- Hold a stock for one year or less and you owe ordinary income tax on the profit — the same rate as your salary. Hold for at least 366 days and the IRS taxes it at a separate, lower schedule: 0%, 15%, or 20%.

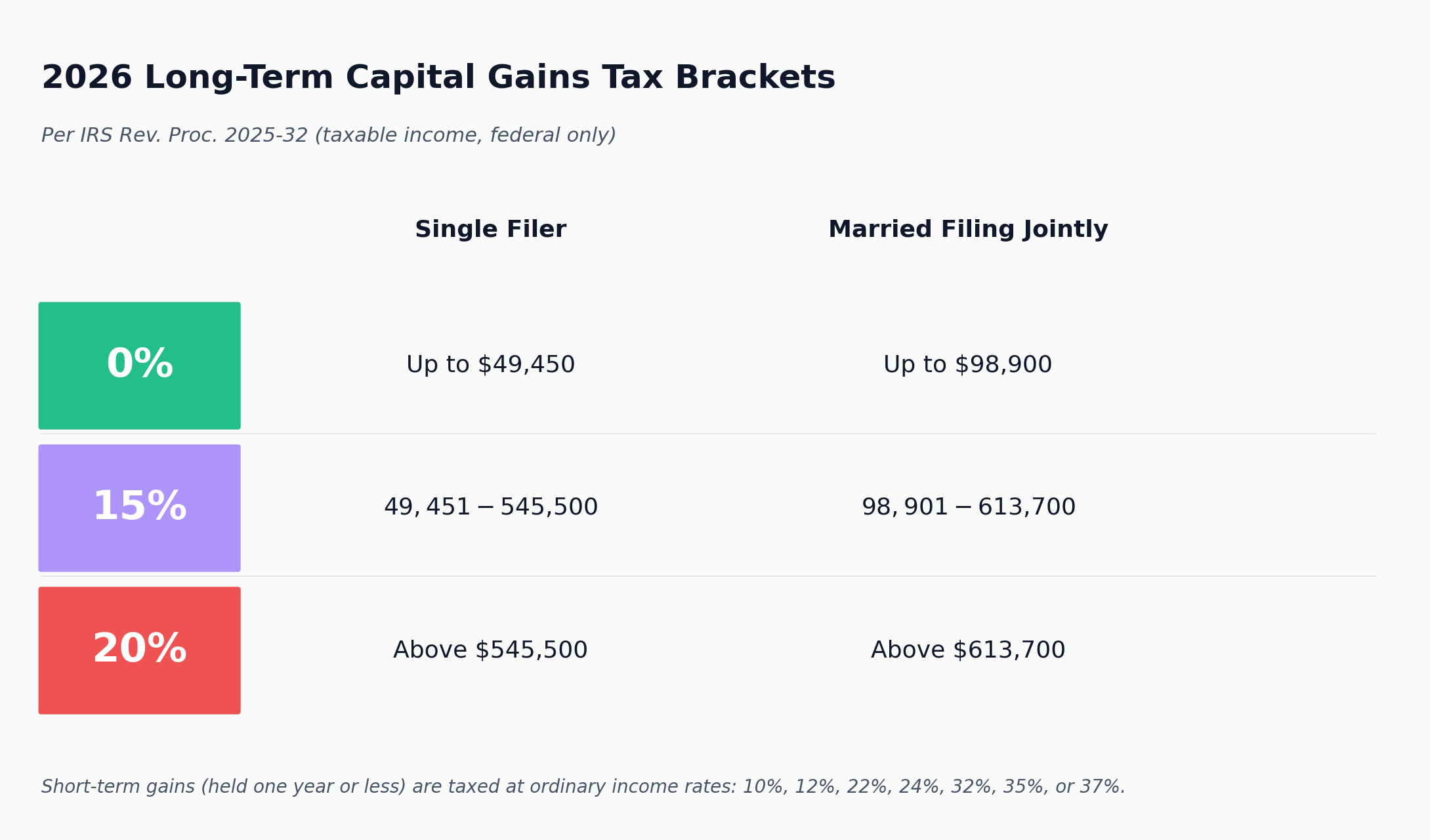

- In 2026, a single filer with taxable income up to $49,450 pays 0% on long-term capital gains. Married filing jointly: up to $98,900. The bracket is real, not theoretical.

- Three retail-actionable levers cut the bill: hold for 366+ days, tax-loss harvest losing positions (watch the wash-sale rule), and hold appreciating assets inside tax-advantaged accounts.

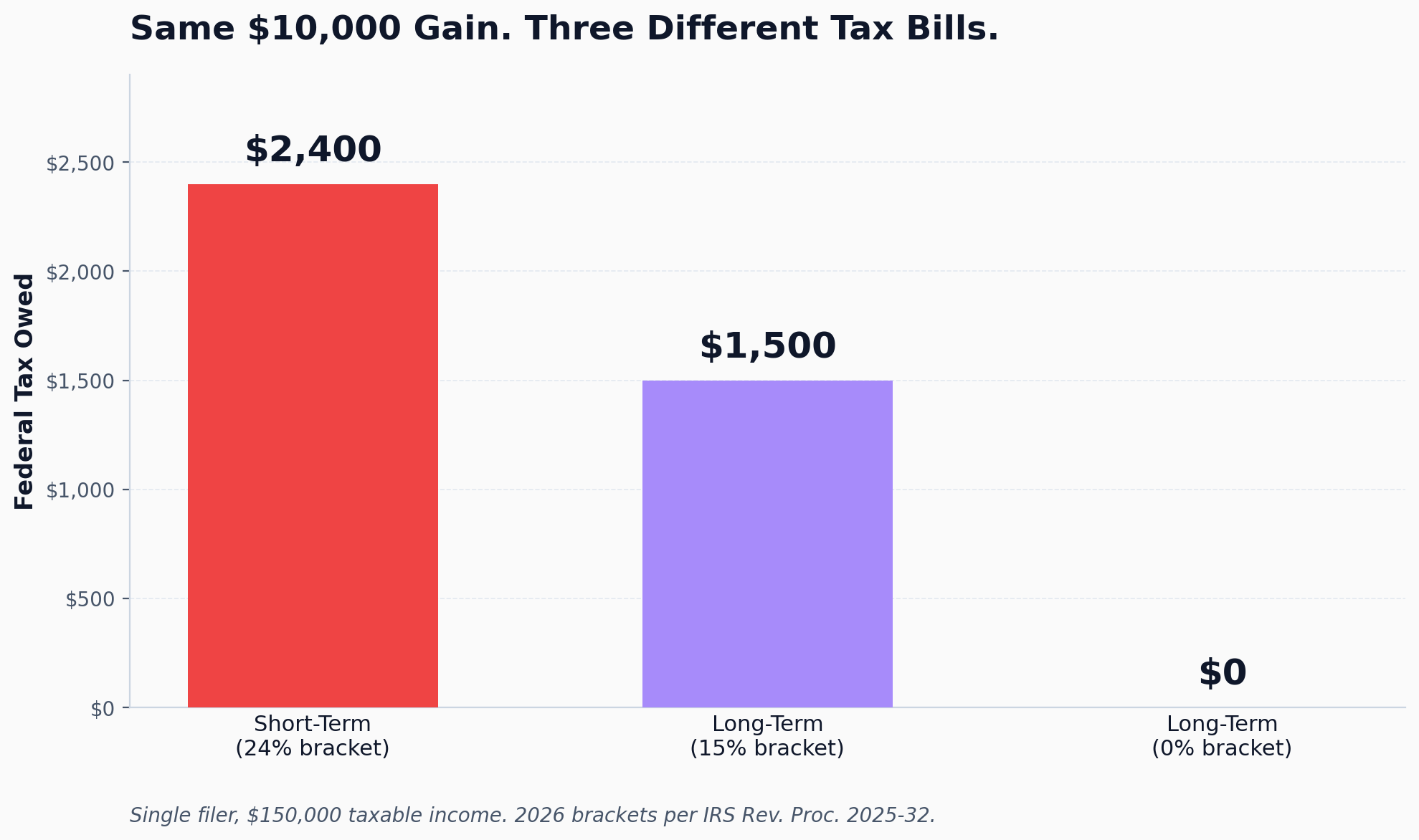

Two investors. Same stock. Same $10,000 profit. One sells on day 364 and owes roughly $2,400 in federal tax. The other sells on day 367 and owes $1,500. Three days, $900 difference — that is the holding-period cliff at the heart of capital gains tax, and it is the highest-ROI tax rule most retail investors never learn to use.

What Is Capital Gains Tax, Exactly?

Capital gains tax is the federal tax you owe on the profit when you sell an investment for more than you paid. Profit equals sale price minus cost basis (what you paid, including commissions). If you bought 100 shares at $40 and sold at $50, your gain is $1,000 — and that is the number the IRS taxes.

The trigger is the sale, not the appreciation. A stock that has tripled inside your brokerage account creates exactly zero tax liability until you push the sell button. The IRS does not tax paper gains. This is the single most important mental model for how the US treats investments: tax is owed on realized gains.

Almost everything you might invest in counts as a “capital asset” — stocks, ETFs, mutual funds, bonds, crypto, collectibles, real estate. Your primary home gets a partial exclusion: a single filer can exclude up to $250,000 of gain on the sale; married filing jointly excludes $500,000 (Section 121 of the tax code). Losses work as the inverse: sold below cost basis means a capital loss, which you can use to offset gains.

How Capital Gains Tax Actually Works

The mechanical flow is straightforward. You buy → you hold → you sell → your broker issues a Form 1099-B at year-end → you report the transactions on IRS Form 8949 and summarise on Schedule D → you owe tax based on how long you held the asset.

The IRS classifies every sale into one of two buckets based on the holding period:

- Short-term: held for one year or less. Taxed as ordinary income — the same rate as your salary, anywhere from 10% to 37% depending on your bracket.

- Long-term: held for more than one year. Taxed on a separate, lower schedule: 0%, 15%, or 20%.

The holding clock starts the day after you buy and runs through the day you sell. Buy on March 1 and sell exactly one year later on March 1, and the IRS still considers that short-term. You need to sell on March 2 (day 366 or later) to qualify for long-term treatment. The threshold is precise, and there is no partial credit.

Here is the worked example that anchors everything else in this guide. A single filer with $150,000 in taxable income realises a $10,000 gain. If short-term, that $10,000 stacks on top of ordinary income and gets taxed at the 24% marginal bracket: $2,400 owed. If long-term, that same $10,000 falls into the 15% capital gains bracket: $1,500 owed. Same profit, same investor, same federal government — but $900 difference because of the holding period.

If you build positions through dollar-cost averaging, each purchase starts its own holding-period clock. When you eventually sell, the broker reports each tax lot separately — so a single trade can produce both short-term and long-term gains in the same year. Most brokerages let you pick which lots to sell, which is itself a quiet tax lever.

Short-Term vs Long-Term Capital Gains Tax: The Rate Ladder

The long-term schedule has three rates — 0%, 15%, and 20% — with thresholds set by your taxable income and filing status. The IRS adjusts the cutoffs for inflation each year. Here are the 2026 brackets, straight from IRS Revenue Procedure 2025-32:

The 0% bracket is not theoretical. A retired couple with $90,000 of taxable income filing jointly can sell appreciated stock and owe zero federal capital gains tax on the realised gain, as long as the gain plus their other income stays under $98,900. This is one of the most underused tax-planning moves in the retail playbook — heavily used by wealthier filers who structure their realisations around the brackets.

One mechanic worth knowing: the IRS uses a stacking method. Your ordinary income fills the brackets first, and your long-term gains sit on top. So if you have $80,000 of ordinary income and realise a $50,000 long-term gain (filing jointly), the first $18,900 of that gain fits inside the 0% bracket — taking you up to the $98,900 ceiling — and the remaining $31,100 gets the 15% rate. Part 0%, part 15%, never a single flat number.

Two footnotes that catch some filers off guard. The Net Investment Income Tax (NIIT) is an extra 3.8% surtax on investment income above $200,000 single / $250,000 MFJ in modified adjusted gross income — and those thresholds have not been adjusted for inflation since the tax was created in 2013, so each year a few more filers cross into it. Second, this article covers federal tax only. State treatment varies widely: California and New York tax gains as ordinary income at state rates up to 13.3% and 10.9% respectively, while Florida, Texas, Washington, and a handful of others have no state income tax on gains at all.

Three Legal Ways to Lower the Bill

Capital gains tax is one of the few federal taxes where ordinary retail investors have real, legal optimisation levers. Three of them, in order of effort:

1. Hold for at least 366 days. The simplest lever and the one most retail investors leave on the table. If you are sitting on a gain at the 11-month mark, the default move is to wait the extra month unless you have a strong thesis for selling now. Going from a short-term gain in the 24% bracket to a long-term gain in the 15% bracket is a 37.5% reduction in the tax bill on that profit — and the trade-off is one month of price exposure.

2. Tax-loss harvesting. If you have realised gains during the year, you can sell losing positions to offset them. Capital losses first cancel out capital gains dollar-for-dollar; any remaining net loss can offset up to $3,000 of ordinary income, and the rest carries forward indefinitely to future tax years. The catch is the wash-sale rule: if you buy a “substantially identical” security within 30 days before or after the loss sale — a 61-day window in total — the IRS disallows the loss for that year. Most retail tax-loss harvesters swap into a similar-but-not-identical ETF (VOO → IVV → back to VOO after 31 days) to stay invested in the asset class without triggering the rule.

3. Hold appreciating assets inside tax-advantaged accounts. Inside a Roth IRA, traditional IRA, 401(k), or HSA, capital gains are not taxed when realised. The shielding mechanic differs by account type — gains in a Roth compound tax-free forever; gains in a traditional account compound tax-deferred and get taxed as ordinary income at withdrawal — but the principle is the same: no annual capital gains tax friction. For long-horizon investors, this is the highest-impact lever, which is why the Roth vs Traditional IRA decision matters even more than most retail investors realise.

Common Confusions About Capital Gains Tax

Do ETFs trigger capital gains when the fund rebalances? Rarely. ETFs use in-kind redemptions — the fund hands appreciated stock directly to an authorised participant in exchange for ETF shares, which under Section 852(b)(6) of the tax code does not trigger a taxable event. This is the structural reason index ETFs distribute almost no capital gains while equivalent mutual funds distribute meaningful ones each year. You still owe capital gains tax when you sell your ETF shares — but you do not owe tax on the fund’s internal rebalancing the way you do with a mutual fund.

Are dividends the same as capital gains? No, they are taxed separately. Qualified dividends — paid by US corporations (and qualifying foreign ones) and held through a 60-day window around the ex-dividend date — get the same 0% / 15% / 20% rates as long-term capital gains. Ordinary (non-qualified) dividends get taxed at your ordinary income rate. Your broker classifies each dividend on the 1099-DIV form.

What if I reinvest the proceeds into another stock? Does not matter. The sale itself is the taxable event. Reinvesting the cash does not defer the tax, and the new position starts a brand-new holding-period clock.

Do I owe capital gains tax on crypto? Yes. Per IRS Notice 2014-21, the IRS treats cryptocurrency as property, not currency. Every sell, swap, or use-as-payment is a taxable disposition. Sold ETH for cash, swapped ETH for SOL, paid for coffee with BTC — all three trigger a capital gains calculation. Holding-period rules apply the same way they do for stocks.

Does day trading count as long-term? Almost never — by definition, day-trade holding periods are seconds to days, all short-term. Heavy, full-time traders may qualify for “trader-in-securities” status with its own ruleset, but that is a separate path most retail investors will never need.

The Bottom Line

Capital gains tax is the tax the federal government applies to your realised investment profits, split into two buckets based on how long you held the asset. Sell at one year or less and the IRS taxes the gain as ordinary income at your marginal rate. Sell at more than one year and the gain falls into the long-term schedule at 0%, 15%, or 20%, with the bracket depending on your taxable income and filing status. The day-365 cliff is the single biggest controllable variable in retail investment tax planning.

If you remember three things from this guide: the holding-period cliff (366 days flips your gain into the lower schedule), the 0% bracket is real (and worth designing realisations around), and tax-advantaged accounts shield gains from the schedule entirely. For more on how the rate schedule fits with the rest of the tax code, the IRS publishes a complete reference in Topic 409 and the fuller treatment in Publication 550. For a meaningful tax situation, the highest-ROI move is talking to a CPA — every situation has wrinkles, and the rules above are the general framework, not a personalised plan.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!