- Cadillac paid a $450M anti-dilution fee — split equally among the 10 existing teams ($45M each) — to become F1's 11th constructor for the 2026 season, first race March 8 in Melbourne.

- Apple TV won the US F1 broadcast rights starting 2026 — a 5-year ~$750M deal (~$140-150M/yr), a roughly 55% step-up from ESPN's expiring $90M/yr contract.

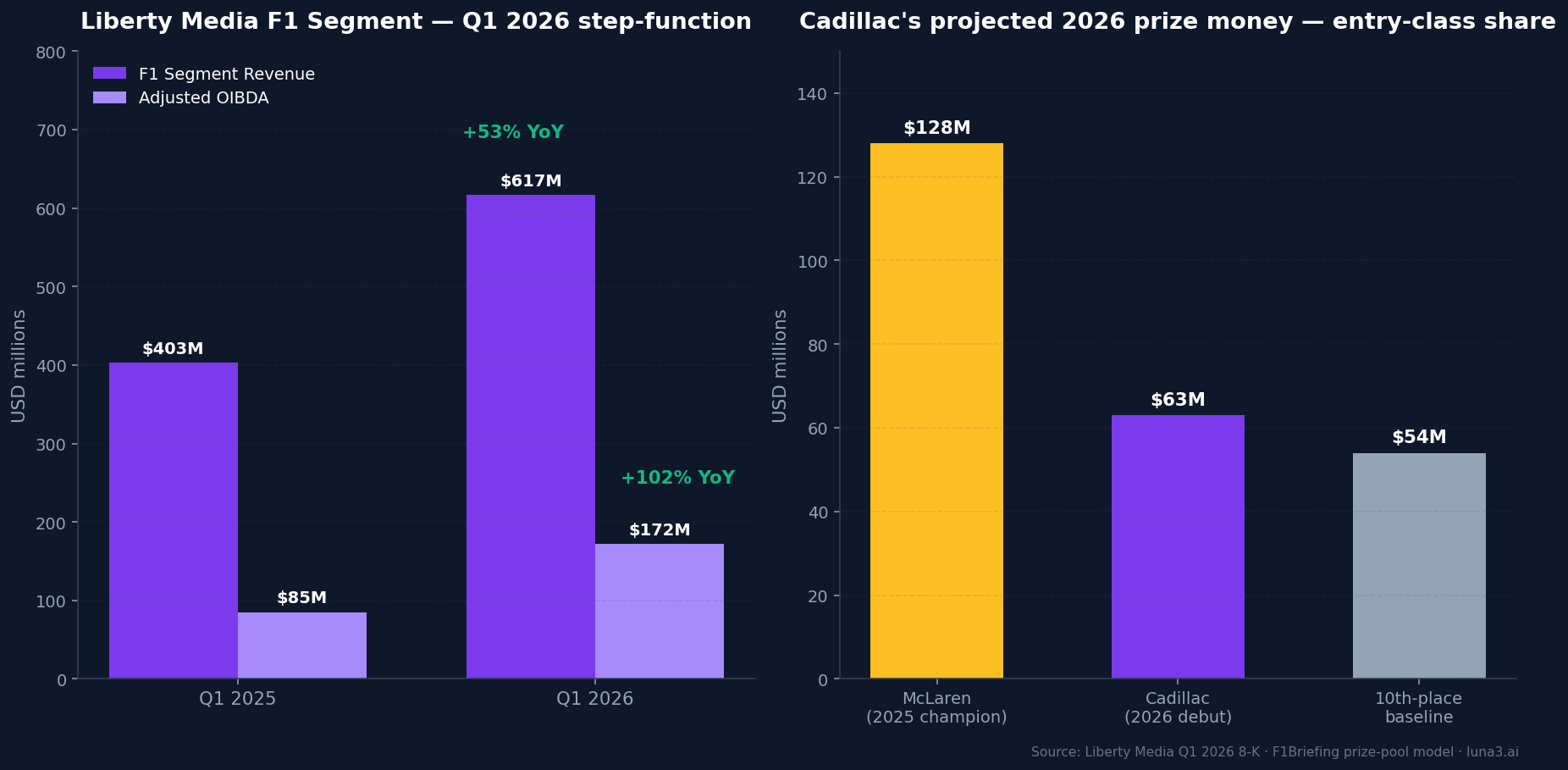

- FWONK (Liberty Media Formula One Group) is the only US-listed pure-play on the F1 economy — Q1 2026 segment revenue printed $617M, up 53% year-on-year.

The F1 Cadillac entry — quietly formalised by Formula One Management on March 7, 2025, and live on the grid since the Australian Grand Prix on March 8, 2026 — isn’t really a sports story. It’s a $450 million cheque, an 11-way prize-money split, a Concorde Agreement rewrite, and Apple TV stepping in for ESPN as the US broadcast partner. All in the same season.

For investors, the cleanest exposure to the whole package is one ticker most retail readers price as a media stock when the underlying is closer to a sovereign-grade infrastructure asset: FWONK, Liberty Media’s Formula One Group tracking stock, currently around $90 a share and a roughly $22 billion market cap.

The stock — ticker FWONK — last printed $90.33 going into publication on May 28, 2026, and is trading in the lower third of its 52-week range as the first full quarter under the new Concorde and the Apple deal prints through Liberty’s segment financials. Here’s what changed, where the money flows, and what would invalidate the case.

What just happened — and what made it possible

For 24 seasons F1 ran with 10 teams. Now it’s 11. Cadillac, owned by General Motors and run on the ground by TWG Motorsports with Graeme Lowdon as team principal, is the first new constructor on the grid since Haas in 2016.

The drivers are veterans, not rookies. Sergio Pérez, the former Red Bull number two, and Valtteri Bottas, the former Mercedes wing-man — both World Drivers’ Championship runners-up at peak. That’s a deliberate read: Cadillac isn’t paying for a two-season learning curve. They want competitive midfield results inside the cost cap from race one.

The route to entry was the slow one. The FIA approved Andretti’s standalone bid in October 2023, but FOM rejected the application on January 31, 2024. FOM’s stated rationale ran roughly: an 11th team didn’t add commercial value, would burden race promoters and dilute the existing teams’ commercial space, and the applicant didn’t bring as much to F1 as F1 would bring to it. The same gatekeeping logic Apollo or KKR uses to screen a club deal.

What unlocked the slot was a brand swap. With General Motors and the Cadillac mark replacing Andretti at the front of the bid, plus a commitment that GM would supply its own Power Units from 2029 (so the 11th team would be a full-stack constructor, not a customer in perpetuity), FOM approved the application on March 7, 2025.

Cadillac’s first-season setup runs on a customer Ferrari power unit. GM’s in-house engine programme — GM Performance Power Units, near Charlotte, NC — has roughly $290 million committed: about $150 million for the facility build-out and $140 million for factory and start-up costs. The total Cadillac commitment, including the $450 million entry fee, comes to about $740 million across 2025-2029.

For the existing 10 teams, the $450 million fee was the load-bearing concession. The previous Concorde anti-dilution figure was $200 million. Andretti could pay $200 million; only GM could write the $450 million cheque without flinching.

The Concorde Agreement — the deal nobody reads

The Concorde Agreement is the document that actually runs F1. It’s a tri-party contract between FOM (the commercial rights holder, owned by Liberty Media), the FIA (the regulator), and the teams. It runs in five-year cycles. The current cycle is 2026-2030 — the ninth Concorde — and it was signed in two parts: the Commercial Agreement in March 2025, the Governance Agreement in December 2025.

The two-step is itself a tell. Liberty locked the commercial terms first — anti-dilution, prize-money formula, cost cap, broadcast carve-outs — and then negotiated governance with all 11 teams on the table. The order matters: the teams agreed to commercial terms before they knew who their 11th was going to be.

Four levers the Concorde controls.

First, the anti-dilution payment for a new constructor: now $450 million, split equally among the 10 existing teams — $45 million each, not split with FOM. This is the single biggest commercial change in the 2026-2030 cycle.

Second, the cost cap. The 2023-2025 cap was $135 million per team. The 2026 headline cap is $215 million. That looks like a 60% loosening, but it isn’t. The new cap absorbs items that used to sit outside it: the separate capital-expenditure cap is gone, depreciation is now in scope, and any cost not 100% F1-attributed counts. For well-funded teams that had been using capex and non-F1 staff allocations to compete just below the old cap, the new structure tightens rather than loosens. For midfield teams, the effective cap is roughly unchanged.

Third, the prize-money formula. About 45% of F1’s total revenue flows to the teams. Inside that pool, 75% is allocated by Constructors’ Championship standings (Column 1), 20% by historic-performance bonuses (Column 2), and 5% is the Ferrari heritage payment — the only team that gets a payment line specifically for being itself.

Fourth, governance veto rights — which is where Cadillac’s signing matters most. All 11 teams, including Cadillac, signed the Governance Agreement in December 2025. Each received a $50 million signing incentive for committing. That’s $550 million Liberty spent just to keep the room together — a small fraction of F1 segment OIBDA but a useful signal that Liberty understands the asset’s long-term value is bound up in keeping the cartel cohesive.

The reader takeaway. The Concorde is the deed to an asset most investors don’t realise they can own a piece of. Most public-market analysts treat FWONK as a sports-media holding company. The right way to read it is closer to: a tightly-held commercial-rights concession on a global sport with regulator-enforced supply discipline, multi-decade broadcast contracts, and a fixed-supply event calendar.

Where the F1 Cadillac entry money flows — FWONK and its public co-beneficiaries

The point of the Private pillar is to map money you can’t directly invest in onto public stocks you can. Here’s the F1 Cadillac entry version of that map.

FWONK (Liberty Media — Formula One Group) is the only US-listed pure-play. Market cap roughly $22 billion as of late May 2026; share price around $90. Structure: it’s a tracking stock, not a separate legal entity — Liberty Media uses the FWONK symbol to track the economic performance of its Formula One Group segment, while Series A (FWONA) and Series K (FWONK, no voting) trade as different vote classes against the same underlying. For practical purposes, if you want F1 exposure on a US brokerage account, FWONK is the answer.

The Q1 2026 print, which captures the first quarter under both the new Concorde and the start of Apple’s US deal, came in at $617 million in F1 segment revenue — up 53% year-on-year. Adjusted OIBDA was $172 million, up 102%. Operating Income was $107 million. The step-function on the revenue line is real and just printed.

AAPL is the new US rights holder, replacing ESPN. Apple TV won the US F1 broadcast deal in mid-2025 — a 5-year exclusive package worth roughly $750 million, around $140-150 million per year, starting with the 2026 season. ESPN reportedly offered $95 million per year; Apple’s bid was roughly $120-150 million; ESPN declined to match. That’s a ~55% step-up on the per-year rights price versus ESPN’s prior $90 million contract. Drive to Survive remains on Netflix as a content-partner arrangement, and Netflix gets US livestreaming rights for one race per season (the Canadian GP for 2026).

For Apple, F1 is a Services-segment bet: the sport’s calendar is appointment viewing, the audience is high-income, and Apple TV needed a global-sport flagship after Major League Soccer underdelivered subscriber growth.

CMCSA holds the international anchor. Sky Sports’ UK and Ireland F1 rights, originally extended to 2029 in 2022, were further extended through end-2034 in a deal reportedly worth around £200 million per year. That’s the long-duration commercial-rights revenue most analysts under-model in their FWONK comps — Sky is locked in past the next Concorde cycle.

GM is the Cadillac parent. F1 is a small fraction of GM’s roughly $190 billion revenue base, but the $740 million committed (entry fee plus engine programme) is the largest single brand investment GM has made in motorsport since the Corvette factory racing programme. Watch whether the engine timeline holds for 2029 — GM’s recent record on greenfield programmes (Hummer EV delays, Cruise robotaxi shutdown) leaves room for slippage.

NFLX is content-partner-only — keeps Drive to Survive plus the Canadian GP livestream. Not a rights holder, but tied to the F1 audience funnel. Useful as a sentiment proxy, not a thesis ticker.

Why FWONK is the only pure-play. Every other F1 exposure — AAPL, CMCSA, GM, NFLX — is a single-digit revenue line item for a much bigger entity. FWONK is F1. If you want to underwrite a view on Formula 1 as a commercial-rights asset, this is the only ticker on the menu. The closest comparable thinking exercise is the NFL’s recent private equity opening, where Arctos paid $9 billion for a minority stake in the Browns — same logic about sovereign-grade sports cashflows, but the NFL has no FWONK equivalent on US exchanges. The closest other public window into a private-market asset is the SpaceX secondary market, where the pre-IPO bid runs through Hiive and 401(k) sleeves — a different mechanism but the same Private pillar principle.

The bear case

Four things would compress this view.

11-team dilution is real on a five-year horizon. The $450 million entry fee makes the math work for the existing teams’ 2026 P&L. But the per-team Column 1 share thins by roughly 9% versus the 10-team baseline. Unless commercial-rights revenue keeps scaling at the Q1 2026 +53% YoY pace — and it won’t — the prize pool gets thinner per team over the cycle. That feeds back into team-side margins, which is where governance friction tends to compound.

Cost-cap optics could pressure team profitability differently than the headline suggests. The $215 million cap looks looser, but the inclusivity expansion means well-funded teams (Ferrari, Mercedes, Red Bull, McLaren) lose accounting flexibility they’d used to manage spending just under the prior cap. If team-side returns compress, the next Concorde negotiation in 2029-2030 may see more aggressive demands for the FOM share to come down.

Streaming-rights risk. Apple’s $140-150 million per year is the high-water mark in any reasonable read. ESPN is now a non-bidder, NBC’s interest cooled, and Netflix is content-partnering rather than rights-holding. If Apple TV decides at deal-end (2030) that F1 isn’t driving enough Services-segment subscribers, the next US bidding pool is materially smaller. The optionality is on Apple’s side.

Cadillac-specific execution risk. GM’s 2029 in-house engine target is ambitious by any reading. Slips are common in greenfield engine programmes — Renault’s Alpine power-unit programme had a multi-year delay before getting competitive. If Cadillac slips to 2030-2031, Liberty loses the “full-stack new manufacturer” halo that made the entry case to FOM’s other stakeholders.

None of these would invalidate FWONK as a long-cycle commercial-rights concession. They would compress the multiple. That distinction matters for entry timing.

What we’re watching

A handful of measurable things that confirm or invalidate the case in the next 12 months.

Cadillac’s constructor points. A competitive entrant grows the audience and the prize pool. A backmarker is just an extra mouth at the same table. Track the average finishing position through the Hungarian GP in late July — the summer-break marker.

FWONK quarterly cadence. Q1 2026 printed +53% revenue YoY. Watch whether Q2 (reporting in August) maintains the step-function as Apple’s first full-season subscriber funnel matures. A drop to +25-30% would suggest a one-quarter effect; sustained +40%+ would suggest structural re-rating.

Sponsorship ARR. Q1 2026 added Salesforce and Allwyn extensions, plus new multi-year deals with Marsh, FanDuel, Betway, and Standard Chartered. FanDuel and Betway are the first explicit retail-betting sponsorship wave — watch whether DraftKings follows in the next two quarters.

Apple TV F1 engagement. Sustained Apple TV+ time-on-app for F1 sessions is the leading indicator on whether Apple gets the Services-segment ROI it underwrote. Apple’s own F1 movie (Brad Pitt, June 2025) grossed $634 million worldwide and won the Best Sound Oscar — the cultural traction is there; the question is whether it converts to subs.

Next Concorde signalling. Liberty’s first public commentary on the 2031-onwards cycle will land in earnings calls through 2027-2028. The earlier the signalling, the more confidence the team-share negotiation is going Liberty’s way.

The clean read on F1 as an asset is that it sits closer to a private-credit-backed infrastructure concession than to media. Multi-decade commercial-rights contracts, regulator-enforced supply discipline, a fixed-calendar event delivery model, and a tightly-held cartel of operating partners. Most investors price it as if it were Comcast. The F1 Cadillac entry — a $450 million cheque, an Apple TV deal, a fresh Concorde cycle, and a Q1 print that says the whole thing just got measurably bigger — is the moment the asset becomes legible. FWONK is the public-equity vehicle for the trade.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!