vs IC Markets 2026 — if you want to manage capital outside super, broker selection follows the same fee-drag and execution-quality logic as fund selection

- ASIC MoneySmart on super investment options — the regulator’s plain-English reference for option types and risk profiles

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!