- $7,500 in a Roth IRA is not the same money as $7,500 in a Traditional — one is pre-tax, the other is after-tax. Most guides quietly skip this distinction.

- Do the math properly and the growth rate plus time horizon cancel out of the breakeven equation. The only variable that matters is your current marginal rate vs your expected retirement rate.

- Under the 2025 One Big Beautiful Bill Act, the 10/12/22/24/32/35/37 tax brackets are now permanent. 'TCJA sunset' anxiety is no longer a reason to favor Roth — today's rates are the established baseline.

The Roth vs Traditional IRA decision usually gets handed off in one sentence: “If your future tax rate is higher, choose Roth; if lower, choose Traditional.” Then everyone moves on. The interesting work — what the breakeven tax rate actually is for your situation, why $7,500 in one isn’t equivalent to $7,500 in the other, and how a planner’s optimization model handles the uncertainty — never shows up.

This is the math we wish someone had shown us the first time.

The trap most guides set

Picture someone earning $90,000 in 2026. They contribute $7,500 to a Traditional IRA, pocket the $1,650 tax deduction at the 22% bracket, and feel pretty good about it. Twenty years later at 7% real returns, the account compounds to roughly $29,025. They withdraw at the same 22% rate — and net $22,640 after tax.

Now run the Roth version. Same person, same $90,000 income. They pay $1,650 in tax today, contribute $7,500 to a Roth IRA. Same 7% growth, same 20 years — $29,025, withdrawn tax-free. Net: $29,025.

Roth wins by $6,385. Case closed?

Not quite. The trap is that we just compared $7,500 in Traditional to $7,500 in Roth as if they were the same starting position. They weren’t. In the Traditional case, $7,500 was pre-tax money — the contribution was deducted from taxable income. In the Roth case, $7,500 was after-tax — the contributor effectively spent $7,500 + $1,650 = $9,150 of pre-tax earnings to get $7,500 into the account. The Traditional contributor still has the $1,650 tax savings sitting in their pocket. If they invest it too, the comparison shifts dramatically.

This is where most articles stop. We’re going to keep going.

How Roth vs Traditional IRA actually differs (the 2026 mechanics)

The two accounts share more than they differ: same menu of investments, same compounding mechanics, same penalty rules for non-qualified early withdrawals. What differs is when the IRS takes its cut.

The 2026 numbers, current as of this writing

Per the IRS’s November 2025 inflation-adjustment notice:

| 2026 IRA rule | Roth | Traditional |

|---|---|---|

| Contribution limit (under 50) | $7,500 | $7,500 |

| Contribution limit (age 50+, with $1,100 catch-up) | $8,600 | $8,600 |

| Tax treatment going in | After-tax (no deduction) | Pre-tax (deductible, subject to limits) |

| Tax treatment coming out | Tax-free (after 5-year rule + age 59½) | Taxed as ordinary income |

| Income phase-out, single | MAGI $153,000–$168,000 | $81,000–$91,000 (only if covered by workplace plan) |

| Income phase-out, married joint | MAGI $242,000–$252,000 | $129,000–$149,000 (only if covered by workplace plan) |

| RMDs (required minimum distributions) | None for original owner | Start at age 73 (per SECURE Act 2.0) |

Two practical implications of those phase-outs. First, if you’re a single filer earning over $168,000 (or married joint over $252,000), the front door to a Roth IRA is closed — you can’t contribute directly. The “backdoor Roth” mechanic still works (non-deductible Traditional contribution, immediate conversion), but it requires you not to already hold a sizable Traditional IRA balance, thanks to the pro-rata rule. Second, the Traditional deduction also phases out — but only if you’re already covered by a workplace plan like a 401(k). If neither you nor your spouse has a workplace plan, the Traditional deduction is unlimited regardless of income.

The actual breakeven math

Here’s the comparison that’s actually apples-to-apples. Pretend you have $10,000 of pre-tax money to put toward retirement. Same growth rate, same time horizon. Run both paths.

Traditional path. You drop the full $10,000 in (the deduction shields it from this year’s tax). It grows. At retirement you withdraw the entire balance and pay tax on it at your retirement bracket.

Roth path. You pay tax now on that $10,000 at your current bracket — say 22%. So $2,200 goes to the IRS and only $7,800 actually lands in the Roth account. It grows. At retirement you withdraw the entire balance tax-free.

Here’s the thing nobody points out: the same growth multiplier — whatever the market returns, however many years you let it compound — applies to BOTH balances identically. Whether stocks return 5% or 10%, whether the horizon is 10 years or 40, the multiplier scales both numbers the same way.

Once the matching growth gets divided out of both sides, all that’s left is the tax-rate comparison:

| Traditional | Roth | |

|---|---|---|

| What goes in | $10,000 pre-tax | $7,800 (after paying 22% today) |

| How it grows | same multiplier | same multiplier |

| Taxed at withdrawal | retirement bracket | tax-free |

If your retirement bracket equals your current bracket (both 22%), Traditional pays 22% on the larger balance, Roth already paid 22% upfront on the smaller balance — they produce exactly the same after-tax dollars. If your retirement bracket is lower (say 12%), Traditional wins: you paid 12% later on the big balance instead of 22% today on the contribution. If retirement is higher, Roth wins.

That’s the entire decision. Not the growth rate. Not the time horizon. Not “tax-free sounds nicer.” Your current marginal bracket vs your expected retirement bracket. Full stop.

Most guides bury this under spreadsheets and “depends on your situation” hedging. The cleanness of the result is itself the answer: you don’t need a calculator. You need an honest estimate of where your bracket lands now and where it’s likely to land in retirement.

Where the math breaks down

The clean breakeven above assumes you can contribute the full annual limit either way. If you can’t — and most savers can’t — the wrinkles start to matter:

- The “what about the tax savings?” question. If you contribute $7,500 to Traditional and have $1,650 left over from the tax deduction, that $1,650 has to go somewhere. If you invest it in a taxable account, it drags from annual dividends and capital-gains tax. If you spend it (most people do), the original breakeven math gives Roth the edge by default — Roth force-saved you that tax bill.

- State taxes. A high earner in California (13.3% top state rate) contributing to Traditional today might retire in Florida (0% state) — adding roughly 13 percentage points to the favor-Traditional side. Going the other way is rarer but possible.

- Roth has no RMDs. A Traditional IRA forces required distributions starting at age 73. A Roth doesn’t, for the original owner. That extra decade or two of tax-free compounding is a real advantage if you don’t need the money at 73.

- Bracket politics. Future tax rates aren’t permanent — Congress can change brackets in any future year. But as of July 4, 2025, the One Big Beautiful Bill Act made the 10/12/22/24/32/35/37 bracket structure permanent. There’s no scheduled 2026 sunset, no automatic reversion to pre-2017 brackets. Today’s rates are the established baseline. Net implication: locking in current rates via Roth carries less “vs. an unknown future regime” anxiety than it did a year ago.

- Roth conversion ladders. The arbitrage most people miss is converting Traditional to Roth during low-income windows — early retirement, sabbatical, between jobs. Each conversion bumps you into a bracket; you stop just below the next one. Over a few years you migrate the balance with minimal tax drag.

How a planner’s optimization model actually solves it

“Compare current to retirement rate” is the right answer at the napkin level. But the real models that financial planners and robo-advisors run go further — and the way they go further reveals which decisions matter most.

Software like Income Lab and RightCapital, plus the institutional engines behind robo-advisors, run something like this:

- Monte Carlo across tax-bracket paths. Run 1,000+ futures: brackets stay as-is, brackets rise (debt and deficit pressure), brackets fall (unlikely but modeled). Each path produces a different optimal split. The model returns a weighted recommendation, not a deterministic one.

- Asset-location optimization. Different assets are taxed differently — bond interest at ordinary income, qualified dividends at preferential rates, growth stocks deferred until sale, municipal bond interest federally tax-free. Vanguard’s asset-location research shows the typical optimal placement: bonds in Traditional IRA first, equities in Roth, muni bonds and tax-efficient index funds in taxable. The reasoning: bonds throw off ordinary-income interest that’s taxed annually in taxable accounts, so sheltering them inside Traditional defers that. High-growth equities get the most upside, so put them where the upside compounds tax-free — Roth.

- Roth conversion ladders. Identify the years where your taxable income is naturally low (between retirement and Social Security claim, sabbatical, between jobs). Run conversions that max out a target bracket — e.g. convert just enough to fill the 12% bracket without bumping into 22%. Over five to ten years a six-figure Traditional balance can migrate to Roth at low marginal cost.

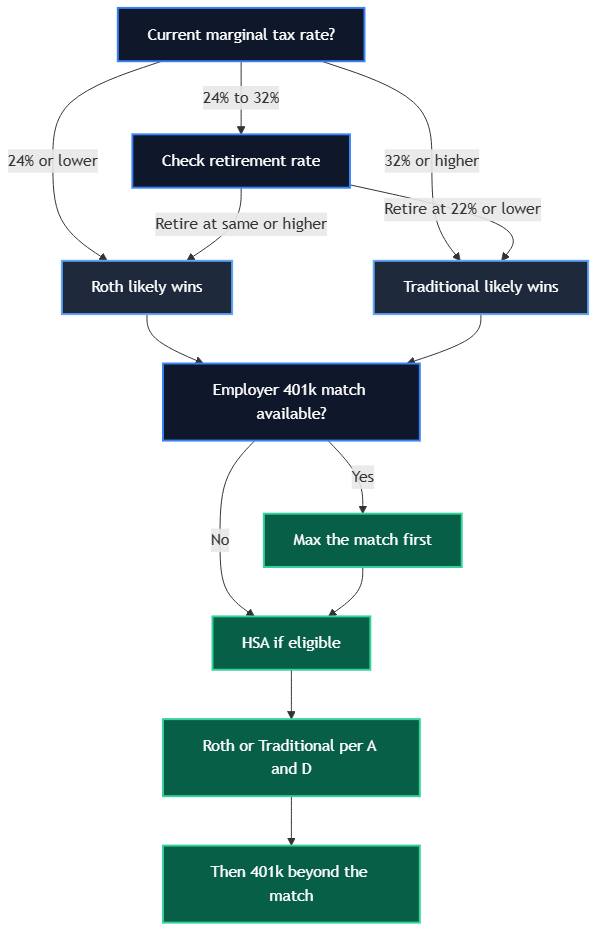

- The contribution hierarchy that falls out of the math. Almost every model converges on the same priority order: (a) 401(k) up to the employer match — free money beats any tax arbitrage; (b) HSA if eligible — the only triple tax-advantaged account; (c) Roth IRA up to limit IF your current marginal rate is 24% or lower; (d) Traditional 401(k) or IRA for everything beyond. Robo-advisors default to this hierarchy not because it’s hardcoded as a rule, but because it’s what their optimization engine outputs for the typical saver who lands in the 12–24% bracket range.

The honest planner-grade answer to “Roth or Traditional?” is almost never one or the other. It’s: show us your current bracket, your projected retirement income, your state-tax path, and your employer match — and even then, the answer is usually both, in a specific ratio.

Where beginners go wrong

- Comparing $7,500 in Traditional to $7,500 in Roth as if they’re equivalent. They aren’t — one is pre-tax, one is after-tax. The fair comparison is per pre-tax dollar.

- Taking the Traditional deduction and spending it. Pocket the tax savings instead of investing them, and the structural advantage that made Traditional competitive in the math disappears. Roth doesn’t have this trap because the tax bill comes off the top by design.

- Maxing Roth in a high-earning year when your marginal rate is 32% or higher. If you’ll retire in the 22% bracket, paying 32% today to avoid 22% later is paying retail price on the wrong shelf. For high-bracket earners, Traditional usually wins on pure breakeven — even before counting state-tax mobility.

- Ignoring the 5-year rule on Roth. Earnings withdrawn before age 59½ and before 5 years have elapsed since the first Roth contribution get taxed and penalized (10%). Contributions themselves can come out any time tax- and penalty-free — but earnings can’t. A common mistake: someone starts a Roth at age 56 thinking they can tap it at 59½, then discovers the 5-year clock means earnings stay locked until age 61.

- Missing the backdoor Roth. If your MAGI is above the Roth direct-contribution phase-out, you can still contribute via a non-deductible Traditional contribution followed by an immediate conversion. The pro-rata rule applies: if you already hold pre-tax Traditional IRA dollars elsewhere, conversions are taxed proportionally. Best done when your Traditional IRA balance is zero or near-zero.

- Treating “tax-free” as automatically better. “Roth is tax-free” sounds great and feels right. But the math doesn’t care how it sounds — it cares about the marginal-rate comparison. Many people would be objectively better off in Traditional and choose Roth based on the marketing word “free.” Tools like Fidelity’s Roth conversion calculator back-check the intuition with numbers.

Going deeper

Once the account-type question is settled, the next decision is what to actually hold inside it. A few starting points:

- ETF expense ratios — the same arithmetic that makes tax drag matter applies to fund fees. A 0.30% fee compounds over 30 years to a remarkably large number.

- VOO vs VTI — practical follow-up if you’re deciding what core holding to use inside your IRA.

- Dividend ETFs vs growth ETFs — asset-location relevance: high-yield dividend ETFs benefit disproportionately from Roth’s tax-free compounding, since dividends would otherwise be taxed annually in taxable accounts.

The right way to read the Roth vs Traditional IRA question isn’t “which one.” It’s: what does your honest tax-rate trajectory look like, and what’s the contribution mix that maximizes after-tax retirement dollars across that uncertainty? The math is cleaner than most guides make it. The reasoning around it is where the real work happens.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!