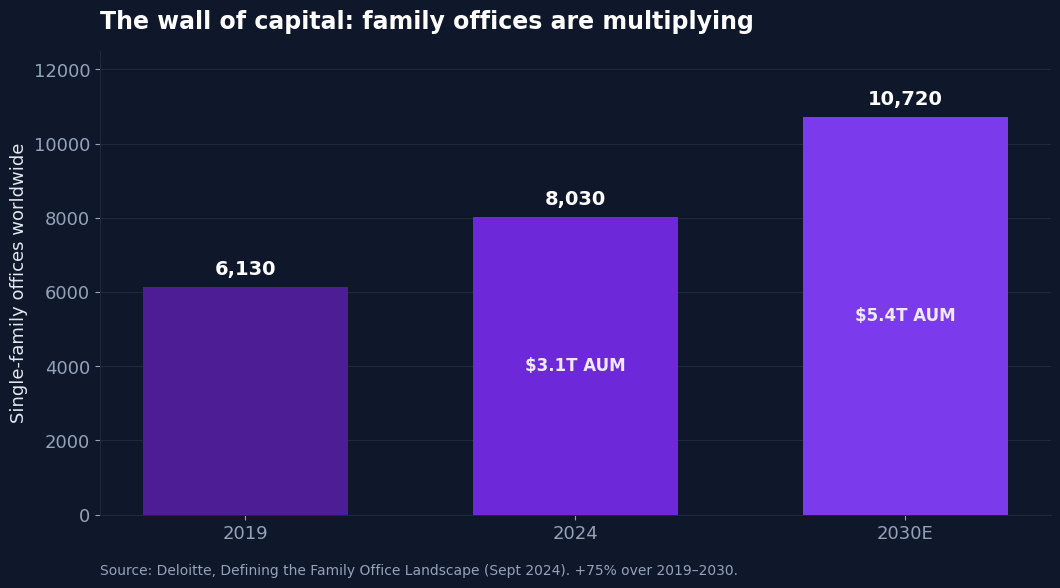

- A family office is a private company built to invest one family's fortune. Deloitte counts 8,030 of them worldwide in 2024, managing about $3.1 trillion — a figure set to reach $5.4 trillion by 2030.

- They are going direct: direct deals and co-investments now make up over 40% of the typical family-office private-equity sleeve, as families skip the 2-and-20 fund fees.

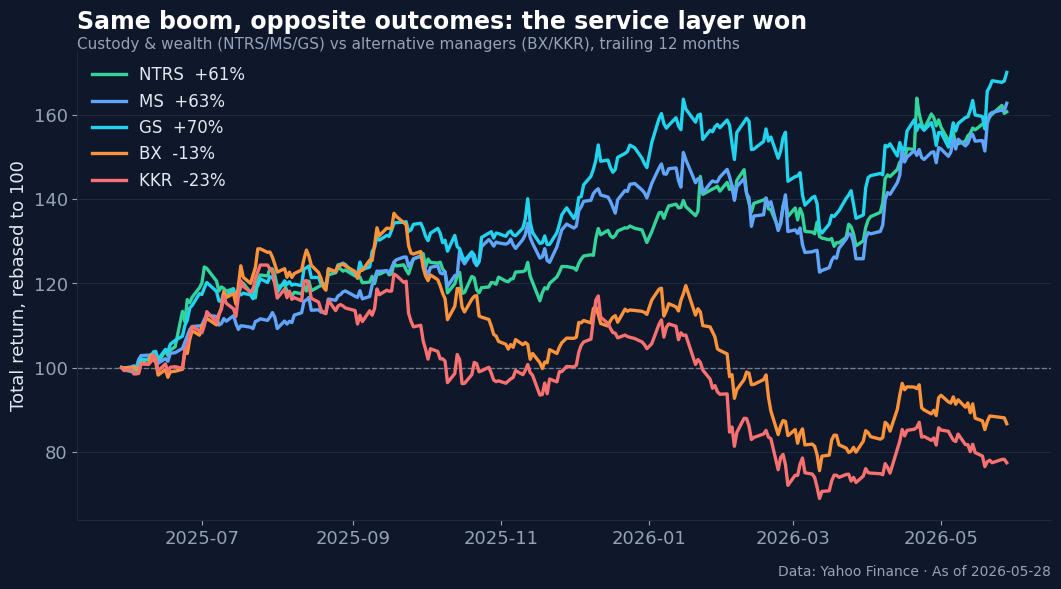

- You can't invest in a family office. But the custodians (NTRS), wealth platforms (MS, GS) and alternative managers (BX, KKR, APO) that serve them are all public — and over the past year, the service layer was the side that won.

Yesterday — May 28 — UBS released its 2026 Global Family Office Report, a survey of 307 of these vehicles whose families are worth an average of $2.7 billion each. Family office investing has quietly become one of the largest and fastest-growing forces in global markets — and one almost no outsider will ever be allowed to join. You can’t wire money into a family office. There are no units to buy and no investor portal, because there is no door. That exclusivity is exactly what creates the opening for everyone else: the custodians, banks, and asset managers that serve these families trade on public exchanges, and over the past twelve months, owning the right ones was the cleanest way to ride the boom.

This is the recurring shape of private markets, and the reason this category exists: it’s money you can’t directly invest in, but that moves public beneficiaries you can. So let’s do two things — explain how the ultra-wealthy actually deploy capital, and then map the publicly traded plumbing underneath it.

What a family office actually is

Strip away the mystique and a family office is just a private company that exists to manage one family’s investments, taxes, estate planning, and often its philanthropy and lifestyle. It is not a fund. There are no outside limited partners, no fundraising deck, and nothing for you to buy. A single-family office (SFO) serves exactly one family; a multi-family office (MFO) pools several families to share the overhead. The distinction matters because the economics are brutal at the bottom.

Running a real SFO costs roughly $1–2 million a year — investment staff, legal, tax, custody, technology. That only makes sense once a family’s investable assets clear about $100 million, and many advisers put the practical bar closer to $250 million. Below $100 million, more than a quarter of single-family offices fold within three years; the fixed costs eat the edge. That’s why everyone short of that threshold rents the function from a private bank or a multi-family office instead of building one.

The scale of all this is what’s changed. Deloitte’s Defining the Family Office Landscape report counts 8,030 single-family offices worldwide in 2024, up from 6,130 in 2019, and projects 10,720 by 2030 — a 75% jump across the decade. Their assets under management are estimated at $3.1 trillion today, headed for $5.4 trillion by 2030. (Keep two numbers separate: that AUM figure is smaller than the families’ total wealth, which Deloitte pegs at $5.5 trillion now and $9.5 trillion by 2030.)

One more structural feature explains a lot of the behavior that follows: most SFOs don’t have to register with regulators. The SEC’s family-office exemption — rule 202(a)(11)(G)-1, adopted in 2011 under Dodd-Frank — excludes a family office from the Investment Advisers Act of 1940 as long as it advises only family members, is owned and controlled by the family, and doesn’t hold itself out to the public. The trade-off for that privacy is disclosure: the public never sees their holdings, which is why every AUM figure here is an estimate, not a filing.

How family office investing actually works

Family offices invest more like university endowments than like retail portfolios. UBS’s 2025 survey put the average allocation at roughly 30% equities, 18% fixed income, 8% cash — and the rest, more than 40%, in alternatives: 21% private equity, 11% real estate, 4% private debt, 4% hedge funds, plus gold and infrastructure. That alternatives weight is the whole game. A long horizon and zero redemption pressure let a family office hold illiquid assets that an open-ended retail fund simply can’t, and harvest the illiquidity premium most portfolios are structurally unable to touch.

This year’s report shows where the marginal dollar is moving. Developed-market equities sit near 27%, real estate is being trimmed toward 8% from 11%, and gold is ticking up toward 3%. The loudest signal is currency: 65% of family offices expect confidence in the US dollar’s reserve status to weaken, and 60% plan to change their strategic allocation in the next twelve months. Artificial intelligence has become a cohort-wide theme, with 65% now invested in it. These are not traders chasing a quarter — they’re repositioning a multi-decade book.

Why they’re going direct — and where it stops

The structural shift worth understanding is that family offices increasingly skip the fund and do the deal themselves. Direct investments and co-investments now account for more than 40% of the typical family-office private-equity sleeve, a sharp rise over the past decade, and 37% of offices told UBS they plan to increase direct private equity over the next five years. They are also active buyers in the pre-IPO secondary market, picking up stakes in names like SpaceX years before any listing.

Three forces drive it. The first is fee fatigue: paying 2% of assets plus 20% of profits on every dollar, every year, compounds into an enormous drag over a thirty-year horizon. The second is control — a direct stake lets the family choose exactly what it owns and hold it as long as it likes, with no fund clock forcing an exit. The third is talent: the largest offices now hire ex-private-equity and ex-banking professionals and run like boutique institutions.

It would be easy to overstate this. Direct investing demands a real team, real deal flow, and real underwriting, and the long tail of smaller offices still leans heavily on funds and private banks — the “going direct” story is concentrated in a few hundred mega-offices, not the whole population. It’s cyclical, too: the same UBS data shows families actually trimmed private equity in the near term as slow exits and expensive financing made new deals harder. That’s selective patience, not a retreat. And here’s the key point for public-market investors — even the families building in-house teams still outsource custody, administration, tax, estate work, and lending. That outsourced layer is exactly what you can buy.

Where the money flows — the public-ticker map

There are three public expressions of the family-office boom, and over the past year they did not behave alike.

Custody and asset servicing is the purest proxy. Northern Trust (NTRS) runs a dedicated Global Family & Private Investment Offices group that says it has worked with more than 450 of the world’s wealthiest families and serves roughly 30% of the Forbes 400; it expanded the service in April 2025. BNY (BK) custodies for family offices and RIAs through Pershing, and State Street (STT) provides asset servicing at institutional scale. These businesses earn fees on assets they hold and administer, regardless of how those assets perform — the most resilient slice of the chain.

Wealth management and private banking is the second layer. Morgan Stanley (MS) and Goldman Sachs (GS) both run family-office service arms, and UBS (UBS) — the bank that publishes the report this article opened with — is the dominant global player and is US-listed.

Alternative asset managers are the third, and the most direct beneficiary of the alts-heavy allocation: Blackstone (BX), KKR, Apollo (APO), Ares (ARES) and Blue Owl (OWL). Family offices are major limited partners in their funds and the explicit target of their private-wealth push — Blackstone’s private-wealth solutions arm, launched in 2011, now runs more than $250 billion for individuals, and its individual-investor vehicle BXPE has gathered roughly $8.5 billion since 2024. These are the same fee-on-mandate economics that make the public alternative managers such clean ways to own private capital.

The chart is the surprise. Over the past twelve months the service layer ran away from the alts. The custodians and wealth platforms — NTRS, MS, GS, BK, STT — gained roughly 60–70% each, while the marquee alternative managers fell: Blackstone down about 13%, KKR down 23%, Ares down 21%, Blue Owl down 43%, with Apollo roughly flat. The obvious “family-office play” — owning the firms whose funds these families pile into — was the one that lagged, caught in the same rate-and-redemption cycle that gripped private credit. The boom paid off, but in the plumbing, not the headline names.

| Company | Ticker | How it earns from family offices | Past 12 mo |

|---|---|---|---|

| Northern Trust | NTRS | Custody + Global Family Office servicing | +61% |

| Goldman Sachs | GS | Private wealth + Ayco family-office services | +70% |

| State Street | STT | Asset servicing / custody | +67% |

| Morgan Stanley | MS | Wealth management + family-office unit | +63% |

| BNY | BK | Custody via Pershing | +61% |

| Apollo | APO | Alts LP capital + wealth channel | −2% |

| Blackstone | BX | Alts LP capital + private-wealth (BXPE) | −13% |

| Ares | ARES | Alts / private credit | −21% |

| KKR | KKR | Alts LP capital + K-series | −23% |

| Blue Owl | OWL | Private credit / GP stakes | −43% |

One layer stays stubbornly private: the software. Addepar, iCapital, Arch and Canoe are where family offices actually run their reporting and access private deals, but none trade publicly. For now, the only way to own that theme is through the custodians and managers above.

The bear case — what could break this

The same trend that grows family-office influence can shrink it for the people who serve them. If families build in-house teams and do deals directly, they pay less in advisory fees and less in fund carry — the disintermediation cuts both ways. Custody at NTRS and BK is more resilient than advisory revenue at the banks or carry at the funds, which is part of why the service layer held up while the managers didn’t.

The bigger risk is that the alts firms’ bet on private wealth disappoints. They are counting on family-office and high-net-worth money to fuel their next leg of growth; if those flows stall the way retail private-credit flows did when several large funds gated redemptions earlier this year, the growth multiple on BX, KKR and APO compresses further. Part of this bear case has already played out in the price action above — the same families learned that illiquid means illiquid right before the managers de-rated.

Two more cautions. First, opacity: because the sector reports nothing, the “$3 trillion” is an estimate concentrated in a few hundred offices, not an evenly spread, easily tracked pool. Second, the regulatory tail. The family-office exemption gets questioned periodically, and the cautionary tale is Archegos — the family office that managed about $36 billion of Bill Hwang’s money and used total-return swaps to hide its exposure from its own banks before defaulting in March 2021. Hwang was later sentenced to 18 years. Any tightening of the exemption in response would add cost and disclosure across the industry.

What we’re watching

- The annual family-office surveys — UBS, Citi and J.P. Morgan — for the direction of the direct-investing share. The fresh 2026 UBS report is the most current read.

- Private-wealth AUM disclosures from Blackstone (now $250B+ for individuals), KKR’s K-series and Apollo — the clearest evidence of whether the family-office and high-net-worth capture is real or aspirational.

- Custody-servicing growth at NTRS and BK — the organic health of the most resilient layer.

- The dollar signal — if 65% of family offices follow through on cutting dollar exposure, watch the read-through to gold, non-US equities and FX.

- Any move to narrow the SEC family-office exemption in the long shadow of Archegos.

- Pre-IPO secondary marks on names like SpaceX, where family offices are active buyers.

The bottom line

The family office is the one corner of finance engineered specifically to keep outsiders out — no door, no units, no filings. That exclusivity is precisely why the public companies that custody, advise, and co-invest alongside these families are the only practical way to ride the trend. And the past year delivered a quiet lesson about which ones: when the ultra-wealthy got richer and more numerous, the money showed up not in the alternative managers everyone points to, but in the unglamorous plumbing that holds the assets and sends the statements.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!