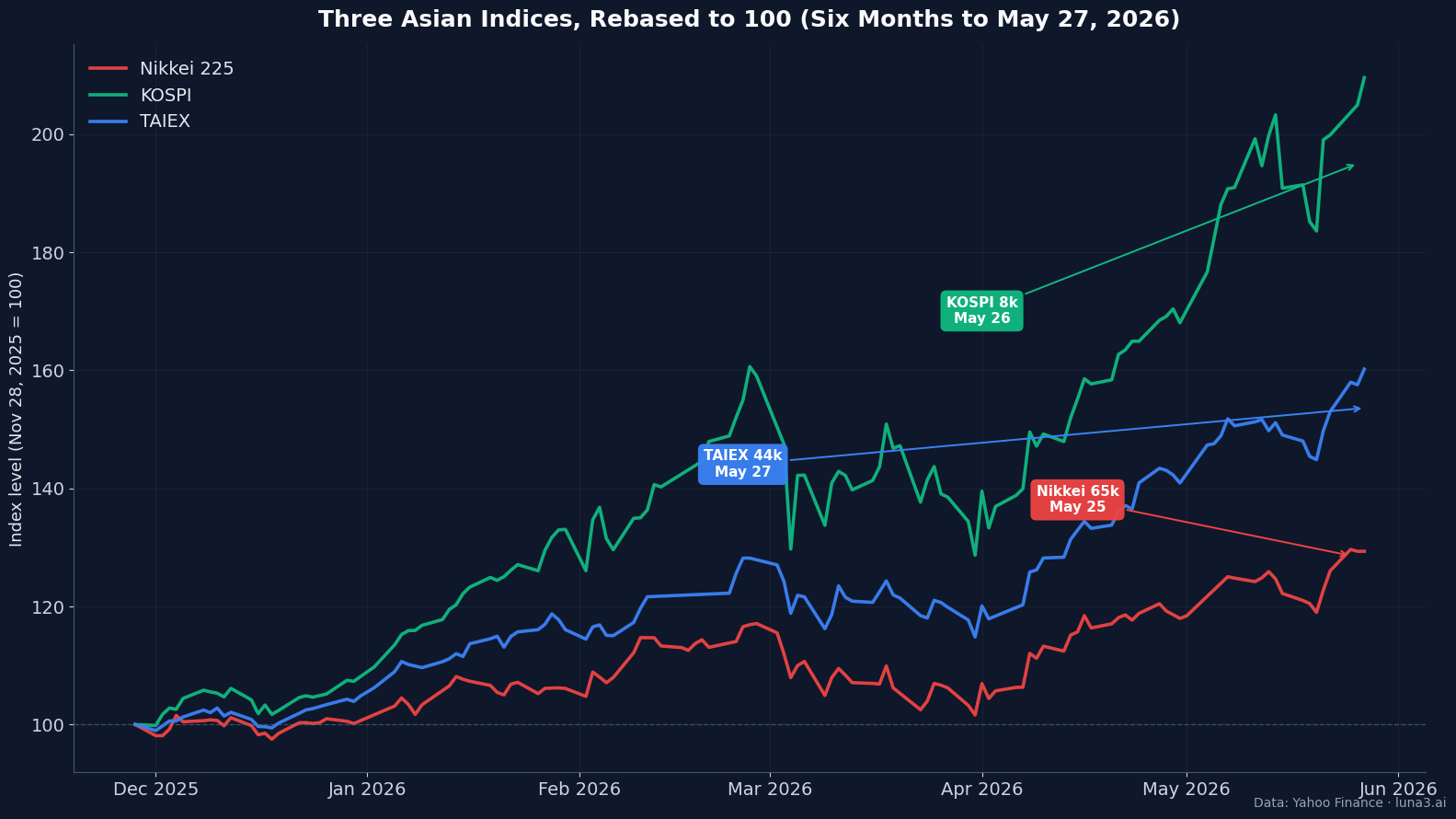

- Three Asian benchmarks set all-time records inside one week — Nikkei 65,158 on May 25, KOSPI 8,047 on May 26, TAIEX 44,256 by May 27 close.

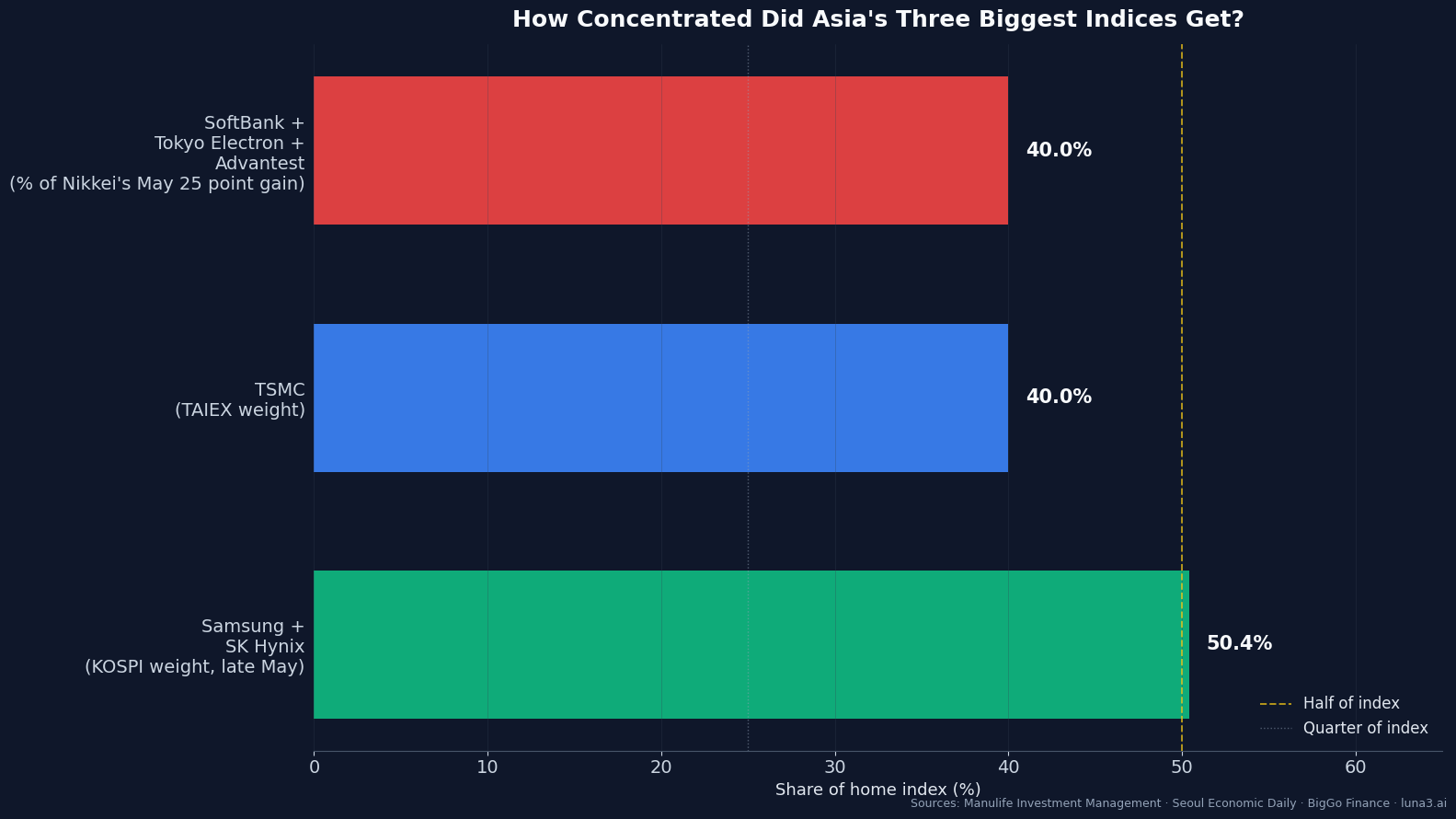

- The breadth is narrower than the index moves suggest. Samsung and SK Hynix now account for roughly half of KOSPI market cap. TSMC carries more than 40% of the TAIEX. Three Japanese AI names drove ~40% of the Nikkei’s record-setting May 25 point gain.

- If you own a passive Asia or emerging-markets ETF, your exposure to the AI infrastructure cycle is higher than the fund factsheet suggests — and historically, single-name-dominated benchmarks have amplified drawdowns when the lead name’s catalyst breaks.

The asia ai concentration story behind Asia’s late-May rally is narrower than the headlines suggest. Three of Asia’s biggest equity indices printed all-time closing highs inside one trading week. Japan’s Nikkei 225 closed at 65,158.19 on Monday, May 25 — the first time the 75-year-old benchmark has finished above 65,000. South Korea’s KOSPI followed on Tuesday with 8,047.51, its first close above 8,000. Taiwan’s TAIEX extended its own record run to 44,256.80 by Wednesday’s close. A very small group of stocks did most of the work.

For context: KOSPI is up roughly 95% year-to-date through May 27, on yfinance close-to-close basis. TAIEX is up about 54%. The Nikkei is up around 29%. KOSPI is the world’s best-performing major equity benchmark in 2026. None of the U.S. indices come close. The S&P 500 and Nasdaq 100 are mid-single-digit territory. What you’re looking at, in raw return space, is an Asian outperformance episode without recent parallel. What you’re looking at in composition space is the second-order story — and it’s the one that matters for anyone holding a passive Asia or broad emerging-markets fund.

How Asia AI Concentration Became Structural

Five names are doing most of the regional lifting. Three are Korean and Taiwanese chip designers and foundries. Two are Japanese semiconductor-equipment and AI-platform names. They are not the only stocks rising. They are the stocks that mathematically explain the index moves.

TSMC (2330.TW / TSM ADR). Taiwan Semiconductor changed hands at $422.73 (ADR) going into publication on May 28, and is up about 50% in 2026 on the Taipei line. According to Manulife Investment Management and CNBC reporting, TSMC now accounts for more than 40% of the TAIEX. Capacity is the load-bearing variable. Per DataCenterDynamics, TSMC guided FY26 capex to $52–56 billion in January, with management indicating it would spend near the high end. Roughly 70–80% of that is going into 2nm and 3nm advanced nodes; another 10–20% into CoWoS and SoIC advanced packaging, where capacity is targeted to reach 150,000 wafers per month by year-end — a fourfold expansion from late 2024. The foundry is the choke point. Nvidia, AMD, Apple, Broadcom, custom-silicon hyperscalers — they all queue.

Samsung Electronics (005930.KS). Up roughly 157% year-to-date through May 27, on yfinance close-to-close numbers (KRW 119,500 to KRW 307,000). Samsung makes HBM3E and is in the qualification cycle for HBM4, the next-generation memory stack that NVDA’s post-B100 architecture needs. Foundry remains a structural drag versus TSMC, but the memory side has carried the whole story this year.

SK Hynix (000660.KS). Up about 250% year-to-date on the same close-to-close basis. SK Hynix joined the trillion-dollar market-cap club on May 26 alongside Samsung and Micron, per U.S. News & World Report. SK Hynix is the primary HBM supplier to Nvidia’s H100 and B100, and the company has been the cleanest pure-play on the memory cycle this year. Per Manulife Investment Management figures cited by CNBC, Samsung and SK Hynix together made up 42.2% of the KOSPI in early May. By late May, per Seoul Economic Daily, the combined share had climbed to about 50% — in other words, two names now move half the index.

SoftBank Group (9984.T). Trading near ¥7,125 on the Tokyo line going into May 28, up about 59% in 2026. SoftBank had two of its biggest single-day moves of the year on May 21 (+20%) and May 22 (+12%) following Nvidia’s Q1 FY27 print, which delivered $81.6 billion in revenue, up 85% year-over-year, plus an $80 billion buyback authorization. The two-day move added over $61 billion in market value. SoftBank’s rally tracks Arm Holdings (in which it holds the majority stake) and re-rates its $30+ billion OpenAI position whenever Nvidia’s numbers extend the AI capex cycle.

Tokyo Electron (8035.T) and Advantest (6857.T). Tokyo Electron makes the etch and deposition equipment that builds advanced nodes; Advantest makes the testers that validate every AI accelerator coming off TSMC and Samsung lines. Together with SoftBank, these three names accounted for roughly 40% of the Nikkei’s point gain on May 25 — the day the index first crossed 65,000. Three stocks. Forty percent of one day’s headline number. The other 222 names in the Nikkei moved the remaining 60%.

What An Asia ETF Actually Owns Now

Index construction is a passive process. Cap-weighted benchmarks track market value, and the funds that replicate them — iShares MSCI Taiwan ETF (EWT), iShares MSCI South Korea ETF (EWY), iShares MSCI Japan ETF (EWJ), Vanguard FTSE Emerging Markets ETF (VWO), Vanguard FTSE Pacific ETF (VPL) — don’t adjudicate concentration. They just hold what’s in the index. When five names rip, the funds tilt automatically.

The mechanical effects are now visible in the holdings sheets. EWT’s top position, TSMC, sits at about 21% of the fund — the maximum allowed under the index methodology. EWY’s top two positions — Samsung and SK Hynix — collectively exceed half the fund (about 53% as of late May), tracking the combined KOSPI share. Even in VWO, a broad emerging-markets fund spanning 27 countries, TSMC and Samsung have grown into a combined share roughly double what they carried before the current AI capex cycle began. The reader who bought a “diversified emerging markets” position three years ago for portfolio diversification reasons now owns, in part, a leveraged bet on Nvidia’s order book.

None of this is a flaw in passive design. The funds are doing what the prospectus promises. The point is that the label on the fund — “Asia-Pacific,” “emerging markets,” “Korea,” “Taiwan” — no longer describes the underlying exposure accurately. The exposure is increasingly to the AI infrastructure cycle. The country wrapper is incidental.

The Saudi Aramco And Novo Nordisk Parallel

Manulife Investment Management, in the CNBC piece cited above, drew the parallel that probably travels furthest. Single-name-dominated benchmarks are not unprecedented. Saudi Arabia’s Tadawul is heavily weighted toward Saudi Aramco. Denmark’s OMX Copenhagen has been heavily weighted toward Novo Nordisk during the GLP-1 cycle. In both cases, when the dominant name’s catalyst stalled — a swing in oil prices for Aramco, a Wegovy revenue revision for Novo — the entire national benchmark moved with it. Diversification within the index did not bail out the index-level return.

Korea and Taiwan now sit in similar structural company. If Samsung guides HBM4 contract pricing lower next quarter, or if TSMC monthly revenue rolls over from the current pace, the index-level math gets ugly fast — because a 10% move in TSMC is a 4-percentage-point move in the TAIEX before anything else trades. Japan is one step removed from this concentration because the Nikkei is more diversified across exporters, but the marginal move — the alpha generation — has narrowed to a similar handful of AI-linked names. The structural exposure is the same shape; the magnitude is just lower.

What Could Break The Asia AI Trade

The bear case isn’t a single event. It’s a list of independent triggers, any one of which would propagate through the same five names and therefore through the indices.

Nvidia earnings cycle. The Q1 FY27 print on May 20 was the catalyst that triggered the SoftBank surge and reinforced the Asia AI bid. The next print in late August carries higher base-rate risk — expectations have been pulled forward, the buyback authorization is now in the price, and the China H20 export framework remains unsettled per the Trump-Xi summit deliverables. A miss or a soft data-center segment guide would land hardest in Asia, because Asia’s top names are leveraged to Nvidia’s order pattern more directly than U.S. semis are.

Chinese semi catching up. SMIC, Cambricon Technologies, and the broader mainland Chinese semiconductor cohort have been rallying alongside — Cambricon was up about 9% on May 25 alone, with SMIC and other semi names posting multi-percent single-day gains during the same week. Beijing’s industrial policy explicitly targets domestic substitution for advanced AI silicon. The Taiwan and Korea concentration trade does not require these efforts to succeed, but it does require them to remain at least one generation behind. If the gap narrows faster than expected, the foundry premium compresses.

Energy and shipping disruption. Korea and Taiwan are large energy importers. A Strait of Hormuz disruption — the variable that bid oil sharply through mid-May before Iran negotiations stabilized prices — raises input costs, compresses operating margins, and tightens shipping for finished semis to U.S. and European customers. The exporter model assumes cheap energy and open Pacific shipping lanes. Either assumption breaking is a headwind that doesn’t require anything to be wrong with Nvidia’s order book.

Currency. A material yen strengthening reverses the Japanese exporter tailwind that has helped SoftBank, Tokyo Electron, and Advantest convert dollar revenue to yen earnings. The Bank of Japan is under increasing pressure to raise rates to curb inflation, per multiple analyst notes; a more aggressive policy path narrows the yen’s rate differential against the dollar and removes the FX kicker that has been part of the Nikkei’s 29% YTD math.

Passive money rotation. If active managers begin underweighting Korea and Taiwan against benchmark to reduce single-name concentration, ETF inflows slow. Mechanical buying — the kind that’s rewarded Samsung and SK Hynix on every up-move via passive rebalancing — turns into mechanical selling on the way down. Concentration cuts both ways.

What We’re Watching

A handful of specific data points decide whether the asia ai concentration story extends or starts to reverse. Foreign net flows in Korean equities — already showing large-scale net selling on profit-taking in late May per Seoul Economic Daily coverage — are the cleanest near-term tell. HBM4 contract pricing, which Samsung and SK Hynix will negotiate through Q3 2026, sets the operating leverage for the memory side. TSMC’s monthly revenue prints, next out around June 10, give the foundry pulse. And the concentration spread itself — Samsung + SK Hynix as a percentage of KOSPI, TSMC as a percentage of TAIEX — is worth tracking on its own. When that number starts compressing, the passive flow has already begun rotating.

For now, the AI infrastructure cycle remains the dominant macro variable for Asian equity returns. The records being set in late May 2026 reflect that. The records do not, by themselves, broaden the trade. Anyone holding Asia exposure through a passive vehicle should at minimum know what they actually own — because the fund label and the underlying exposure have drifted further apart than they were a year ago, and the gap is still widening.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!