- ASML holds a near-total monopoly on EUV lithography — the machines that print every advanced AI chip — and no EUV system has ever been delivered to China.

- Q1 2026 brought €8.8 billion in net sales (+13% year on year) and a backlog near €38 billion, yet the shares slipped as the US tightened China export curbs.

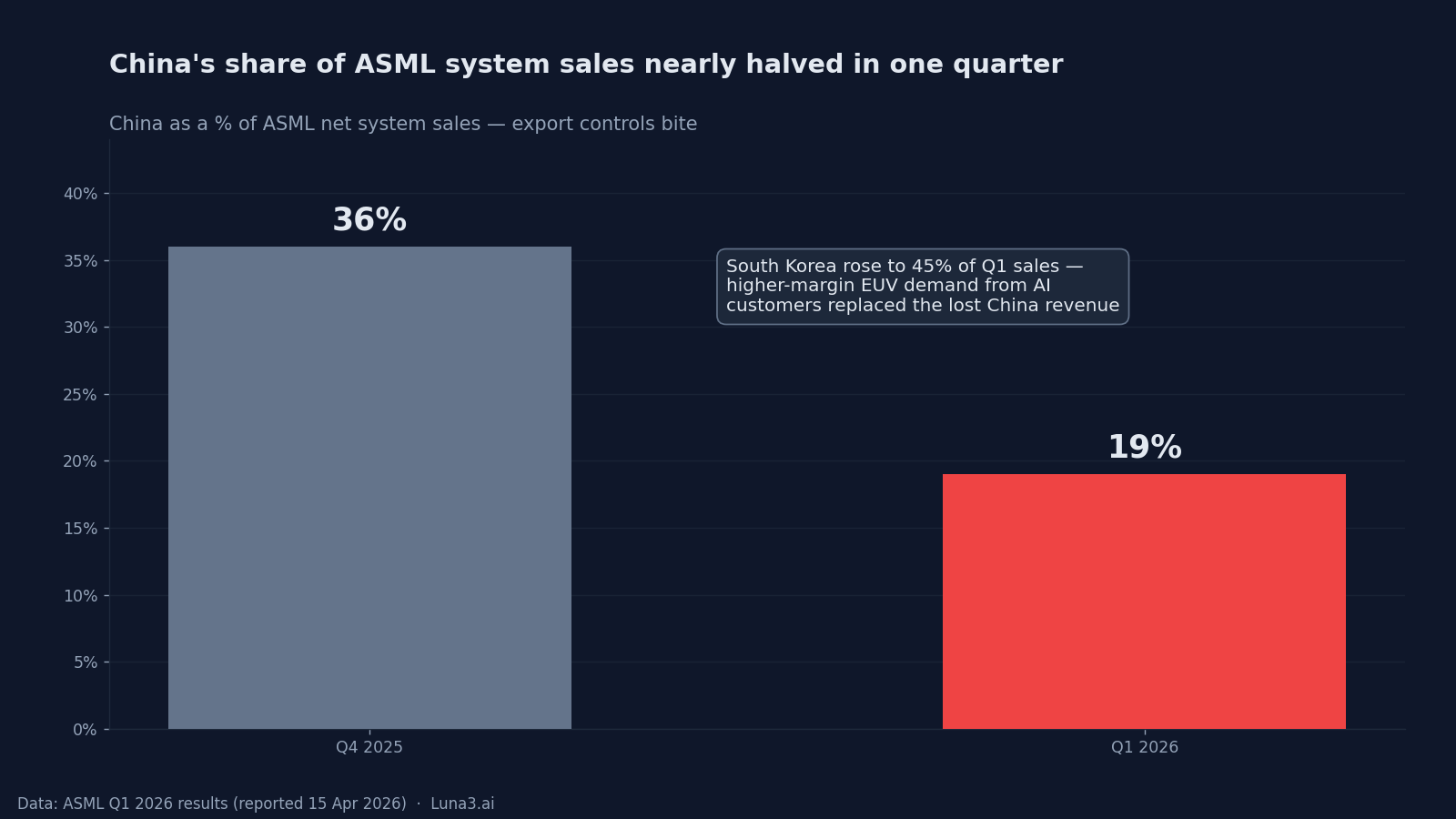

- China fell from 36% to 19% of system sales in a single quarter; higher-margin EUV demand from South Korea (45% of Q1), Taiwan and the US more than filled the gap.

ASML stock just did something that ought to feel contradictory: it hit a record high on the back of the very quarter that exposed its biggest vulnerability. The Dutch company’s shares traded around €1,400 in late May — within a whisker of the €1,431 all-time high set on 25 May 2026 — even as the earnings report powering that run showed China collapsing from roughly a third of its machine sales to under a fifth. To see why the market waved that away, you have to grasp what ASML actually is: the single chokepoint the entire AI buildout — and the hyperscaler capex cycle behind it — has to pass through.

The stock — ticker ASML.AS on Euronext Amsterdam — last changed hands around €1,399 going into publication on May 30, 2026, just shy of that 25 May record and up roughly 110% over the trailing twelve months. A run like that, in a company already worth about €550 billion, is the market pricing in a very specific story. Here is the story — and the part of it that is genuinely contested.

The one machine the AI era can’t be built without

Strip away the jargon and ASML’s moat is almost comically simple: it is the only company on Earth that makes extreme ultraviolet (EUV) lithography machines — the room-sized systems that etch the finest features onto leading-edge logic and memory chips. Not the leading maker. The only one. Every advanced processor that trains or runs a large AI model, whoever designs it, is printed on a tool that came from a single campus in Veldhoven. It took two decades and tens of billions in research to get there — and the light-source physics involved is precisely why no competitor has replicated it.

That is why ASML sits upstream of everyone. TSMC, Samsung, Intel and SK Hynix all have to buy from it to stay on the leading edge — and so, indirectly, does every hyperscaler racing to stand up AI capacity and every fabless designer shipping the custom AI silicon those fabs print. The next rung up is High-NA EUV, the roughly €350 million ($380–400 million) successor system ASML has begun shipping in small numbers.

Here the honest nuance matters, because the High-NA ramp is not a uniform march. Intel deployed the first High-NA system to support its 14A node and is leading adoption; TSMC has signalled it will stick with current-generation 0.33-NA EUV for its A14 node rather than absorb High-NA’s cost just yet; Samsung is pacing toward roughly 2027. So the monopoly is rock-solid at today’s EUV generation, while the High-NA upgrade cycle is real but back-end-loaded — at once a source of recurring future demand and a reminder that customers can defer the priciest tools when budgets tighten.

What the order book is really telling us

ASML’s Q1 2026 results, reported in mid-April, were strong on the numbers that matter: €8.8 billion in net sales, up 13% year on year, at a 53% gross margin, with a backlog of roughly €38 billion — more than half of it EUV — stretching into 2027. Management held full-year guidance at €36–40 billion, and bookings came in well ahead of estimates.

The backlog is the part worth dwelling on. Because every advanced fab funnels through ASML, its order book is arguably a cleaner read on the AI-capex cycle than any single hyperscaler’s quarterly guidance — it aggregates the spending intentions of the entire leading edge, including the demand for the advanced-packaging bottleneck downstream that turns raw chips into finished accelerators. A backlog reaching into 2027 says the people who build AI hardware are committing capital years out, not quarters.

The caveat — and we would rather state it than bury it — is that a backlog is not locked revenue. Slots can be pushed, reconfigured or, in rarer cases, cancelled, and ASML’s order intake is famously lumpy from one quarter to the next. The signal is in the direction of travel and the EUV mix, not in treating €38 billion as money already in the bank.

The China overhang nobody can hand-wave away

Now the fault line. China was about 36% of ASML’s net system sales as recently as the fourth quarter of 2025. One quarter later it was 19% — and the company guides to roughly 20% of total sales from China for full-year 2026. That is not a wobble; it is a structural reset driven by the China export-control overhang.

Export rules now effectively bar EUV systems from China entirely — by ASML’s own account, not a single EUV machine has ever been delivered there — and increasingly constrain the most advanced DUV immersion tools, with fresh US proposals threatening to tighten further. That last point is why the stock actually slipped after a quarter it beat on: the market was reacting to the policy trajectory, not the print.

The rebuttal, and it is a real one, is the mix. The revenue ASML is losing in China was lower-margin DUV; what is replacing it is higher-margin EUV demand from AI customers in South Korea — which jumped to 45% of Q1 sales — alongside Taiwan and the US. Less China, but a richer sales mix. The bear case (a geopolitical single point of failure, plus a determined Chinese push toward domestic self-reliance that could erode the service base over time) and the bull rebuttal (a margin upgrade, with demand that more than backfills the gap) are both true at once. That tension is the entire investment debate compressed into one quarter.

What ASML stock is actually pricing in

At about €550 billion — roughly $615 billion — ASML is comfortably Europe’s most valuable company, ahead of Roche and LVMH, and it trades at a premium multiple to the broad market. That valuation is the market paying up for the monopoly and the multi-year AI-capex runway. It also means the bar is high: when a company is priced for dominance, even a strong quarter can sell off on a single adverse headline, which is precisely what happened in April.

It helps to situate ASML in the wider tape, too. The same enthusiasm lifting it is the same AI-concentration trade playing out across Asia and, in Europe, in names like Sweden’s Sivers Semiconductors — a speculative bid piling into anything credibly attached to AI infrastructure. ASML is the blue-chip, monopoly-backed end of that spectrum rather than the lottery-ticket end, but it is not immune to the cohort’s mood swings.

So what is the stock pricing in? Roughly this: that EUV demand compounds through the AI buildout, that High-NA becomes the next leg of growth, and that the China hit is a manageable mix-shift rather than the first crack in the moat. A record backlog and an all-time high say the market is confident on all three. A 17-point China cliff and a rich multiple are the reasons that confidence is worth interrogating.

What we’re watching from here

Four things will tell us which way the debate resolves. First, the High-NA cadence — does TSMC eventually commit, or hold on 0.33-NA for A14? Intel’s execution on the first units is the early tell. Second, China policy: whether Washington tightens DUV rules further or a thaw emerges, and how fast China’s domestic toolmakers close the gap. Third, the hyperscaler capex signals upstream of the backlog — if AI-infrastructure spending plateaus, ASML’s order book is the first place it would show up. And fourth, conversion: whether that ~€38 billion backlog ships on schedule or slots begin to slip. You can track ASML’s own figures on its investor relations pages.

None of that resolves into a tidy verdict, and it shouldn’t. The cleaner takeaway is structural: for now, the company that gates the entire AI buildout is selling every machine it can make, at a record backlog, while carrying a geopolitical risk no amount of demand can fully hedge. Watch the order book and the export headlines in tandem — between them, they will tell the next chapter of this story well before the share price does.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!