- Apollo's $25B Apollo Debt Solutions fund capped redemptions at 5% of NAV on March 23, 2026, after investors asked for 11% — the first hard gate in retail private credit's modern era.

- The transmission mechanism wasn't credit losses. It was a structural mismatch between 90-day retail redemption windows and 1,800-day underlying loan tenors. The gates aren't a bug — they're the prospectus working as designed.

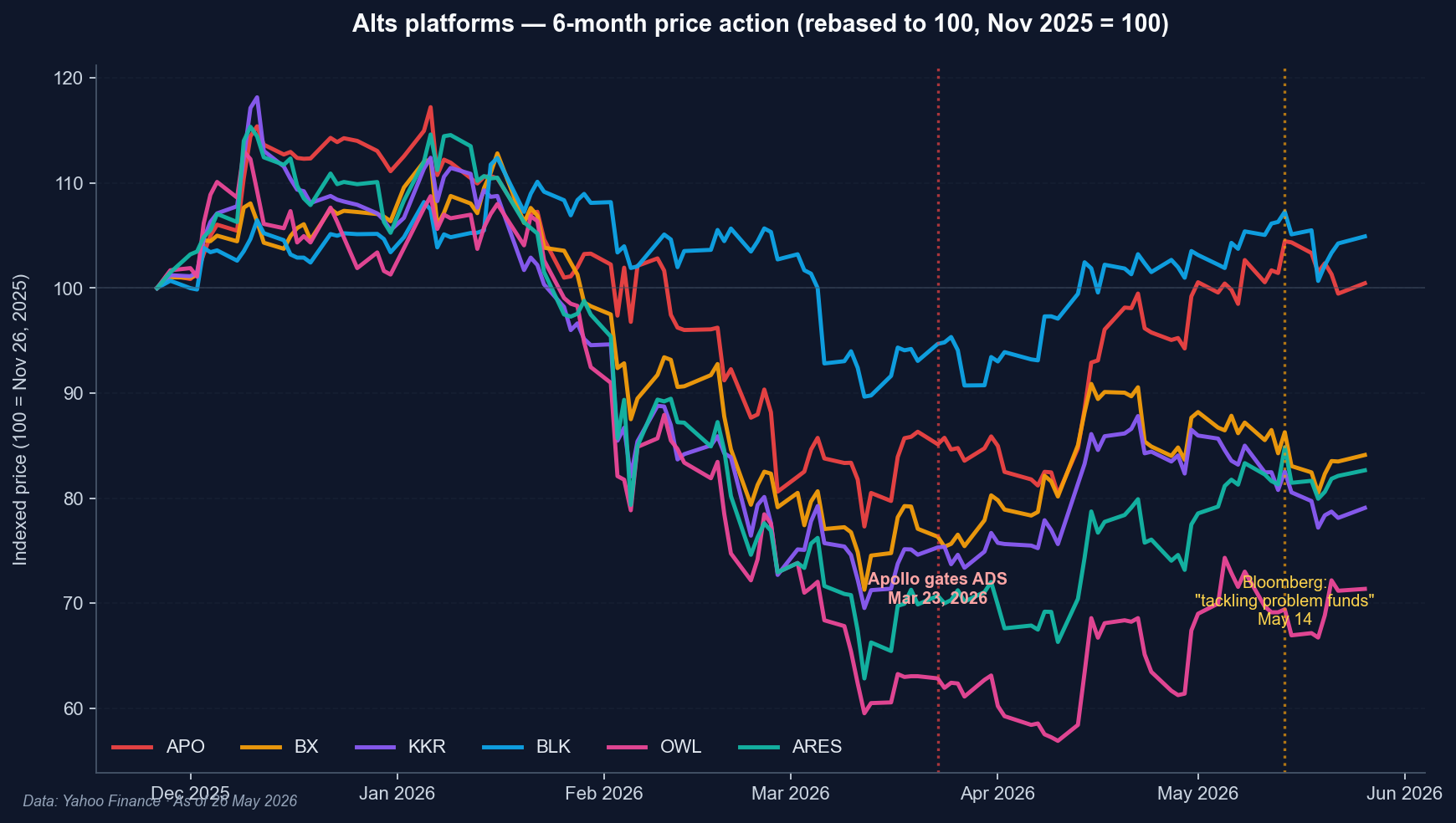

- Goldman Sachs forecasts retail private credit could shed $45–70 billion in AUM over the next two years. The GP-equity cohort (APO, KKR, BX, BLK, OWL, ARES) is repricing the asset-gathering story accordingly.

On March 23, 2026, Apollo Global Management told the holders of its $25 billion Apollo Debt Solutions fund that they could not have all their money back. ADS — a non-traded business development company that had been pitched to retail investors with words like “evergreen” and “income” — capped redemptions at 5% of net asset value for the quarter after receiving requests for 11%. Six weeks later, Bloomberg reported that KKR, Apollo, and BlackRock were all “tackling problem funds.” Blackstone’s BCRED — the largest retail private credit vehicle in the market — saw 7.9% of investors ask for their money back in a single quarter and quietly raised its cap from 5% to 7%, with Blackstone and its employees adding $400 million of their own capital to meet the shortfall.

The private credit crisis that finally arrived in Q1 2026 isn’t really a credit story. It’s a plumbing story — and the plumbing was always going to do this.

Apollo — the firm at the centre of the gate — last printed $128.51 going into publication on May 26, 2026, roughly 8% below where it traded the day before the ADS announcement and 20% off its 12-month high. We’ll come back to why the GP-equity reaction has been more measured than the underlying fund stress would suggest.

The setup — how private credit went retail

The total private credit market — direct lending, mezzanine, distressed, opportunistic — is now roughly $1.8 trillion globally, with $1.3–1.4 trillion based in the US per Federal Reserve data cited in Vice Chair Bowman’s May 8 speech. Most of that capital still belongs to pension funds, endowments, and insurance companies — investors who locked their money up for 7-to-10 years on day one and never expected to see it before the fund’s term ended.

The slice that broke in Q1 2026 is much smaller. Fortune’s reporting on the “$265 billion meltdown” refers specifically to the retail-accessible portion — non-traded BDCs, interval funds, and tender-offer evergreen vehicles sold through advisor channels and platforms like iCapital, CAIS, and the major wirehouses. That’s the universe we mean when we say private credit “went retail”:

- Non-traded BDCs — closed-end vehicles that file with the SEC, mark their portfolios quarterly, and offer share repurchase tender offers up to ~5% of NAV per quarter. ADS and BCRED are both in this bucket.

- Interval funds — closed-end ’40 Act funds with a mandatory repurchase offer at a stated interval (usually quarterly), capped at 5–25% of shares.

- Evergreen tender-offer vehicles — perpetual structures with discretionary tender offers. The most flexible wrapper from the manager’s standpoint, the least liquid from the investor’s.

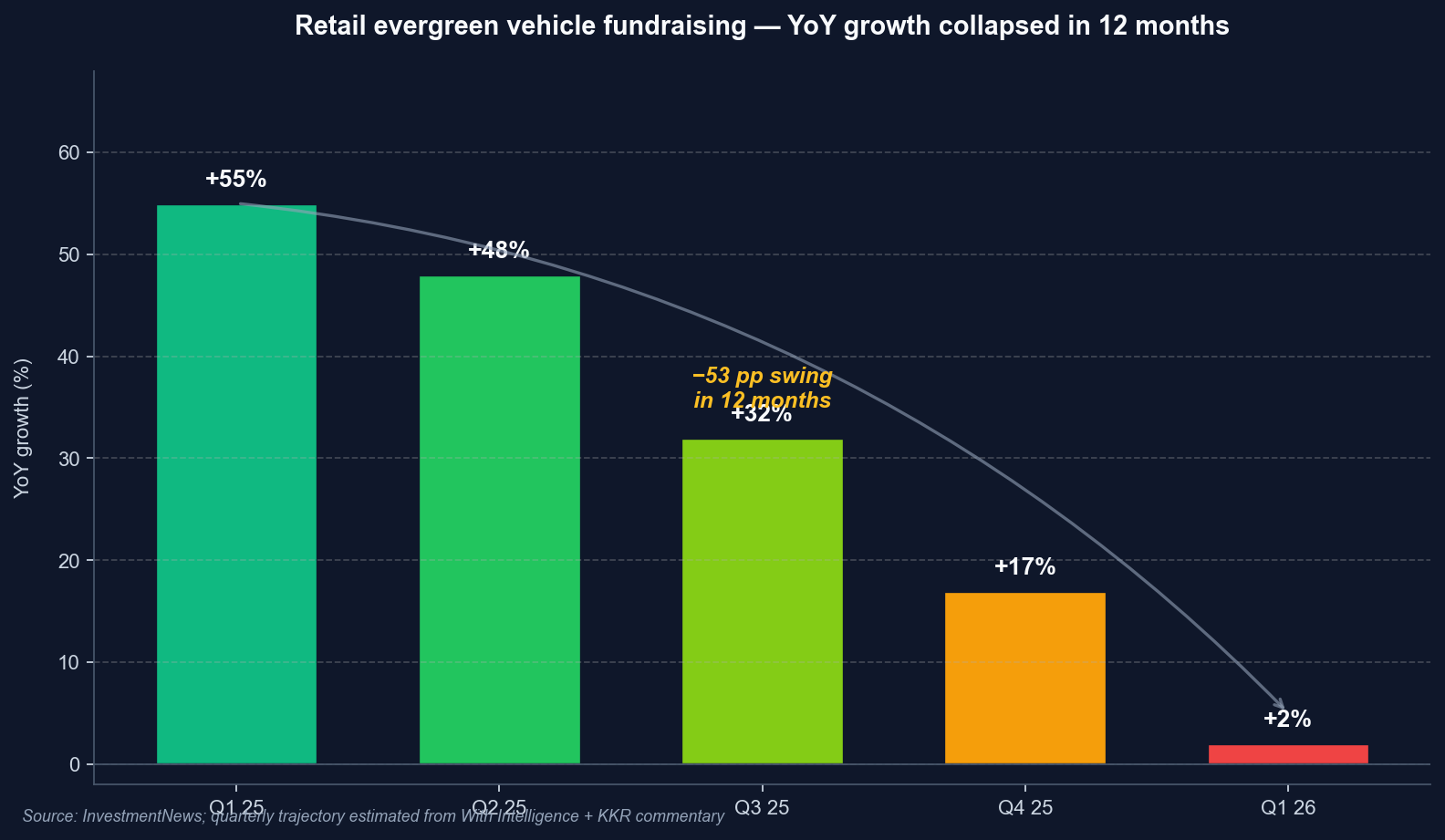

All three wrappers were sold against the same pitch: 8–11% target yields, monthly distributions, a quarterly NAV print, and the institutional asset class that had outperformed public credit for a decade. They scaled fast. Capital into retail-accessible evergreen vehicles — counting private equity, venture, and credit together — grew 55% year-on-year in Q1 2025. By Q1 2026 it was up just 2%, per InvestmentNews. That’s a 53-percentage-point swing in 12 months, and the gates hadn’t even started when the fundraising slowed.

This is the natural rhyme with the 60/40 alternative-allocation pitch that’s been running for three years: when public bond returns disappointed in the post-2022 rate environment, advisors reached for private credit yields as the substitute. The reach worked beautifully in the bull market. It works less well when redemption queues form.

How the private credit crisis unfolded

Three things matter about the Q1 2026 cohort: who actually gated, who strained but didn’t, and what Bloomberg meant when it described the industry as “tackling problem funds.”

Apollo: the hard gate (March 23, 2026)

Apollo Debt Solutions is the only fund in the cohort that ran a formal gate this cycle. The $25 billion BDC received redemption requests totalling 11% of NAV for the Q1 tender offer window and accepted only 5% — the prospectus-stipulated cap. The remaining 6% of requests were prorated and rolled to the Q2 window, where the same cap applies. Apollo confirmed the cap publicly on March 24.

The reaction in the GP equity was telling. APO sold off ~8% in the week after the announcement but recovered most of it within a month. Investors had already priced in the broader narrative; the ADS gate confirmed it rather than introducing new information.

Blackstone BCRED: the soft strain

BCRED is a different story. Blackstone Private Credit Fund is the largest non-traded BDC in the market — roughly $45 billion in equity NAV against an $80 billion gross investment portfolio across nearly 700 issuers — and Q1 2026 redemption requests reached 7.9% of NAV, or about $3.7 billion. Rather than gating, Blackstone raised its quarterly cap from 5% to 7%, then closed the residual gap by injecting roughly $400 million of Blackstone Inc. and employee capital into the fund.

The mechanics matter. A $400 million capital injection from the manager isn’t a loss — Blackstone bought NAV at NAV and now owns more of a fund it controls. What it bought was reputation: BCRED ran a normal Q1 tender process, returned everyone’s money, and avoided the “gate” headline that hit ADS. Blackstone shares — which we’ll come back to in the public-ticker map below — are down materially over six months, but the BCRED-specific reputational damage was contained.

KKR and BlackRock: working through

Bloomberg’s May 14 piece framed KKR and BlackRock as part of the same cohort dealing with redemption stress — but neither has run a formal gate event of its own through Q1 2026. KKR’s retail-credit footprint is meaningfully smaller than Apollo’s or Blackstone’s; its 2026 inaugural End-Investor Survey reads more like a marketing pivot than a stress disclosure. BlackRock’s private credit fund follows standard quarterly tender mechanics and has not, on the public record, breached its cap.

What “tackling problem funds” appears to mean in practice is a workout phase on individual loans within the cohort’s portfolios — restructuring software-sector borrowers whose enterprise value AI is quietly eroding, extending duration on names that can’t refi, marking down equity kickers that won’t print. That’s not a liquidity event. That’s the credit work that always happens when a rate cycle turns. It’s just happening in vehicles where retail can see the marks.

The mismatch — why this was always going to happen

The structural argument is easier to see in a diagram than in prose. Retail capital flows into the wrapper expecting weekly visibility and quarterly liquidity. The wrapper deploys that capital into senior secured loans to PE-owned mid-market companies — loans with stated tenors of 4 to 7 years that mostly don’t amortise meaningfully until year three. Then the fund has to figure out how to settle a 90-day redemption obligation from an asset base that, by design, settles in 1,800 days or more.

Three mechanisms close the gap in normal times. First, new subscriptions: as long as new money flowing in exceeds old money flowing out, the fund pays redemptions from inflows rather than from asset sales. Second, a cash and liquid-investment sleeve, typically 10–20% of NAV, held in syndicated loans, public credit, or Treasuries. Third, secondary sales — selling loans to other private credit funds or back to the syndicated market.

All three mechanisms compress simultaneously in stress. Subscriptions slow exactly when redemptions spike. The cash sleeve gets drawn down to the bone. And secondary loan sales force the fund into a price-discovery event that mechanically reveals the NAV-vs-mark gap — the very thing the appraisal-based NAV process was designed to smooth. The 5% quarterly cap is the prospectus saying: if all three mechanisms compress at once, we will not be selling the loan book at a discount to make you whole. We will queue you instead.

Institutional LPs accepted this trade-off explicitly when they signed the LP agreement. They expected an illiquidity premium, they got a multi-year lock-up, and they don’t generally call back capital during stress because their pension actuaries told them not to. Retail investors got the same illiquidity terms — in the prospectus, in plain English — and most didn’t read it. The gate is the moment the trade-off stops being abstract.

Where the money flows — the public-ticker map

The Private pillar at Luna3 will always name the public beneficiaries. In this case, the beneficiaries — and the names taking the price hit — are the publicly-traded general partners that own the fund-management businesses. They earn money in two ways: management fees on assets under management (sticky, recurring, paid even when the fund underperforms) and performance fees / carried interest (cyclical, paid when underlying funds realise gains above hurdle).

The distinction matters because the GP equity (ticker APO) trades differently from the BDC equity (ticker AINV in Apollo’s case, ARCC for Ares, ORCC for Blue Owl, etc.). The GP collects fees off committed capital regardless of NAV drift — Apollo will earn its management fee on ADS in Q2 2026 whether or not the prorated redemption queue clears. The BDC is the entity carrying the actual loans on its balance sheet. The fees get paid first, the residual returns flow to BDC shareholders.

Here’s the six-month tape across the cohort, with management-fee structure context for each:

| Ticker | Company | Pub price (May 26) | 6-mo move | Fee model relevant to retail credit |

|---|---|---|---|---|

| APO | Apollo Global Management | $128.51 | ~flat | ADS management fee (~1.0% of NAV) + incentive on 5% hurdle |

| BX | Blackstone | $118.51 | −16% | BCRED management fee (1.25% of NAV) + 12.5% income incentive |

| KKR | KKR & Co. | $94.04 | −21% | Smaller direct retail credit footprint; broader alts platform leverage |

| BLK | BlackRock | $1,073 | +5% | Largest by AUM, smallest by retail-credit % of revenue; least cohort-sensitive |

| OWL | Blue Owl Capital | $10.06 | −29% | Most concentrated in direct lending; retail-credit beta is highest |

| ARES | Ares Management | $124.41 | −17% | ARCC (publicly-traded BDC) is the visible mark; private BDCs scaling |

The dispersion within the cohort is the interesting signal. BLK is up because retail credit is a marginal slice of a $13.9 trillion AUM platform — the iShares ETF business and the institutional-allocation engine dominate. APO is flat because the market priced in the gating risk months before it happened. OWL is down 29% because Blue Owl’s revenue mix is concentrated in exactly the direct-lending product that is now under redemption pressure, with less of a diversified-fees buffer than Blackstone or Apollo.

Second-derivative beneficiaries also exist on the public side, though more diffuse. Traditional banks (JPM, GS, MS, WFC) are quietly reclaiming middle-market lending share from the private credit complex in segments where their balance sheet rules permit. The same retail flow rotation that walked $640B out of active equity funds last year is now starting to walk capital out of high-fee alternative wrappers and back toward lower-cost diversified products. We’ll come back to that thread in a future post — it’s the next-leg story.

The bear case — what could make this worse

Counter-arguments are non-negotiable on this kind of post. There are four ways the Q1 2026 stress could metastasise into something larger:

- NAV markdowns prove understated. Non-traded BDC NAVs are appraisal-based, not transaction-based. If a syndicated-market dislocation forces a public price-discovery event on a representative portion of a fund’s portfolio — for example, a $500M secondary loan sale priced at 92¢ — every other fund holding the same paper has to mark in sympathy. That could catalyse a redemption avalanche where the marked NAV no longer reflects the realisable value of the underlying assets.

- Rates fall faster than expected. Private credit revenue is dominated by floating-rate loans (SOFR+spread). A rapid Fed easing cycle drops the coupon income before the spread tightens, and distribution coverage gets uncomfortable for non-traded BDCs that pay near-current income out. Distribution cuts triggered the 2008–09 mortgage-REIT collapse via the same mechanism.

- Private equity’s terminal-value problem hits. Direct lending portfolios are concentrated in PE-owned mid-market companies. Recent vintages have been exiting at ~2.0× cost MOIC versus the ~2.5× implied in mark-to-market valuations. If the gap is structural rather than cyclical, equity kickers and back-end fees stop printing — and back-end fees are where the alts GPs make their carried interest.

- Regulatory tightening. The SEC’s marketing-rule scrutiny on private fund disclosures has been escalating since 2024. FINRA suitability reviews on retail private-credit sales are already underway. Higher disclosure burden compresses retail demand; tougher suitability rules shrink the addressable advisor channel. Either change reduces the AUM growth path the GP-equity multiples currently capitalise.

Goldman Sachs analysts have publicly modelled the retail private credit AUM trajectory and estimate the asset class could shed $45–70 billion over the next two years if retail investors continue to step back. The forecast assumes no catastrophic credit losses — purely a behavioural unwind of the retail-channel growth trajectory. The fundraising data we showed earlier suggests Goldman’s range is the central case, not the bear case.

What we’re watching

- Q2 2026 fundraising prints. Q1 retail-evergreen growth collapsed from +55% YoY to +2% YoY. Q2 confirms the trajectory or signals stabilisation. The major data points land in late July with the next set of 13F-equivalent disclosures and direct-lending-index updates.

- BCRED Q2 tender-offer take-up. Did Blackstone’s raised 7% cap clear the residual queue? If a second injection is needed in Q2, the “soft strain” narrative starts to look more like “managed gate.”

- Publicly-traded BDC discount-to-NAV. ARCC, ORCC, OBDC, and FSK trade in real time. Their discounts are the best leading indicator of where non-traded BDC NAVs will reset over the next two quarterly windows. A widening discount on the publicly-traded names typically precedes mark adjustments at the non-traded names by 60–90 days.

- The next firm joining the cohort. Ares (ARES) and Blue Owl (OWL) are the two names with the largest retail credit beta outside the cohort that already disclosed Q1 stress. A public gating event from either would suggest the issue is broader than the Apollo / Blackstone narrative implies.

- StepStone × PitchBook private-markets transparency launch. Announced May 6, scheduled to launch in Q2 2026, the partnership puts deal-level performance and operating metrics across PE, VC, growth, and infrastructure into a single anonymised dataset. It’s the first time retail-channel allocators will be able to benchmark private fund NAVs against deal-level comparables in something close to real time. If the data shows persistent NAV-vs-realisable gaps, the redemption queue gets longer.

- KKR End-Investor Survey follow-ups. The inaugural 2026 print found 42% of non-investors cite “lack of knowledge” as the barrier to entry. Does the next survey, post-gate, show that share rising — and if so, does it correlate with redemption behaviour?

The bigger picture sits inside the credit cycle’s current position: rates are easing modestly, defaults remain low, the syndicated loan market is functioning. None of those preconditions are screaming distress. What broke in Q1 2026 was a wrapper, not the underlying asset class. But wrappers that misalign liabilities with assets tend to break the same way every time the cycle turns — and the next wrapper, the next product, the next retail-channel push will face the same arithmetic.

For now, Apollo Debt Solutions ran its prospectus exactly as written. BCRED ran a tender, raised a cap, and stayed standing with a $400M nudge from the house. KKR and BlackRock are doing the workout work that loan portfolios always need at this point in a cycle. The crisis is real. It just isn’t, on the public record, a credit crisis yet.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!