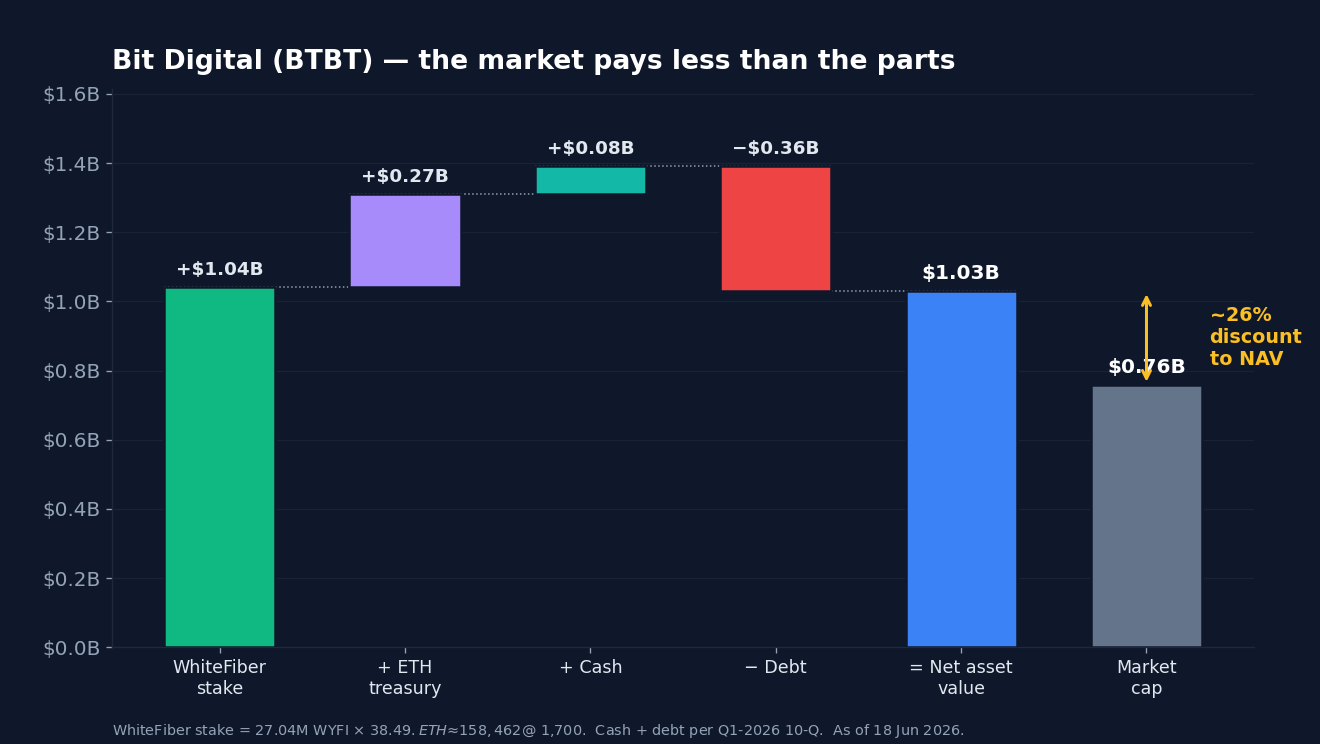

- At $2.17 (June 18, 2026), the market values all of Bit Digital (NASDAQ: BTBT) at about $758 million — yet its ~70% stake in separately listed WhiteFiber (NASDAQ: WYFI) is worth roughly $1.04 billion on its own.

- Add a ~158,000-ETH treasury and cash, subtract the debt, and net asset value lands near $1.03 billion — so BTBT trades at roughly a 26% discount to the parts, and below its WhiteFiber stake alone.

- The discount is real, but so is the reason for it: Bit Digital has pledged not to sell any WhiteFiber shares in 2026, the structure is tax-inefficient to unwind, and the asset propping up the value just tripled on a short squeeze.

Start a BTBT stock analysis with one number and the rest of the page rearranges itself: $2.17. That is where Bit Digital closed on June 18, 2026 — a price that values the entire company at about $758 million. The complication is that Bit Digital owns roughly 70% of WhiteFiber, a separately listed AI-infrastructure company, and at WhiteFiber’s own closing price that stake alone is worth about $1.04 billion. The parent is worth less than the slice of itself that already trades on the same exchange.

The stock — ticker BTBT — last printed $2.17 going into publication on June 20, 2026, down roughly 11% over the trailing twelve months even after a 25% bounce in the past month. That bounce is the tell, and it is the reason this is not a simple “deep value” story.

The thesis

Bit Digital is no longer an operating company in the usual sense. It is a holding structure whose value is dominated by one volatile, listed stake — WhiteFiber — plus an Ethereum treasury and cash. On the parts, it looks cheap: the WhiteFiber stake alone exceeds the whole market cap, and that is before counting the crypto. But the gap between price and parts is not an oversight the market will rush to close. It is the price of a controlled-company structure, a self-imposed lock on the one asset that matters, and a balance sheet that swung to roughly $334 million of convertible debt in a single quarter. The interesting question in this BTBT stock analysis is not whether the discount exists — it plainly does — but whether anything will ever force it to close.

How Bit Digital stopped being a miner

Two pivots, eighteen months, same company. Bit Digital spent years as one of the first Nasdaq-listed bitcoin miners. On June 25, 2025 it announced it was exiting mining to become a “pure-play” Ethereum staking and treasury business, converting its bitcoin into ETH and redirecting capital into the chain it now treats as core infrastructure, as CoinDesk reported. By the first quarter of 2026 management described mining as “no longer a strategic growth priority” and kept winding it down — mining revenue fell to $3.7 million, down about a third sequentially.

The second pivot is the one that matters more. In August 2025 Bit Digital carved out its high-performance-computing arm as WhiteFiber and floated about 20% of it on Nasdaq at $17.00 a share. Bit Digital kept the rest. That subsidiary — an NVIDIA-partner GPU cloud bolted onto a data-center build-out — is now the center of gravity. This is the same arc we traced in our analysis of CleanSpark’s late-mover AI pivot and in the broader thesis that bitcoin miners are quietly becoming AI infrastructure. Bit Digital just took it one step further by giving the AI business its own ticker.

The sum-of-the-parts math

Here is the arithmetic that makes the page rearrange itself. Bit Digital owns 27,043,750 WhiteFiber shares — the block it received when it contributed the HPC business before the IPO — which works out to roughly 70% of WhiteFiber’s 38.6 million shares outstanding. At WhiteFiber’s June 18 close of $38.49, that stake is worth about $1.04 billion. Bit Digital’s entire market capitalization that day was about $758 million.

| Metric (Jun 18, 2026) | Bit Digital (BTBT) | WhiteFiber (WYFI) |

|---|---|---|

| Closing price | $2.17 | $38.49 |

| Market cap | ~$758M | ~$1.49B |

| Shares outstanding | ~349M | ~38.6M |

| TTM revenue | ~$115M | ~$83M |

| The business | ETH treasury + 70% of WhiteFiber | NVIDIA-partner GPU cloud + data centers |

| Cross-holding | Owns ~70% of WhiteFiber | ~70% owned by Bit Digital |

Stack the rest on top. Bit Digital held roughly 158,462 ETH after a $20 million purchase in May — worth around $270 million with ether in the low $1,700s — making it the fourth-largest public-company holder of the asset. Add about $80 million of cash from the first-quarter balance sheet. Subtract roughly $360 million of total debt, most of it convertible notes. Net asset value lands near $1.03 billion against a $758 million market cap — a discount of about 26%, with the WhiteFiber stake alone already worth more than the whole company.

A discount to net asset value is normal for holding companies — markets routinely shave 10% to 30% off conglomerates because investors cannot easily get at the trapped value. What is unusual here is the magnitude relative to liquidity: this is not a sprawling private portfolio that is hard to mark. It is one number times a quoted share price. The market can see exactly what the stake is worth and is still declining to pay for it.

Why WhiteFiber is the whole story now

Strip away the crypto branding and Bit Digital’s operating business is, functionally, WhiteFiber. The subsidiary runs an NVIDIA-preferred GPU cloud — among the early providers of H200, B200 and GB200 systems — on top of Tier-3 data centers in Montreal, Iceland and Madison, North Carolina, where the NC-1 campus is building toward 99 megawatts. Its anchor contract is a 10-year colocation deal with Nscale, announced in December 2025, worth roughly $865 million in total contract value, and total contracted colocation obligations sit near $921 million. WhiteFiber’s full-year 2025 revenue was $79.2 million, up from $47.6 million; first-quarter 2026 revenue grew 31% year over year to $21.9 million.

That backlog is what the market is actually repricing, and it sits inside the larger AI capex wave we mapped in our look at hyperscaler spending. WhiteFiber’s stock did most of the work this year — and Bit Digital, holding 70% of it, came along for the ride.

What this BTBT stock analysis can’t promise you

The bear case is not that the math is wrong. It is that every reason the discount exists is also a reason it might persist — or widen.

The discount has no near-term release valve. The cleanest way to close a holding-company discount is to sell the asset and hand back the cash. Bit Digital has done the opposite: after its IPO lock-up expired on February 2, 2026, it publicly reaffirmed it will not sell any WhiteFiber shares during 2026, in a January statement. WhiteFiber is also a Nasdaq “controlled company,” so minority holders have limited say, and any eventual sale of a low-basis carve-out would trigger a large corporate tax bill. The market is pricing that friction, not ignoring it.

The floor asset is frothy. WhiteFiber rose about 154% in three months and roughly 57% in a single week into June 18, a move analysts attribute to record short interest against a tiny ~11-million-share float and a speculative call-option surge — not to earnings. WhiteFiber closed at $38.49, above its consensus mean target of about $35; Barclays initiated at Equal-Weight with a $27 target, while B. Riley sits at $44. If WhiteFiber mean-reverts, Bit Digital’s “net asset value” floor reverts with it.

The crypto leg is underwater, and it did not drive the pop. A common misread is that BTBT rose because Ethereum rose. It didn’t — ether fell from roughly $2,400 in early May toward $1,650 by mid-June while BTBT climbed, because WhiteFiber climbed. The treasury’s average cost is around $3,045 per ETH, so at current prices it sits well underwater; the $121.1 million non-cash mark-to-market hit on that treasury is most of why Bit Digital reported a $146.7 million first-quarter net loss on revenue of $27.9 million.

Dilution and leverage are real. Share count rose roughly 68% over the past year to about 349 million, funded by an at-the-market program that is still live, and convertible debt jumped to about $334 million against only ~$80 million of cash. Bit Digital has even begun borrowing against its ETH to on-lend roughly $100 million to WhiteFiber’s data-center build-out — earning a spread, but layering crypto-collateral risk on top of the equity risk.

WhiteFiber itself is sub-scale with concentration risk. Its largest customer was about 71% of 2025 revenue, and the field it competes in is brutal: CoreWeave alone reported quarterly revenue above $2 billion against WhiteFiber’s $22 million. The asset carrying the whole thesis is early, cash-burning and exposed.

Catalysts to watch

A few things would move the gap in either direction. WhiteFiber’s NC-1 ramp with Nscale is scheduled to start contributing revenue from the second quarter of 2026 — execution there is what justifies the run, or doesn’t. Any signal on WhiteFiber monetization after the 2026 no-sell window would be the clearest discount-closing event. Management has teased “a material update” on its Ethereum treasury strategy; the direction of ether itself sets the size of the crypto leg. And Bit Digital’s annual meeting is set for July 29. Watch the gap between WhiteFiber’s market value and Bit Digital’s — if the parent keeps lagging while the stake holds, the market is telling you it does not believe the value is recoverable.

The bottom line

Bit Digital is the rare case where the headline math and the cautionary tale point in the same direction. The discount is genuine and quantifiable: a roughly $758 million company sitting on a ~$1.04 billion listed stake, a crypto treasury and cash. It is also genuine and structural — a controlled subsidiary the parent has promised not to touch this year, a tax wall around any future sale, heavy dilution, and a “floor” asset that just tripled on a squeeze. Wall Street’s five analysts all rate BTBT a buy with a mean target near $4.60, more than double the current price, and they are pricing the parts. The market is pricing the trap. This BTBT stock analysis can map the gap precisely; what it cannot tell you is which of those two readings the next twelve months will reward.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings (like BTBT) and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!