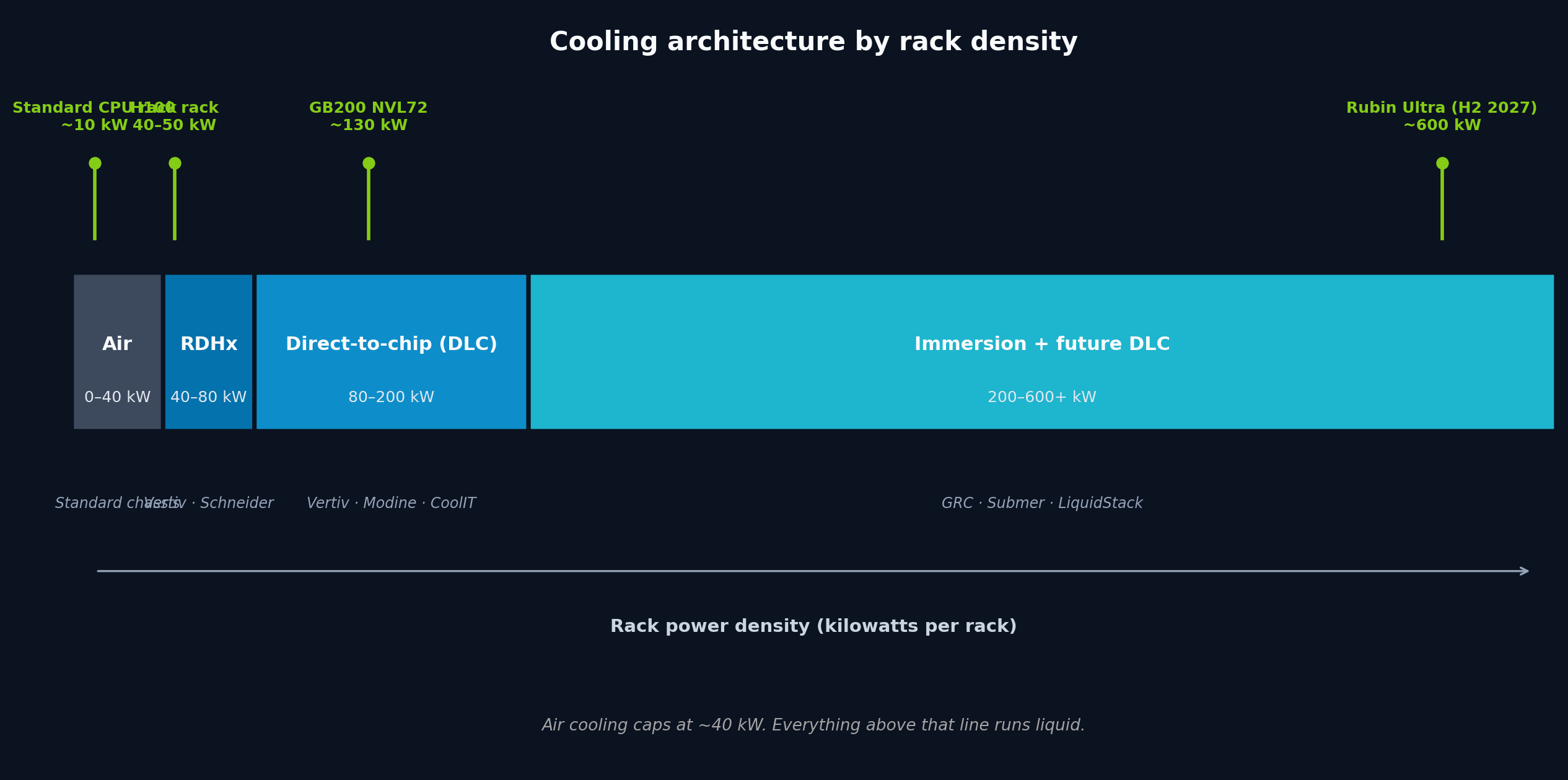

- A standard CPU rack draws 10 kilowatts; a GB200 NVL72 AI rack pulls 130 — air cooling caps out around 40, so everything above that line runs on liquid coolant.

- Vertiv (VRT) backlog more than doubled to $15B+ in Q1 2026, with 2026 revenue guidance raised to $13.5–14.0B; Modine (MOD) Data Center revenue grew 119% year-over-year to $644M in FY2026.

- Dell'Oro projects the data center liquid cooling market grows from ~$3B in 2025 to ~$7B by 2029, riding the $660–690B hyperscaler capex wave.

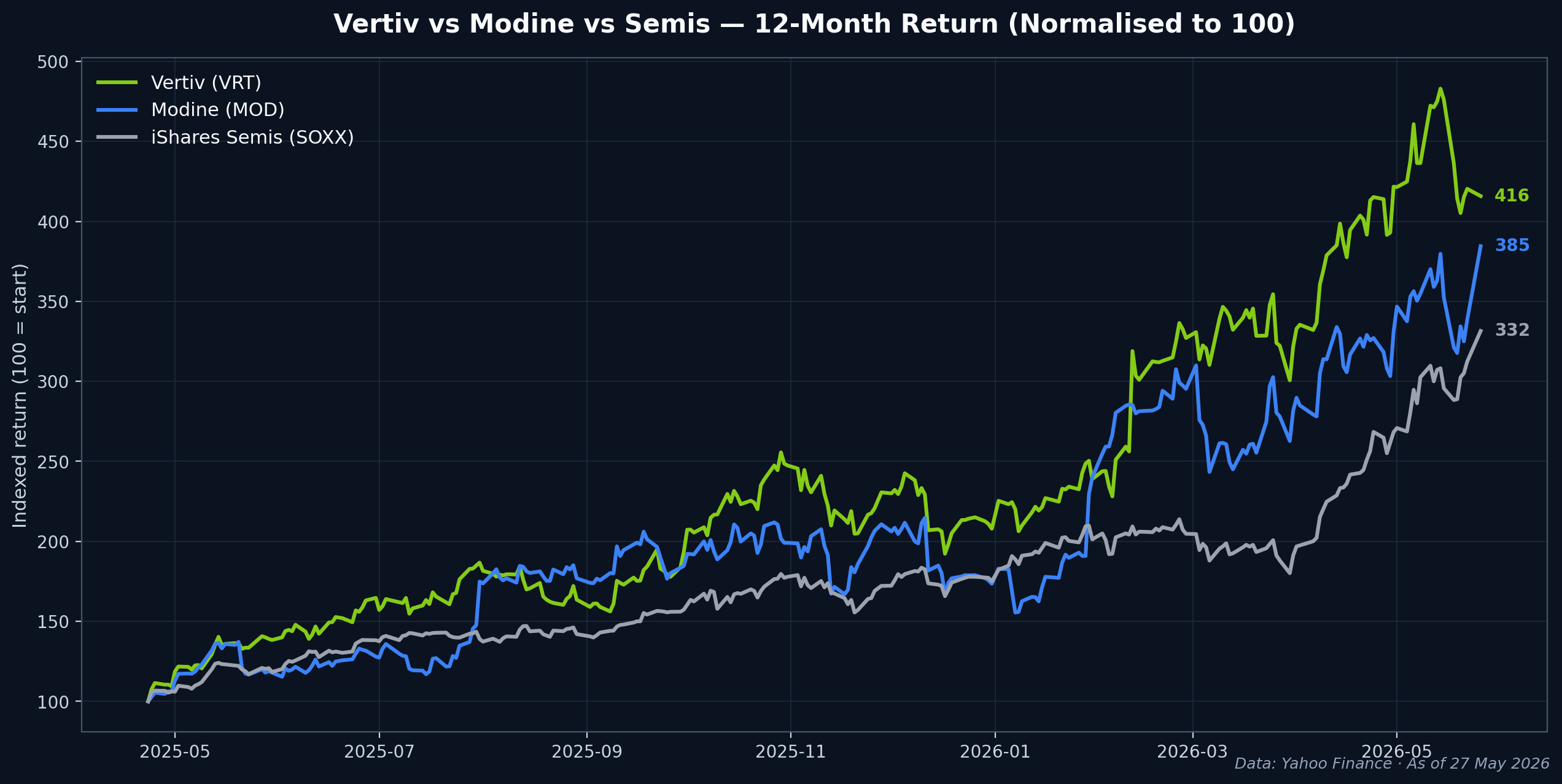

A standard server rack draws 10 kilowatts. An NVIDIA GB200 NVL72 rack pulls 130 — thirteen times the heat, in the same footprint. Air cooling caps out around 40kW. Everything above that line — and there’s a lot of “above that line” being built right now — runs on liquid. Liquid cooling stocks like Vertiv (VRT) and Modine (MOD) are pricing that gap in: Vertiv last printed $323.91 going into publication on May 27, 2026, up roughly 195% in the trailing twelve months — ahead of the iShares Semiconductor ETF (SOXX), which gained 174% over the same window. Modine outpaced both at +220%.

The thesis is mechanical, not narrative: density-per-rack is climbing on a published NVIDIA roadmap, the cooling architecture that handles each density tier is well-understood, and the two US-listed names with concentrated exposure are Vertiv and Modine. Dell’Oro Group’s January 2026 forecast puts the data center liquid cooling market at roughly $3 billion in 2025, on track for about $7 billion by 2029 — more than doubling in four years, riding the same $660–690 billion hyperscaler capex wave that pushed Vertiv’s backlog past $15 billion in the most recent quarter.

Why this matters now

The AI infrastructure trade has run in phases. Phase 1 was the GPUs — NVIDIA, AMD, the design-to-tape-out cycle. Phase 2 was the silicon supply chain — TSMC, the lithography names, the high-bandwidth memory shortage. Then power moved to centre stage: grid queues, transformer backlogs, the SMR financing question. Phase 4 is cooling — the same density curve that broke the grid is now breaking the air-cooled rack.

The forcing function is rack density. A standard CPU rack runs around 10 kilowatts. A 4-system NVIDIA H100 rack — the workhorse of 2024–2025 buildouts — sits at roughly 40–50kW, the practical ceiling for advanced air cooling. The GB200 NVL72 rack that started shipping in volume this year draws about 130kW at full load (NVIDIA’s nominal spec is 120kW; HPE’s deployment sheet reports 115kW liquid-cooled compute + 17kW air-cooled support). NVIDIA’s published roadmap pushes the next tier — the Rubin Ultra NVL576 “Kyber” rack expected in the second half of 2027 — to 600 kilowatts. That’s not an aggressive projection; it’s the spec sheet.

That density curve drives a cooling spend curve. The five largest US hyperscalers (Microsoft, Alphabet, Amazon, Meta, and Oracle) have guided to combined capital expenditure of roughly $660–690 billion in 2026, nearly doubling 2025’s $400 billion. Cooling is a small but rising share of every dollar spent. Direct-to-chip liquid cooling runs $3,500–5,000 per kilowatt installed versus $1,800–3,200 per kilowatt for advanced air — a 20–30% upfront premium that hyperscalers are paying because at densities above 20 kilowatts per rack, total facility capex actually drops by 10–14% (less floor space, less air-side infrastructure) and power-usage effectiveness improves materially.

Power was phase 1 of the AI infrastructure story for a reason: the constraint was visible — grid queues that span years, transformer waitlists, the publicly fought SMR financing question. Cooling has the same constraint structure, just one layer downstream. The market is starting to price that, but the multiples on VRT and MOD suggest it isn’t fully priced yet.

How liquid cooling actually works — the three architectures

Liquid cooling isn’t one technology. It’s three architectures stacked by rack density, each with a different supply chain and a different set of vendors holding the relationships.

Rear-door heat exchangers (RDHx): 40–80kW per rack

The simplest entry point. The back door of the server rack is replaced with a coil through which chilled water from the building loop flows. Hot air from the servers passes through the coil on its way out the back; the water absorbs the heat. Standard air-cooled servers, mostly unchanged inside the chassis — the only modification is the door itself.

What makes RDHx attractive: it slots into existing air-cooled facilities without ripping up the server chassis design. What makes it limited: at densities above ~80kW, even chilled-water back doors can’t dissipate fast enough, because the air pathway is still the bottleneck inside the rack. RDHx is a transition technology — useful for retrofitting legacy halls into mid-density AI service.

Direct-to-chip (DLC): 80–200kW per rack

The dominant architecture for the GB200 class and the assumed cooling for the entire Vera Rubin generation. A cold plate sits on top of each GPU and each CPU; coolant flows through manifolds, into the cold plates, picks up heat directly from the chip surface, returns through a coolant distribution unit (CDU) at the base of the rack, and exchanges that heat with the facility loop.

The thermal path is much shorter than RDHx — no air gap between heat source and heat sink — so DLC handles the 100–200kW range that current-gen Blackwell racks live in. NVIDIA designs the GB200 NVL72 with DLC as the assumed cooling architecture; the 17kW air-cooled portion is just management and power distribution components that don’t generate enough heat to justify a dedicated cold plate.

The supply chain layer that mostly goes unspoken: thermal interface materials (TIMs), the gels and pads sitting between the chip surface and the cold plate. Tighter thermal-interface tolerances mean higher sustained turbo clocks, which means more performance per dollar of GPU spent. It’s a quiet $1–2 billion sub-market that Honeywell, Henkel, and a handful of smaller specialists fight over, with no clean pure-play public name.

Immersion cooling: 100kW+ per rack, niche but growing

The whole server is submerged in a tank of dielectric coolant — either single-phase (the coolant stays liquid) or two-phase (the coolant boils on contact with hot components, condenses on a coil at the top of the tank, drips back down). PUE numbers approach 1.02 — meaning almost every watt that comes into the facility goes to compute, not cooling overhead.

What’s stopped immersion from being the default architecture: standard servers don’t immerse cleanly. Spinning hard drives, cardboard packaging on memory DIMMs, label adhesives on power supplies — all need redesign or replacement. The hyperscalers run pilot deployments; nobody runs a 100% immersion campus yet. The economics work at very high densities, but the operational complexity (drain a tank to service one card) keeps it niche relative to DLC. Most immersion vendors are private: LiquidStack, GRC, Submer. The public-market exposure to immersion is thin.

Where the money flows — liquid cooling stocks

The cleanest way to express the cooling thesis is through two names, with two more in supporting roles.

Vertiv (VRT) — the lead

Vertiv came out of the 2020 Emerson spin-off as a pure-play data center critical infrastructure name — thermal management, power delivery, monitoring, the boring layer between the building shell and the IT racks. The AI capex cycle has rewritten its growth profile.

Q1 2026 revenue was $2.65 billion, up roughly 33% year-over-year. The number worth pinning to the wall: backlog more than doubled to over $15 billion, equivalent to 12–18 months of forward revenue coverage at current run rates. Management raised full-year 2026 guidance to $13.5–14.0 billion in revenue and $6.30–6.40 in adjusted EPS — the kind of mid-year guidance raise that lands when a customer base is locking in multi-quarter capacity, not when a salesforce is hopeful.

In April 2026, Vertiv bought Strategic Thermal Labs, a small cold-plate engineering specialist. The acquisition is modest in dollar terms but signals the integration pattern: hyperscalers want a single-vendor liquid-cooling stack from coolant distribution unit down to the cold plate sitting on the chip. Vertiv is the most credible name that can ship that stack at scale today.

Modine (MOD) — the mid-cap call

Modine is what a New England textile mill was to the cotton boom — a legacy industrial business that found itself sitting on a structurally growing customer base. FY2026 (ending March 2026) revenue hit $3.18 billion, up 23% year-over-year. The Data Center sub-segment within Climate Solutions: $644 million in revenue, up 119% year-over-year — roughly 20% of total company revenue but essentially the entire growth contribution.

The Climate Solutions segment as a whole — which houses Data Center alongside the HVAC names that originally built the company — is now about 63% of total revenue, and management has signalled a planned spin-off of the Performance Technologies segment to concentrate the data-center mix further. Margin trajectory should follow: a Modine that’s 70%+ Climate Solutions trades at a different multiple than a diversified industrial that happens to have a hot segment.

Schneider Electric (SBGSF / SU.PA) — the diversified hedge

Schneider’s EcoStruxure IT and APC cooling brands are everywhere in hyperscaler builds, but Schneider is a €40+ billion revenue conglomerate with energy management businesses far larger than its data-center exposure. The thesis is right-sized exposure without the volatility of a pure-play. The trade-off: less torque to the cooling cycle than VRT or MOD give you. It’s a hedge, not a torque trade.

Peripheral plays and what’s NOT a pure-play

Parker Hannifin (PH) supplies the pumps and manifolds that route coolant through DLC systems — small relative to Parker’s total revenue, but a structural lift to one of its industrial segments. Asetek (ASTK on Oslo Stock Exchange) is a smaller direct-to-chip vendor with European institutional appetite. Honeywell (HON) and Henkel sit in the TIM layer below the cold plates — neither is a pure-play, but each gets a small lift from rising DLC volumes.

The most common confusions worth flagging: Emerson divested its Network Power business — which became Vertiv — back in 2016, so Emerson is no longer cooling exposure. Carrier (CARR) and Trane Technologies (TT) are dominant residential and commercial HVAC names whose data-center segments are too small to move the consolidated picture. The pure-play map is narrower than the headline “AI cooling theme” suggests.

What could break this thesis

Four risks deserve real treatment, not boilerplate.

NVIDIA’s own integration. The GB200 NVL72 ships with a substantial portion of the liquid cooling integrated at the rack level — manifolds, distribution, cold plates engineered to NVIDIA’s spec. Rubin and Rubin Ultra are expected to deepen this integration. The open question is whether NVIDIA’s tighter rack-scale design crowds out third-party manifold and CDU vendors, or locks them in as preferred suppliers. Vertiv’s Q1 2026 commentary suggests the latter — hyperscalers want a partner with installation depth, and NVIDIA is not in that business. But the equilibrium is still being negotiated. A shift toward NVIDIA in-house thermal manufacturing would compress VRT margins on the highest-density tier.

Hyperscaler vertical integration. Google, Meta, and Microsoft all run internal thermal engineering teams. Google has been the most aggressive — its custom TPU pods use bespoke cooling designs that bypass merchant vendors. If Meta and Microsoft follow that path on their custom silicon (Maia, MTIA), the addressable market for outside vendors shrinks on the most rapidly-growing slice of hyperscaler spend. The hedge: external supply is still cheaper for non-custom NVIDIA fleets, which remain the bulk of the 2026 buildout.

Direct-to-chip wins, immersion “strands.” Most immersion equipment is sold by private companies — LiquidStack, GRC, Submer. If the market settles on direct-to-chip as the dominant architecture for the 100–600kW racks that the Vera Rubin roadmap implies, immersion specialists end up serving a smaller niche than today’s optimistic forecasts assume. This doesn’t hurt VRT or MOD — both bet primarily on DLC. It does mean the broader “liquid cooling” theme is narrower than the headline total addressable market suggests, and the public-equity exposure to immersion specifically is minimal.

Commodity and regulation risk. Copper tubing prices, coolant chemistry (PFAS regulation is tightening in the EU and California — some dielectric coolants are PFAS-based), and the rare-earth content in pump motors all sit in the cost-of-goods stack. A copper spike or a PFAS-mandated coolant reformulation hits Modine more than Vertiv given Modine’s manufacturing-heavy mix.

Signals to watch

Three data points to track on this cycle:

VRT and MOD quarterly backlog disclosures. Vertiv broke past $15 billion in Q1 2026; the next print (Q2 in late July) will show whether order momentum is still building or peaking. Modine’s Data Center segment growth rate is the cleaner read — if it sustains above 75% year-over-year through the Performance Technologies spin-off, the multiple holds.

Dell’Oro quarterly TAM revisions. Dell’Oro’s market-sizing reports get revised every quarter; the trajectory of those revisions is the institutional flow signal. A market that’s been revised up four quarters in a row is a market with momentum behind earnings revisions. The January 2026 print already raised the 2029 number meaningfully.

NVIDIA’s rack-density spec sheets. Public Vera Rubin and Rubin Ultra documentation has set the 600kW endpoint for H2 2027. What matters is whether the intermediate generations (Vera Rubin NVL72, the rumoured NVL36) follow that ramp or back off. A backed-off intermediate means cooling intensity peaks earlier; a sustained ramp confirms the secular thesis.

The cooling layer is the most overlooked piece of the AI infrastructure trade. Power got the headlines first because it ran into a hard constraint the public could see — grid queues, transformer shortages, the SMR financing question. Cooling has the same constraint structure, one step downstream, and the public-market pure-plays mapping to it are concentrated in two names. The earnings trajectories suggest the market is starting to understand that. The multiples suggest it’s still early.

For the upstream layer of this story — the GPU and silicon supply chain feeding the racks that need cooling — see our note on the custom silicon race. For the dollar context — what the $700 billion hyperscaler capex number actually buys — see hyperscaler capex and the $700B number.

Get early access to Orbit

Orbit is Luna3.ai’s AI-augmented research engine. 12 algorithmic signals + a gradient-boosted ML model + an agentic LLM that reads each top pick’s filings and writes a daily thesis with conviction score and catalyst proximity. Three regimes, three playbooks — growth in expansion, defensives in late-cycle, recovery plays at panic bottoms. The 3 in Luna3.ai.

No spam. Unsubscribe any time.

No comments yet. Be the first to share your thoughts!