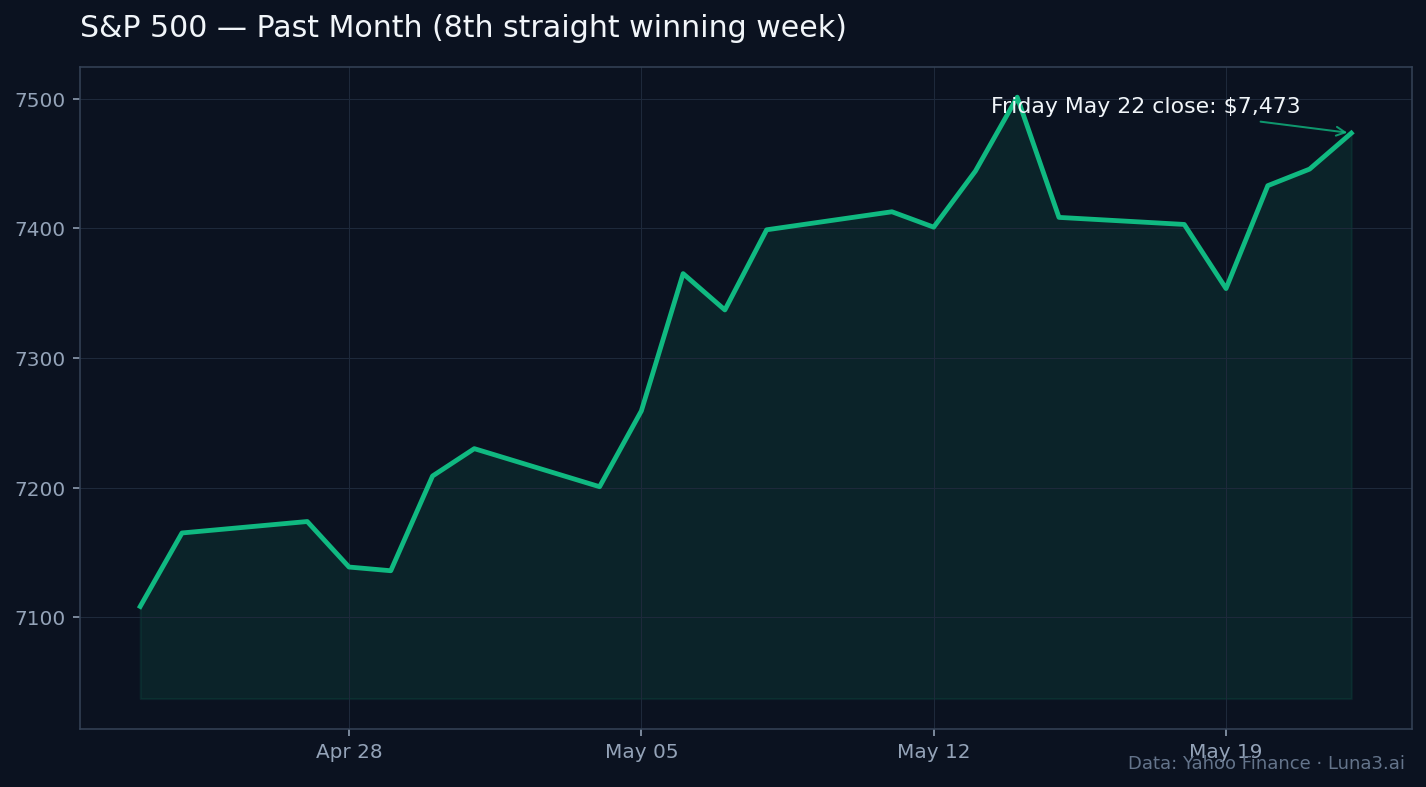

- S&P 500 closed Friday at 7,473.47 — its 8th straight winning week, the longest streak since 2023

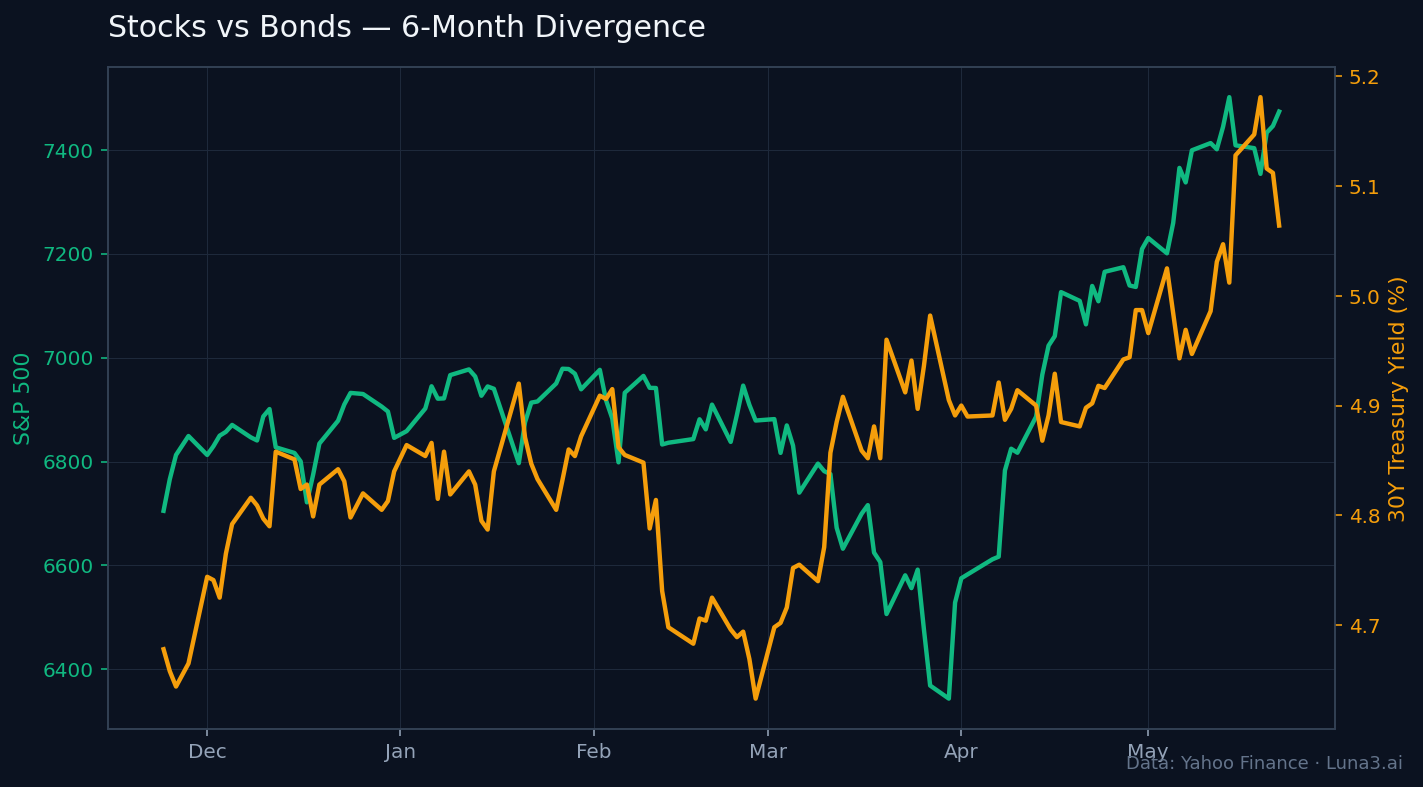

- The 30-year Treasury yield touched 5.197% on May 19 — its highest reading since July 2007, on Iran-conflict oil prices + Fed Gov Waller's hawkish framing

- Kevin Warsh was sworn in Friday as Fed chair; first FOMC under his watch is June, with April PCE landing Thursday May 28

Records on the scoreboard, a 19-year yield high under the surface, and a new Fed chair walking into an FOMC meeting in twenty-four days — this week’s Market Pulse Digest is a story about two markets telling two different stories.

What moved

The S&P 500 closed Friday at 7,473.47, up 0.37% on the session and notching its eighth consecutive weekly win — the longest streak since 2023. The Dow Jones added 294 points to a fresh record close of 50,579.70. The Nasdaq lagged at 26,343.97, up 0.19%. With 94% of S&P 500 companies having reported Q1, blended year-over-year EPS growth landed at 28.4% per FactSet — well above the 13.2% the Street expected entering the season. AI and tech earnings carried the index back toward records after Monday’s selloff.

Bond markets told a sharply different story. The 30-year Treasury yield touched 5.197% intraday on May 19 — its highest reading since July 2007. The 10-year added four basis points to 4.667%. Yields rose on inflation reacceleration fears tied to Iran-conflict-driven oil prices, and on Fed Governor Christopher Waller’s comment that the central bank’s next move “is just as likely to be a hike as a cut.” The fiscal stress that Moody’s flagged a year ago when it pulled the US off Aaa is now visible in the long end of the curve — not as headline news, just as price.

A third thread: progress on turning the fragile Iran-US ceasefire into a lasting peace deal helped fuel Friday’s relief rally, pushing the Dow to its new record close.

What didn’t move

Two things stayed remarkably quiet.

First, rate-cut expectations. Kevin Warsh was sworn in Friday at the White House — the first Fed chair to take the oath in the East Room since Alan Greenspan in 1987. He pledged a “reform-oriented Fed” and his first FOMC meeting is in June. But the curve isn’t pricing a pivot. Warsh walks in with surging inflation, historic-low consumer sentiment, and a president demanding rate cuts. Waller’s hawkish framing this week effectively turned June into the new chair’s first independence test rather than a coronation.

Second, equity volatility. The VIX sat sleepy all week even as the long bond posted a 19-year yield high. Two markets reading two narratives: equities anchored to “AI earnings season, 28% Y/Y EPS growth, capex cycle intact”; bonds anchored to “Iran oil, inflation re-accelerating, no Fed help coming.” Both stories can’t be right indefinitely.

Charts of the week — Market Pulse Digest

The long bond is doing what equity desks aren’t — pricing a regime where inflation drifts higher and the Fed can’t (or won’t) lean against it. 5.197% takes us back to a world where Bear Stearns was still a brokerage.

Eight straight weekly wins. The May 19 wobble (-0.67%) was the deepest intraweek dent in the run — and got bought back inside three sessions. Strong earnings are doing real work here; this isn’t a sentiment rally.

The divergence is the chart that matters. Either bonds are wrong and yields fade as Iran calms, or stocks are wrong and the rate ceiling eventually clips the AI multiple. Historically, when the long bond posts a 19-year yield high while equities print fresh records, one of the two prints retraces. We don’t pretend to know which.

On the calendar — week of May 26

Memorial Day Monday (May 25) shuts US markets; trading resumes Tuesday. A four-session week packed with the load-bearing macro print of the month.

- Tue May 26 — May consumer confidence; AutoZone + Zscaler earnings. Early read on whether the sentiment trough has stopped getting worse.

- Wed May 27 (after close) — Marvell (MRVL), Salesforce (CRM), Snowflake (SNOW), HPQ, Synopsys, Autodesk earnings. The AI-hardware and enterprise-AI demand reads all land on the same tape. MRVL consensus runs around $2.4B in revenue — the marginal read on custom-silicon ramp vs the broader memory-supply-chain pricing cycle.

- Thu May 28 — Dell (DELL), Costco, Best Buy, MongoDB earnings; Q1 GDP second estimate; April PCE inflation (the week’s anchor). Core PCE consensus runs 3.3% Y/Y vs March’s 3.2%. A hot print turns Waller’s “next move could be a hike” from rhetoric into a market-priced probability.

Our read: April PCE is the number to watch. Everything else is a sideshow. If PCE prints in line or hotter, the bond-vs-stock divergence widens; if it cools, the June FOMC narrative pivots and yields can fade fast. The same setup also matters for AI-themed ETF flows, which have been the marginal bid under the AI cohort.

One read for the weekend

CNN Business — “Kevin Warsh sworn in as Fed chair at pivotal moment for US economy”. The institutional context for what June will actually mean.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!