- Arctos paid 41-47% above independent appraisals ($6.14B Sportico, $6.4B Forbes) for 10% of the Browns — and it is not because they think Cleveland is undervalued

- KKR (publicly traded) quietly became the dominant NFL private equity platform via the Feb 5, 2026 Arctos buyout — a structural shift that is barely priced into the stock

- Retail can’t own 10% of a team — but can own the platform that earns 1.5%+20% in fees on the entire $15B sports book

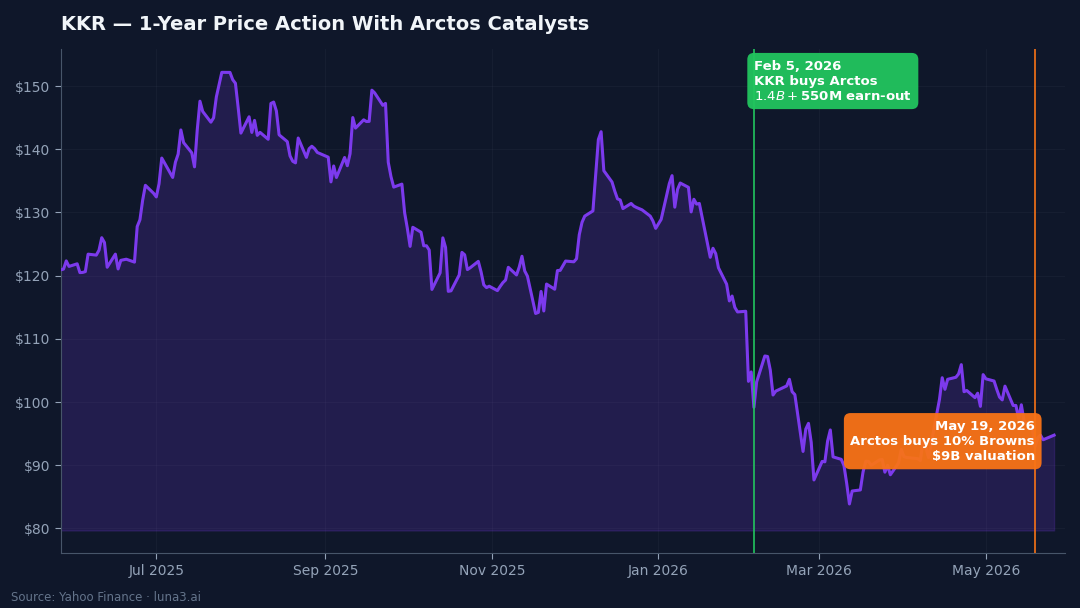

NFL private equity just produced its cleanest valuation signal yet, and it has nothing to do with quarterback play. Arctos Partners is buying 10% of the Cleveland Browns at a $9 billion valuation, in three approved tranches, the first of which closed at $270 million for a 3% stake. Sportico’s most recent published appraisal of the Browns: $6.14 billion (#23 of 32). Forbes (Aug 2025): $6.4 billion (#18 of 32). The deal is priced 47% above the lower mark and 41% above the higher one — paid by a fund that rolled into KKR’s $744 billion AUM platform three months earlier.

The stock — ticker KKR — last traded at $94.04 going into publication on May 27, 2026. The Arctos transaction is the most under-appreciated catalyst inside that quote. This isn’t about Cleveland or football. It’s about the highest scarcity premium in public markets right now and who actually captures it.

How NFL private equity got approved

On August 27, 2024, NFL owners voted 31–1 to allow private equity minority stakes for the first time in league history. The official version is Resolution JC-7. The lone no came from Bengals EVP Katie Blackburn, continuing a Brown-family pattern of voting against league financial expansions. The NFL was the last major US league to open — the NBA, NHL, MLB, MLS, and NWSL had all already done it.

The NFL’s cap structure is the strictest of the major leagues. The headline numbers most articles cite — “30% aggregate PE cap” — are wrong. That’s the NBA/NHL/MLB/MLS rule. The actual NFL framework:

- Up to 10% of a team can be owned by private equity in aggregate — across all PE funds combined, not per fund.

- Minimum 3% per stake — no token positions.

- Maximum 6 NFL teams per fund — once a firm hits the cap, the next deal goes to a competitor.

- Maximum 20% of a fund’s capital in any one team.

- 6-year minimum hold.

- Fund must have $2 billion+ in committed capital.

- Passive only — no voting rights, no governance seats, no GM hiring input.

The approved-firm shortlist is shorter than the press coverage suggests: Arctos, Ares, Sixth Street, and one consortium nicknamed “The Avengers” (Blackstone, Carlyle, CVC, Dynasty Equity, and Ludis — Ludis is led by Hall of Fame running back Curtis Martin). Four platforms competing for ~32 teams × ~3 PE slots = ~96 total stakes ever available, but with the 6-team-per-fund cap, real competition tightens fast.

Why did the NFL hold out for so long? The revenue-sharing model is a public good — each team gets roughly $400 million per year from the national media deal regardless of W/L record. Private equity was seen as cap-table noise that could complicate the next collective bargaining negotiation. The flip happened when franchise valuations broke $7 billion and family heirs started looking at estate-tax bills they couldn’t cover with cash. PE became the only buyer that could write a check for a minority slice without forcing a control sale.

What’s actually happened in the 18 months since the rule passed: four PE deals. Bills (Arctos, Dec 2024, $5.8B valuation). Dolphins (Ares, Dec 2024, $8.1B — plus a separate 3% to Joe Tsai). Chargers (Arctos, May 2025, undisclosed). Browns (Arctos, May 2026, $9B). The Bears’ 2.35% sale at an $8.9 billion valuation in September 2025 sometimes gets counted; it shouldn’t — that was an internal McKenna estate transfer to the McCaskey and Ryan families, not a private equity deal. Total PE capital deployed across the four: roughly $700 million. The Browns deal is the first valuation reset that ratifies a floor for the next wave.

How the Browns deal got to $9B

Bloomberg broke the story on May 19, 2026: the Cleveland Browns selling 10% to Arctos at a $9 billion valuation, with the deal closing in three tranches. The NFL Finance Committee approved tranche one shortly after — a 3% stake at roughly $270 million. The arithmetic: $270M / 3% = $9 billion. Sportico’s most recent appraisal is $6.14 billion (#23 of 32 NFL teams). Forbes, in its August 28, 2025 valuation update, put the Browns at $6.4 billion (#18 of 32). Arctos paid 47% above the Sportico mark and 41% above the Forbes mark.

Where is the $270 million going? The Browns’ new $2.6 billion stadium project. Jimmy and Dee Haslam have pledged to fund $1.76 billion of that out of pocket. The Arctos tranche helps backfill the family’s stadium commitment without forcing a sale of control. That detail matters — PE money is functioning as illiquid mezzanine for franchise capex, not as a thesis on the team’s competitive trajectory.

What Arctos didn’t pay for: trailing EBITDA (the Browns are middle-of-pack on revenue and bottom-tier on operating margin given stadium debt service), quarterback play, or playoff probability. None of it. So why pay 47% over the published appraisal? Four scarcity levers that the comp-based valuation models cannot capture.

- Asset scarcity. Only 32 NFL franchises exist. PE-permitted minority slots are capped at 10% per team in aggregate, and each fund maxes at six teams. With four platforms competing (Arctos, Ares, Sixth Street, the Avengers), the demand-supply balance is structurally tight — and it gets tighter every time a competitor closes another deal.

- No “minority discount” in transactions. Academic valuation theory says illiquid minority stakes trade at 20–30% discount to control value. In NFL PE practice, they don’t — because there is no forced seller. The Haslams set the price; PE buys at par or doesn’t get in. The minority-discount adjustment is a model artifact when supply is constrained.

- Media-rights embedded growth. The current NFL media deal is over $110 billion across 11 years (2023–2033), averaging roughly $10 billion per year. CBS, FOX, and NBC each pay ~$2 billion annually; ESPN is around $2.7 billion; Amazon pays $1.2 billion for Thursday Night Football. The 2033 renewal is the upside vector. How big the step-up is depends entirely on whether linear-TV cash flow holds and streamers keep paying premiums.

- Optionality on majority sales. If the Haslams ever sell the franchise outright — a 10-25 year tail — the existing 10% limited partners gain right-of-first-refusal optics on the next round. The Seahawks auction (Paul Allen estate, $9–11 billion range expected) is the validation event coming this year. If it clears $10 billion, every minority stake struck in 2024–2026 re-rates instantly.

Why can’t Sportico price this in? Their model is DCF + comparable transactions. Comps don’t capture the access premium because there are no public comparables for “the only firm approved across all five major US sports leagues.” The $9 billion isn’t a Cleveland number. It’s an Arctos-and-only-Arctos number.

KKR owns this trade now — the February 2026 deal that changed everything

The most under-appreciated piece of the Browns story happened three months earlier and 1,500 miles away. On February 5, 2026, KKR announced a definitive agreement to acquire Arctos Partners. Initial consideration: $1.4 billion. Breakdown straight from KKR’s 8-K filing: $300 million in cash, $900 million in KKR equity to existing Arctos shareholders (with the management portion vesting through 2030), and $200 million in additional equity to be allocated by 2028 (vesting through 2033). On top of that, up to $550 million in future equity tied to KKR’s share price and business-specific performance, vesting through 2031.

What did KKR actually buy? A $15 billion AUM book — and the only firm approved for multi-team ownership across all five major US leagues (NBA, NFL, MLB, NHL, MLS). The Arctos portfolio now contains 30+ team stakes including PSG, Liverpool FC, Atalanta, the Aston Martin Formula 1 team, SeatGeek, the Golden State Warriors, Sacramento Kings, Utah Jazz, six MLB teams (Dodgers, Red Sox, Cubs, Giants, Astros, Padres), four NHL teams, Real Salt Lake in MLS, and three NFL teams (Bills, Chargers, and now Browns).

The internal positioning at KKR is a new unit called KKR Solutions — sports plus GP solutions plus secondaries, with sports as the marquee. Until this deal, KKR didn’t have a dedicated secondaries unit; rivals Blackstone, Ares, and TPG all did. The Arctos buyout closes the secondaries gap and brings sports under one roof simultaneously.

The earnings math is straightforward: a 1.5% management fee on $15 billion AUM equals $225 million in annual recurring revenue, plus a 20% performance carry on net asset appreciation. If sports franchise values compound at 8% per year (which is consistent with the last decade), the carry stream alone throws off $400–500 million per year by 2030. That’s before the platform attracts net-new capital, which it will. The previous active-management business model is dying; the alts fee-on-AUM model isn’t — this is the same fee-economics story we covered in the $640 billion walking out of active mutual funds in 2025.

The contrast against KKR’s closest public peers explains why this is a re-rating event, not just a tuck-in M&A. Apollo (APO) is the largest alts firm by AUM but has no NFL stake as of May 2026 — the competitive question is whether Apollo builds a sports vertical from scratch or acquires a smaller competitor. Ares (ARES) has the Dolphins stake plus a separate sports book (Inter Miami MLS, McLaren F1, Atlético Madrid), but no Arctos-scale infrastructure. Blackstone (BX) is in the NFL-approved Avengers consortium with no closed deal yet. KKR didn’t build a sports platform; it bought the only complete one in existence.

“Complete” here means league relationships, deal-team underwriters, valuation models, ops support for franchise improvement plans, and secondary-sale capability. None of those exist as line items. They have to be built over years of relationship work. KKR bought a finished platform.

Where the money flows — the public-ticker map

Retail can’t buy 10% of a team. But it can own the platform that owns the team. Five ways to express it:

- KKR (NYSE: KKR) — the dominant exposure. Arctos is now a wholly-owned KKR platform. Every fee on every Browns, Bills, Chargers, PSG, Liverpool, Warriors, Kings, Jazz, and MLB stake flows to KKR shareholders. This is the cleanest single-name expression of the NFL private equity trade.

- ARES (NYSE: ARES) — the runner-up. Owns 10% of the Miami Dolphins (Dec 2024, $8.1B valuation; the package included Hard Rock Stadium and the F1 Miami Grand Prix). NFL-approved. Smaller sports book than Arctos, but Ares’ broader credit-plus-secondaries platform has its own momentum.

- APO (NYSE: APO) — outside-looking-in. Apollo is the biggest alts manager by AUM but has zero NFL stakes as of May 2026. If Apollo enters by buying a smaller approved firm rather than building, that’s a fast and material multiple expansion. If they build organically, slower.

- BX (NYSE: BX) — consortium member, no closes yet. Blackstone sits inside the Avengers consortium (with Carlyle, CVC, Dynasty Equity, Ludis). No deal closed yet, but the consortium structure means it gets a deal eventually — the timing is the question, not the existence.

- OWL (NYSE: OWL) — adjacent. Blue Owl has alts in expansion mode, minor sports exposure, no NFL approval yet. The least direct expression of the thesis.

There’s also a publicly-traded franchise comp track:

- MSGS (NYSE: MSGS) — Madison Square Garden Sports owns the Knicks and Rangers. The most direct public-traded NFL/NBA franchise analog at roughly $8.6 billion market cap.

- LSXMK (NASDAQ: LSXMK) — Liberty Media Atlanta Braves; the closest public MLB comp.

- FWONK (NASDAQ: FWONK) — Liberty Media Formula 1; the original “league-as-public-equity” structure that predates the alts cohort.

The franchise comps and the alts cohort don’t trade together. MSGS trades on Knicks fortunes and arena ops; KKR trades on platform fee economics. The reader who wants the cleanest exposure to the NFL private equity story specifically wants KKR. The reader who wants diversified exposure to alts-in-sports wants the four-name basket (KKR + ARES + BX + OWL). The reader who wants direct franchise correlation wants the comp basket (MSGS + LSXMK + FWONK). They’re three different trades pointing at vaguely overlapping themes.

The bear case — what could break this

The 47% premium isn’t risk-free, and ignoring the bear case is what gets investors hurt at the top of structural booms. Five real risks:

- Media-rights reset. The embedded growth thesis assumes the 2033 NFL media deal renews above $10 billion per year. If linear TV cash flow collapses further and streamers refuse to pay premiums for sports content, the renewal could come in flat. That outcome breaks the IRR math on every NFL deal struck between 2024 and 2026.

- Antitrust. The NFL’s revenue-sharing model depends on the Sports Broadcasting Act’s 1961 antitrust exemption. The DOJ has opened an active antitrust investigation into NFL TV deals. Senator Mike Lee (R-UT, chair of Senate Judiciary’s Antitrust Subcommittee) sent a letter on March 3, 2026 to DOJ and FTC asking whether modern subscription-streaming distribution still fits the 1961 statute’s “sponsored telecasting” definition. Repeal-by-legislation is low probability. Regulatory action is not — the 2024 Sunday Ticket jury verdict against the NFL was $4.7 billion before being overturned by the judge on appeal.

- CBA risk (2030). The next collective bargaining agreement is in 2030. If the player share moves from the current 48% (48.5% in 17-game seasons) to 50%+, owner economics compress and PE stake values follow.

- Alts-sector drawdowns. The public-alts cohort (KKR / APO / ARES / BX / OWL) is up sharply since January 2024. A standard alts-sector drawdown takes the group down 35–40%. That doesn’t break the thesis — it breaks the entry timing.

- Sportico might be right. If media rights deflate and the Browns continue operating at sub-$200M EBITDA, $9 billion is roughly 45x earnings. Even at 5% growth, that’s pricing a $20 billion exit. That could happen. It could also not.

The structural risk that doesn’t get talked about enough: PE returns depend on majority exits. A 10% minority stake can’t sell to another minority buyer without league approval. The real liquidity event is when the family owner sells the franchise outright. That’s a 10–25 year tail. NFL PE is, mechanically, a multi-decade hold. The same illiquidity-mismatch problem hit private credit two months earlier when Apollo gated its $25B ADS fund — the asset side moves slower than the liability side, and retail-evergreen vehicles aren’t the right wrapper for either.

What we are watching

- Seahawks auction (Paul Allen estate, $9–11 billion expected). The validation event. If it clears $10 billion, Sportico’s appraisal model is broken and the entire cohort re-rates upward.

- KKR Q2 2026 earnings (August). First full quarter with Arctos consolidated. Watch the management-fee disclosure on the $15 billion sports book and how the new KKR Solutions segment is broken out in the financial statements.

- The next NFL PE deal. Arctos has done three (Bills, Chargers, Browns). Ares has done one (Dolphins). Sixth Street and the Avengers consortium are at zero. Watch which platform closes next — the order matters for competitive positioning.

- Apollo entering NFL. Does APO buy a smaller approved firm or build organically? The acquisition path means rapid multiple expansion; the build path is slower.

- DOJ antitrust probe outcome. Any meaningful action on the NFL TV-rights investigation directly impacts the media-rights growth thesis that anchors the franchise valuations.

- LIV Golf $250M raise. Different sport, but a real-time stress test of whether sports private capital still bids when one of the larger plays (LIV) is essentially out of capital.

- Cash on the sidelines. The retail demand for alts wrappers has been funded by the $7.77 trillion sitting in money market funds. That cash chasing alts is what made the retail-evergreen PE product work in the first place — why $7.77 trillion is still on the sidelines remains the key macro variable behind the inflows.

Bottom line

The Browns at $9 billion isn’t a Cleveland story. It’s the first clean signal that the structural shift NFL private equity began in August 2024 is now repricing the entire asset class — and the access slot to that repricing isn’t a team, it’s a fee-bearing public platform. KKR bought the only complete one in February. Arctos closed the third NFL stake in May. The rest of the public-alts cohort is positioning for what comes next. The cheap signal here isn’t the deal valuation; it’s how few public investors are paying attention to who actually captures the fees.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!